The yield on 10-year Treasuries has slipped back to just a hair over 3% – despite the fact that the US has hit its legal “debt ceiling.” The fresh reversal in yields appears to be further evidence against the ongoing hard-money fears that the combination of quantitative easing, deficit spending, and a falling Dollar are sure to spell inflationary doom. As Paul Krugman likes to quip, the bond market vigilantes remain invisible.

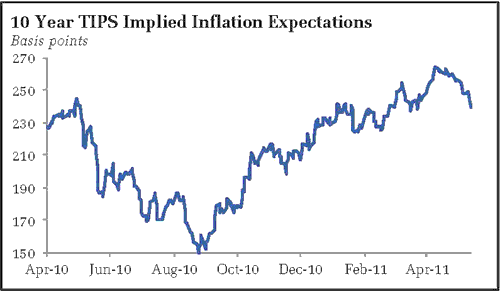

From a monetary policy perspective, the behavior of the Treasury market would suggest that it may be too early to tap on the policy breaks. Here I offer an alternative perspective – one that I suspect will find some play among Fed officials. Recall that in his recent press conference, Federal Reserve Chairman Ben Bernanke focused on the need to maintain stable inflation expectations. Consider the behavior of an admittedly rudimentary measure of inflation expectations, the spread between Treasuries and inflation protected Treasuries:

By this measure, inflation expectations have come off their peaks in recent weeks. Further evidence that bond market vigilantes were getting ahead of themselves? Or evidence that the Fed did what “needed” to be done – throttle back on monetary policy to keep expectations under control?

In other words, I can see where some Fed officials could make the case that financial markets are simply responding positively to good, old-fashioned monetary austerity. The implications for policy are straightforward; officials could pat themselves on the back for a job well done, rather than worry that the move toward tighter money was once again premature.

From my perspective, recent market activity has followed a standard playbook – the advent of QE2 push market participants into the obvious trades. Long equities and commodities and short Dollar. Trades that worked because they were balanced on a kernel of truth. Global economic activity did firm, and interest rate differentials should be Dollar negative. At the same time, there was always a risk the trades would overextend and collapse, either under their own weight because the Fed took away part of the story. Perhaps a little of both have occurred, with at least energy prices clearly sapping US growth and the Fed calling it quits on quantitative easing. What is left? An economy that is growing yet remains mired at a suboptimal level relative to potential output. Very similar to what we had before QE2 – an economic roundtrip to somewhere that is at least within sight of another lost decade for US job growth.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply