Several sources reported that the 2012 Republican Platform would call for a commission to explore the possibility of the U.S. returning to a gold standard. However, the final document makes no mention of gold, and instead seems to have settled on a proposal that is unlikely to do any harm:

President Reagan, shortly after his inauguration, established a commission to consider the feasibility of a metallic basis for U.S. currency. The commission advised against such a move. Now, three decades later, as we face the task of cleaning up the wreckage of the current Administration’s policies, we propose a similar commission to investigate possible ways to set a fixed value for the dollar.

I thought it would be worthwhile to review some of the reasons why we should be thankful that saner heads seem to have prevailed.

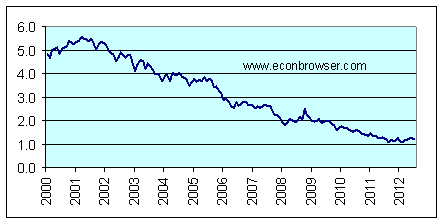

Here’s the core concern. In January of 2000, an average U.S. worker earned $13.75 an hour, and the price of gold was $283 an ounce. If you put in 100 hours of work at that wage, you would earn $1375, which would have been enough to buy a little less than 5 ounces of gold at the time:

Last month, the average U.S. wage was up to $19.77 an hour, but the price of gold had skyrocketed to $1623 an ounce. That means that for 100 hours of labor, the average worker today would only receive 1.2 ounces of gold. Here’s what average U.S. wages would look like if they were reported in units of ounces of gold earned per 100 hours instead of in the usual units of dollars earned.

Number of ounces of gold an average U.S. production and nonsupervisory employee would earn from 100 hours of work, January 2000 to July 2012. Calculated as 100 times the average wage divided by the dollar price of gold

But the essence of a gold standard is that the units used in the above graph would become the units in which wages and prices would get reported and negotiated. Under a gold standard, a dollar always means the same thing in terms of ounces of gold that it would buy. So for example, if the dollar price of gold today was the same as it was in January 2000 ($283/ounce), and if the real value of gold had changed as much as it has since then, the dollar wage that an average worker received would need to have fallen from $13.75/hour in 2000 to $3.45/hour in 2012.

And the problem with that is, for a host of reasons ranging from minimum wage legislation, bargaining agreements and contracts, institutions, and human nature, it is very, very hard to get workers to accept a cut in their wage from $13.75/hour to $3.45/hour. The only way it could possibly happen is with an enormously high unemployment rate for a very long period of time. This strikes most of us as a pretty crazy policy proposal.

To which the gold advocates respond with the claim that if the U.S. had been on a gold standard since 2000, then the huge change in the real value of gold that we observed over the last decade never would have happened in the first place.

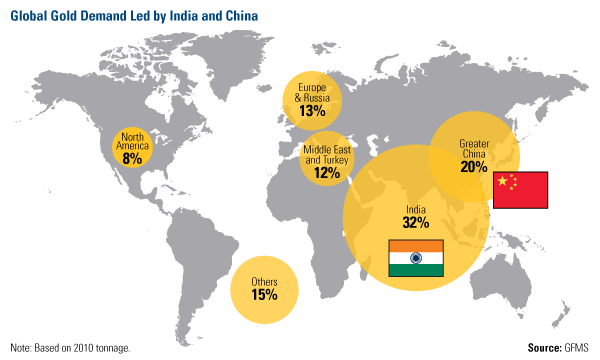

The first strange thing about this claim is its supposition that events and policies within the U.S. are the most important determinants of the real value of gold. According to the World Gold Council, North America accounts for only 8% of global demand.

Source: U.S. Global Investors

The surge in income from the emerging economies rather than U.S. monetary policy seems the most natural explanation for recent moves in the real value of gold.

Source: AdvisorAnalyst.com

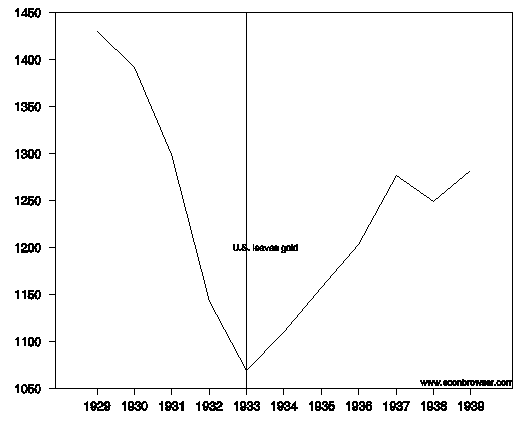

Moreover, between 1929 and 1933, the U.S. and much of the rest of the world were on a gold standard. That did not prevent (indeed, I have argued it was an important cause of) a big increase in the real value of gold over that period. Because the price of gold was fixed at a dollar price of $20/ounce, the increase in the real value of gold required a huge drop in U.S. nominal wages over those years. The theoretical outcome described in the first figure above is exactly what was observed to occur in practice. The problem was solved immediately after the United States abandoned the idea of fixing the price of gold at $20/ounce.

Dollar compensation per full-time equivalent employee in all U.S. industries (wage and salary accruals), 1929-1939. Data source: Historical Statistics of the United States, Table Ba4419-4421.

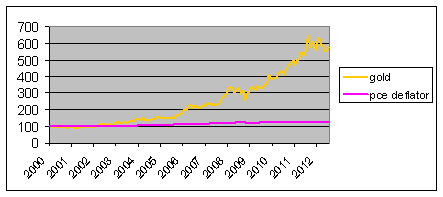

But the really odd thing about the current interest in returning to the gold standard is the timing. The proposals come after a decade in which U.S. inflation has been remarkably tame and stable. Here for example is the average U.S. price level as measured by the PCE deflator, shown on the same scale as gold prices.

Price of gold and average U.S. prices as measured by the implicit PCE deflator, January 2000 to July 2012, both normalized at Jan 2000 = 100.

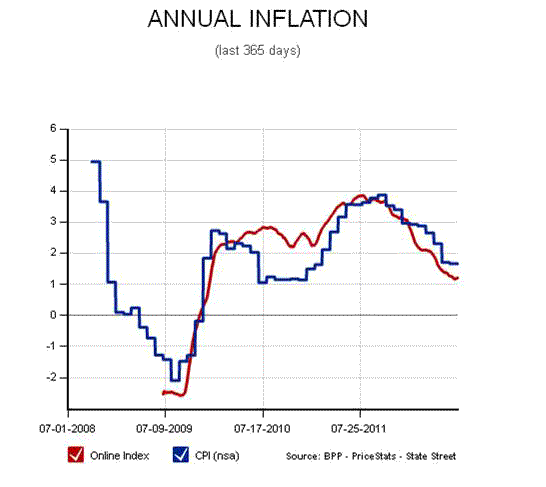

Part of the explanation is perhaps that hardcore gold bugs further disbelieve published government inflation measures such as the PCE deflator or the consumer price index, and likewise disbelieve the objective averaging of posted internet prices reported by MIT’s Billion Prices Project.

U.S. annual inflation rate as measured by CPI (blue) and prices sampled directly from internet listings (red). Source: Billion Prices Project.

For any of you who still believe that Shadowstats provides the only reliable U.S. inflation data, Paul Krugman supplies an amusing observation. The price of a 2012 subscription to Shadowstats is $175.

For comparison, six years ago the price was … $175.

Leave a Reply