Over at TheMoneyIllusion, Scott Sumner takes a shot at what he refers to as “Disinflation Denial.” His point is that prior to the recent run-up, “commodity price indices fell by more than 50%.” Thus, if the run-up in commodity prices suggests loose policy now, they must have been signaling tight policy earlier.

I am hesitant to endorse the view that any subset of prices gives us a clear view of inflation trends. What I do endorse in the Sumner piece is the advice that “the Fed look at a wide range of indicators.” I can tell you that is exactly what we do at the Atlanta Reserve Bank and, as just one example within the Fed System, in this post I’ll review the battery of indicators that we are currently looking at here. Most of these will be no surprise, but I find it useful to occasionally see them in one place. So here we go. (Note that throughout this blog post I will focus most of my comments on the consumer price index [CPI], but most of what I say also applies to the personal consumption expenditure [PCE] price index as well.)

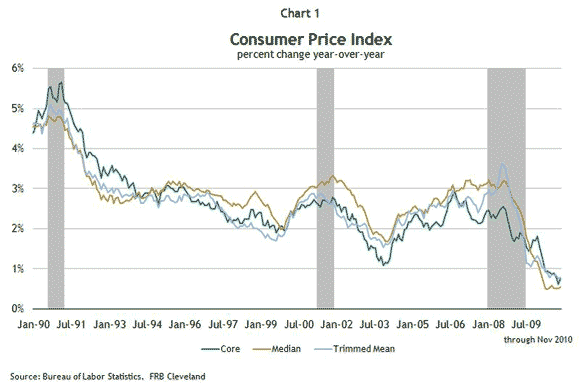

First up, of course, are the so-called (and often maligned) core measures of inflation. I am completely sympathetic to the view that the traditional core index, which subtracts out food and energy components, is a somewhat arbitrary cut of the price statistics. For that reason, Ipersonally tend to lean more heavily on median and trimmed-mean measures.

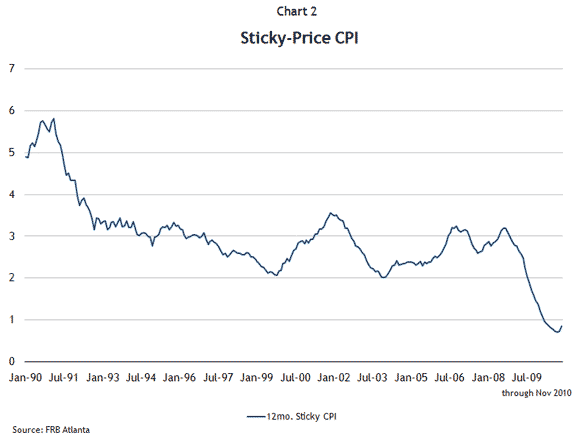

In Atlanta, we have been monitoring a newer core inflation measure, called the “sticky-price CPI,” jointly developed by Mike Bryan and Brent Meyer (of the Atlanta and Cleveland Feds, respectively). As described by Bryan and Meyer:

“Some of the items that make up the Consumer Price Index change prices frequently, while others are slow to change… sticky prices [those that are slow to change] appear to incorporate expectations about future inflation to a greater degree than prices that change on a frequent basis… our sticky-price measure seems to contain a component of inflation expectations, and that component may be useful when trying to gauge where inflation is heading.”

Like the other core measure, the sticky-price CPI shows a pronounced downward movement over the past several years, with some sign of (an ever-so-slight) recovery as of late.

Though I disagree with the assertion that core measures are a convenient way to ignore unpleasant movements in the overall CPI—there is evidence that core measures are useful in predicting where total CPI inflation is heading—it is almost surely a bad idea to ignore what is happening to headline statistics. (After all, in the end it is the average of all prices with which we are concerned.)

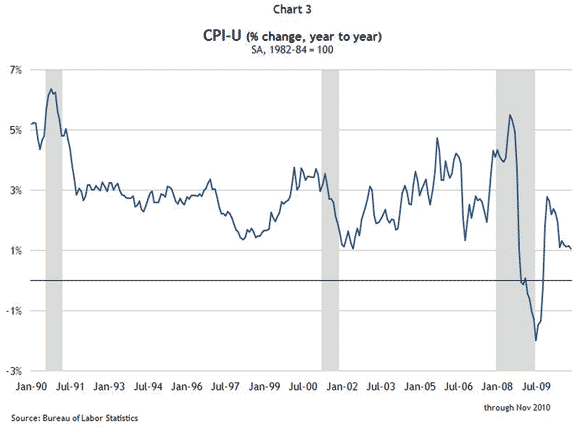

Here too, the evidence suggests, at the very least, there is scant evidence that disinflation has left the scene:

