I am late getting to this, but Mark Thoma wants to hear the case for nominal GDP targeting. This approach to monetary policy requires the Fed stabilize the growth path for total current dollar spending. As an advocate of nominal GDP level targeting, I am more than happy to respond to Mark’s request. I will focus my response on what I see as its three most appealing aspects: (1) it provides a simple and intuitive approach to monetary policy, (2) it focuses monetary policy on that over which it has meaningful influence, and (3) its simplicity makes it easier to implement than other popular alternatives. Let’s consider each point in turn.

(1) It provides a simple and intuitive approach to monetary policy. This first point can be illustrated by considering the following scenario. Imagine the U.S. economy is humming along at its full potential. Suddenly a large negative shock, say a housing bust, hits the economy. This development leads to a decline in expectations of current and future economic activity. As a result, asset prices decline, financial conditions deteriorate, and there is a rush for liquidity. The rise in demand for liquidity means less spending by households and firms and thus, less total current dollar spending in the U.S. economy. Because prices do not adjust instantly, this drop in nominal spending causes a decline in real economic activity too. Thus, even though the primal cause of the decline in the real economy was the housing bust, the proximate cause was the drop in total current dollar spending. The Fed cannot undo the housing bust, but it can prevent the drop in total current dollar spending by providing enough liquidity to offset the spike in liquidity demand. If nominal spending has not been stabilized then the Fed has failed to do this. A nominal GDP target, then, is simply a mandate for the Fed to stabilize total current dollar spending.

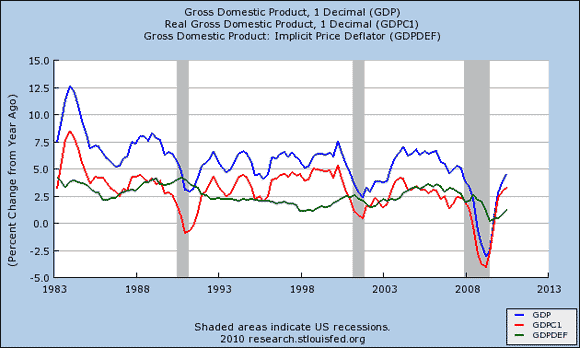

Though a simple objective, stabilizing nominal spending is key to macroeconomic stability. The figure below shows that changes in the growth rate of total current dollar spending (i.e. nominal GDP) got transmitted mostly to changes in the growth rate of real economic activity (i.e. real GDP) rather than inflation (i.e. GDP Deflator). This implies that had monetary policy done a better job stabilizing nominal spending then there would have been fewer recessions during this time.

(2) It focuses monetary policy on that over which it has meaningful influence. There are two types of shocks that buffet the economy: aggregate supply (AS) shocks and aggregate demand (AD) shocks. A nominal GDP targeting rule only responds to AD shocks. It ignores AS shocks while keeping total current dollar spending growing at a stable rate. This is the way it should be. For if monetary policy attempts to offset AS shocks it will tend to increase macroeconomic volatility rather than reduce it. For example, let’s say Y2K actually turned out to be hugely disruptive for a prolonged period. This negative AS shock would reduce output and increase prices. A true inflation targeting central bank would have to respond to this negative AS shock by tightening monetary policy, further constricting the economy. A nominal GDP targeting central bank would not face this dilemma. It would simply keep nominal spending stable.

In general, any kind of price stability objective for a central bank is bound to be problematic because price level changes can come from either AD or AS shocks and are hard to discern. For example, was the low U.S. inflation in 2003 the result of a weakened economy (a negative AD shock) or robust productivity gains (a positive AS shock)? It makes much more sense to focus on the underlying economic shocks themselves rather than a symptom of them (i.e. price level changes). Nominal GDP targeting does that by focusing just on AD shocks. This point is graphically illustrated here using the AD-AS model. More discussion on this point can be found here.

(3) Its simplicity makes it easier to implement than other popular alternatives. This is true on many front. First, a nominal GDP target requires only a measure of the current dollar value of the economy. It does not require knowledge of the proper inflation measure, inflation target, output gap measure, the neutral federal fund rate, coefficient weights, and other elusive information that are required for inflation targeting and the Taylor Rule. There will always be debate on which form of the above measures is appropriate. For example, should the Fed go with the CPI or PCE, the headline inflation measure or the core, the CBO’s output gap or their own internal estimate, the original Taylor Rule or the Glenn Rudebush version, etc.? A nominal GDP target avoids all of these debates.

Second, nominal GDP targeting would also be easier to implement because it is easy to understand. The public can comprehend the notion of stabilizing total current dollar spending. It is less clear they understand output gaps, core inflation, the neutral federal funds rate, and other esoteric elements now used in monetary policy. The Fed would have a far easier time explaining itself to congress and the public if it followed a nominal GDP target. On the flip side, this increased understanding by the public would make the Fed more accountable for its failures.

Third, a nominal GDP target would take the focus off of inflation and what its appropriate value should be. Thus, if there needed to be some catch-up inflation and nominal spending to get nominal GDP back to its targeted growth path the Fed could do it with less political pressure.

Some folks argue that the nominal GDP targeting is nothing more than just a special case of a Taylor Rule. Maybe so, but they miss the bigger point that nominal GDP targeting is a far easier approach to implement for the reasons laid out above. Moreover, in practice the Fed has deviated from the Taylor Rule and during these times it appears to be more of a pure inflation targeter. Thus, adopting an explicit nominal GDP target would force the Fed to stick to stabilizing nominal spending at all times.

Ultimately, I would like to see the Fed adopt not only a nominal GDP level target, but a forward-looking one that targeted nominal GDP futures market. This is an idea that Scott Sumner and Bill Woolsey have been promoting for some time. See here and here for more on this proposal.

Leave a Reply