Since the mid-1980s, when a number of cranks argued that the balance sheet of the US needed to be laid bare, including off balance sheet items like Social Security and Medicare, there came a statutory requirement that there would be a Financial Report of the US Government.

Here is fiscal 2010′s report. Page with more options here.

Now let me give you my summary of the 2010 report.

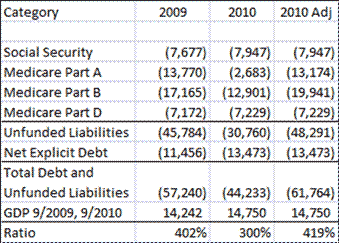

Note the large drops in net liability for Medicare parts A & B. This is the effect of the “Affordable Care Act.” (My, what an Orwellian name.) Yes, Obamacare, in order to get the bill passed, said that there would be reductions made to reimbursements for Medicare.

Note the large drops in net liability for Medicare parts A & B. This is the effect of the “Affordable Care Act.” (My, what an Orwellian name.) Yes, Obamacare, in order to get the bill passed, said that there would be reductions made to reimbursements for Medicare.

The benefits from Medicare are statutory, and are not rights, per se. Yet there are human needs that prompt the estimates, at least on average.

That is why I don’t think that the 2010 report is accurate, and they agree with me in their verbiage:

The extent to which actual future Part A and Part B costs exceed the projected current-law amounts due to changes to the productivity adjustments and physician payments depends on both the specific changes that might be legislated and on whether Congress would pass further provisions to help offset such costs. As noted, these examples only reflect hypothetical changes to provider payment rates.

It is likely that in the coming years Congress will consider, and pass, numerous other legislative proposals affecting Medicare. Many of these will likely be designed to reduce costs in an effort to make the program more affordable. In practice, it is not possible to anticipate what actions Congress might take, either in the near term or over longer periods.

The Medicare Board of Trustees, in their annual report to Congress, references an alternative scenario to illustrate the potential understatement of costs under current law. This alternative scenario assumes that the productivity adjustments are gradually phased out over the 15 years starting in 2020 and that the physician fee reductions are overridden. These examples were developed by management for illustrative purposes only; the calculations have not been audited; and the examples do not attempt to portray likely or recommended future outcomes. Thus, the illustrations are useful only as general indicators of the substantial impacts that could result from future legislation affecting the productivity adjustments and physician payments under Medicare and of the broad range of uncertainty associated with such impacts. The table below contains a comparison of the Medicare 75-year present values of income and expenditures under current law with those under the alternative scenario illustration.

ObamaCare assumes/demands that it can pass through cost reductions to Medicare recipients. The difficulty is whether doctors and other healthcare providers will accept reduced payments. What is a reduction in payment may become a reduction in service. Who cares if you have Medicare, if few doctors are willing to accept it?

Public Statement

I would be much happier if we placed healthcare to be an ordinary matter, not something where the government intervenes to assure coverage. When Medicare was created in the ’60s, the costs of assuring coverage was low, but the government did not accrue the assets to pay for the future coverage. Then again, neither did the budding health insurance business, which relied on estimates of uninsured health care usage to price products, and was surprised to find that usage rises when one is insured. (Just as many health insurers in the present day underpriced high deductible policies for HSAs, assuming that utilization would go down a lot. Instead, it went down a little.

Today, we face a shortfall in most municipalities, where there is not enough to pay benefits, absent an increase in taxes from the municipalities. The taxes will be a continuing burden for municipalities.

Beyond Municipalities

The government can assume that there will be less cost from Medicare. That bogus concept allowed the “Affordable Care Act” to pass. But will Congress have the guts to stand behind their actions when oldsters complain? I doubt it, so I think costs will be considerably higher here.

How much higher? Well, deep in the report on pages 129-131 they suggest an alternative scenario:

This alternative scenario assumes that the productivity adjustments are gradually phased out over the 15 years starting in 2020 and that the physician fee reductions are overridden.

The result is a $12.3 trillion increase in the net present value. Now it would have been nice, and the actuaries could have done it, if they would have broken out separately:

- The effect of the productivity phase-out

- The effect of overriding the physician fee reductions.

- And even, just showing what the difference would have been if they had run the calculation using last year’s assumptions.

That last one is the key omission. As it is, I can’t tell but can only guess at how much higher the liabilities of the government are, going from 2009 to 2010. Compared to using the 2009 assumptions, the 2010 liability figure is understated by $12.3 trillion minimum. My guess on the 2010 liability has the present value of expenses for Medicare parts A & B running ahead at 7% from 2009 to 2010, which is similar to many prior years in the recent decade, if not on the low side.

To see the total liabilities rise by $4.5 trillion in fiscal 2010 isn’t unreasonable, when one sees that the net debt has gone up by $2.0 trillion, and add in the natural drift of underfunded entitlement plans in a slow economy, where unemployment is high. Not counted in the estimate is the payroll tax holiday, which is a ridiculous policy because employers do not respond to temporary measures, and Social Security is already in bad shape.

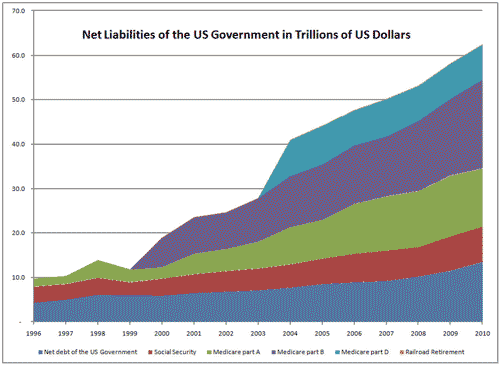

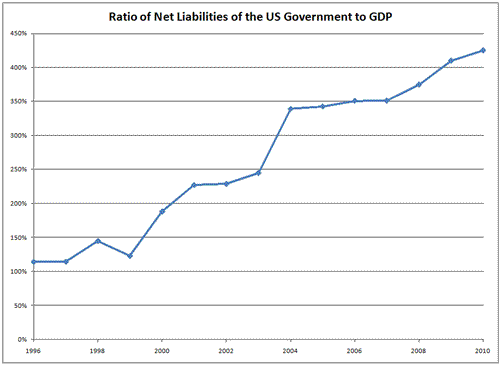

So, there is little reason for cheer in this financial report. In closing, here are a few charts using my estimate for 2010:

Leave a Reply