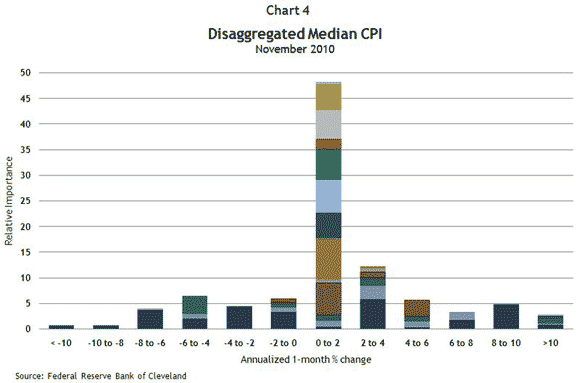

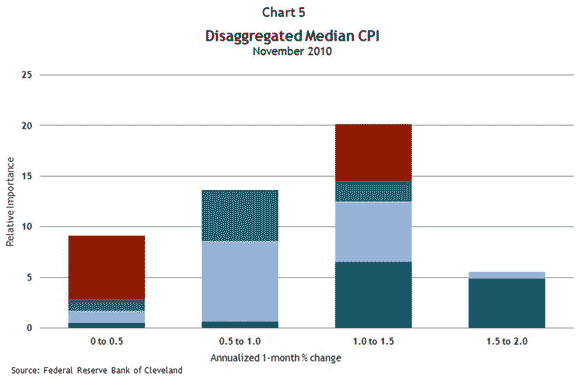

I find it useful to take at least two more cuts at the overall price data. One, which has a decidedly short-term focus, involves examining the distribution of price changes in the broad categories that make up the headline CPI. Though a popular criticism of Fed policy—discussed and critiqued at Econbrowser—tries to deflate deflation concerns by reciting a number of prices that are rising, it is obvious that one could just as easily tick off a reasonably large list of prices that are falling:

(The individual colors in the chart represent different components of the CPI. The underlying data can be found from this link to the explanation of the median CPI.)

The graph of the November price change distribution is actually somewhat encouraging. What it tells us is that almost half of the price changes in the CPI market basket, weighted by their shares of total consumer expenditures, fell in the (annualized) range of 0 percent to 2 percent. Furthermore, about as many price changes were below this range as they were above it.

A closer look at the prices that fall in the 0 percent to 2 percent category, however, reveals that individual price changes are skewed to the downside of the range:

On a month-to-month basis, the distribution of individual prices does shift around, so these statistics are nothing more than suggestive short-run snapshots (but I believe they are informative nonetheless).

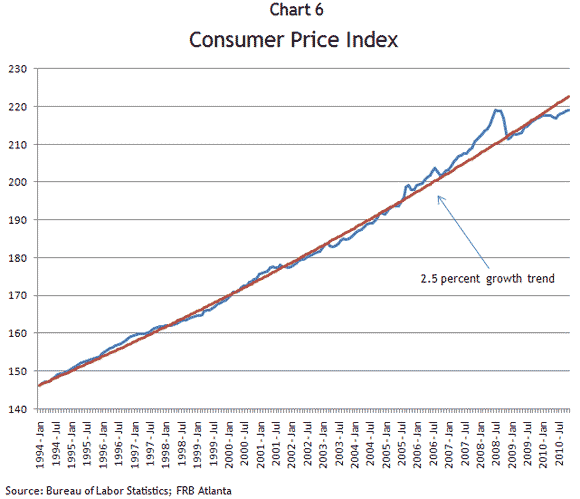

At the other end of the temporal scale is a look at how inflation has behaved over time. If the central bank had a long history of missing its stated inflation objectives, we might feel very different about an inflation rate that is below what Chairman Bernanke has referred to as “the mandate-consistent inflation rate” of “about 2 percent or a bit below” than we would if average prices were hewing pretty close to the target path. As I have previously noted, over the past 15 years or so, the Federal Open Market Committee (FOMC) has delivered an average inflation rate, measured as growth in the PCE price index, that is wholly consistent with this mandate. Here’s the case in a graph, adjusting the mandate-consistent inflation rate to account for an assumed upward bias in the CPI relative to the PCE index:

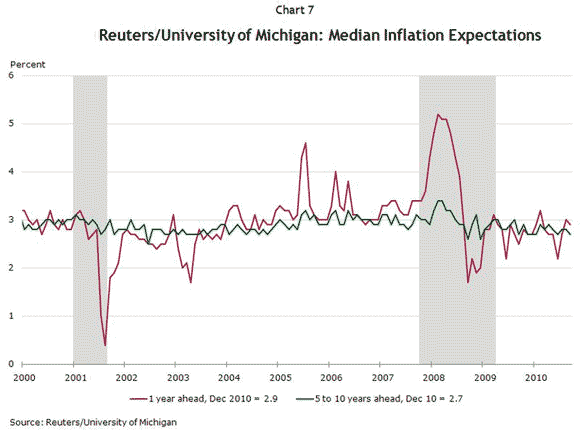

Actually, those short-run complications are mostly associated with falling expectations of inflation. In my last macroblog post, I argued that the stabilization of market-based CPI inflation expectations and the associated decline in the perceived probability of deflation should arguably be counted as a success of the Fed’s current policy stance. The latest on market-based expectations was included in our previous macroblog item. For completeness, survey-based expected long-term inflation remains somewhat below the levels prior to the onset of the recession:

I believe this is basically the bottom line: whether we look at headline inflation (straight-up, component-by-component, or in terms of the long-run trend), core inflation measures (of virtually any sensible variety), or inflation expectations (survey or market based), there is little a hint of building inflationary pressure.

While I don’t dismiss the usefulness of looking at other indicators (stock prices, bond prices, foreign exchange rates, commodity prices, and real estate prices are on Scott Sumner’s list; I would add various measures of labor costs to mine), you have to be pretty selective in your attentions to build the contrary case.

But feel free. We’ll keep watching.

Leave a Reply