The swift policy response to the recent financial crisis helped the world economy avoid a replay of the Great Depression of 1929-32. But can we avoid a replay of 1937-38? With the world economy weakening once again, this column addresses the question with a renewed urgency and comes up with an oft-overlooked explanation – the Treasury Department’s decision to sterilise all gold inflows starting in December 1936.

The recession of 1937-38 is sometimes called “the recession within the Depression.” It came at a time when the recovery from the Great Depression was far from complete and the unemployment rate was still very high. In fact, it was a disastrous setback to the recovery. Real GDP fell 11% and industrial production fell 32%, making it the third-worst US recession in the 20th century (after 1929-32 and 1920-21).

The recession is often attributed to a tightening of fiscal and monetary policy. Christina Romer (2009) and others have argued that it is relevant to today’s situation because it illustrates the dangers of a premature withdrawal of stimulus when the economy is still weak.

But the recession remains somewhat of a mystery because the two most frequently mentioned causes – the reduction in the fiscal deficit and the Federal Reserve’s decision to double reserve requirements – do not appear to have been powerful enough to generate a recession of the magnitude seen. For example, Romer (1992) herself has argued that “it would be very difficult” to attribute much of the decline in output to changes in fiscal policy.1 And most studies of the Fed’s doubling of reserve requirements – most recently, Calomiris et al (2011) – have concluded that it had little impact on banks because they held abundant excess reserves, which they did not seek to rebuild after the new requirements took effect.

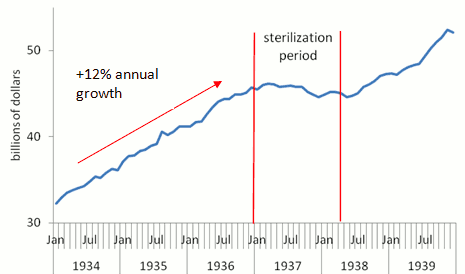

If fiscal retrenchment and higher reserve requirements cannot fully explain the recession, then what can? There is no doubt that there was a severe monetary shock. As Figure 1 shows, the money supply (M2) grew at a consistent rate of about 12% a year from 1934 to 1936, but then suddenly stopped growing in early 1937 and even fell later in the year. The monetary shock, however, was not the Federal Reserve’s decision to increase reserve requirements, but the often overlooked Treasury Department decision to sterilise all gold inflows starting in December 1936.

Figure 1. US money supply (M2), 1934-39

When the dollar was re-pegged to gold at $35 per oz. in January 1934, the US essentially went back on a gold standard. Gold reserves constituted 85% of the monetary base and changes in those reserves accounted for most of the changes in the monetary base. Because the US received large gold inflows in the mid-1930s, monetary policy was expansionary. This was the primary reason for the economic recovery (Romer 1992).

But when the Roosevelt administration began to worry about the potential for higher inflation, the Treasury Department decided to sterilise all gold inflows starting in December 1936. In essence, its new gold holdings were held in an inactive account rather than with the Federal Reserve, where it would have become part of the monetary base and money supply. Thus, instead of allowing the monetary base to grow with the inflow of gold, the monetary base was essentially frozen at its existing level.

The economy faltered in the spring of 1937 and tanked in the autumn of 1937. In February 1938, having realised its error, the Treasury ended its policy. In April 1938, the Treasury implemented its exit strategy and began desterilising its inactive gold holdings. The economy began to recover in June 1938.

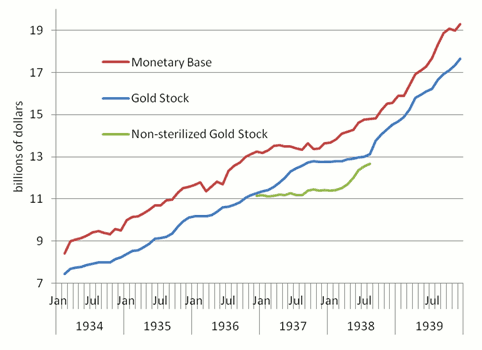

The effect of the gold sterilisation policy on the monetary base is shown in Figure 2. The gold stock and monetary base grew consistently from 1934 to 1936. Although gold stocks continued to grow in 1937, the monetary base flatlined because of the sterilisation. The non-sterilised gold stock is flat until the Treasury began desterilising its gold holdings in April 1938.

Figure 2. US monetary base and gold stock, 1934-39

The impact of gold sterilisation and higher reserve requirements on the money supply can be separated by noting that gold sterilisation affects the monetary base while reserve requirements affect the money multiplier. In a recent paper (Irwin 2012), I find that changes in the monetary base were much more important than changes in the money multiplier in explaining the abrupt end to the growth of the money supply in 1937.

Notice also that gold inflows into the US essentially ceased in late 1937 until mid-1938. The sudden halt to gold inflows was due in part to fears that the Roosevelt administration would respond to the recession by devaluing the dollar, just as it had done in response to the Great Depression in early 1933. (Fool me once, shame on you, fool me twice, shame on me, seems to have been the view of financial markets.) However, gold began surging back into the US in September 1938 when Hitler’s territorial demands on Czechoslovakia (the Munich crisis) set off fears of a European war.

If we are to avoid the mistakes of the past, it is important to have an accurate assessment of what those past mistakes were. The severity of the Recession of 1937-38 was not due to contractionary fiscal policy or higher reserve requirements. By contrast, the policy tightening associated with gold sterilisation was not modest – it did not simply reduce the growth of the monetary base by a few percentage points, it stopped its growth altogether. While the Federal Reserve is often blamed for its poor policy choices during the Great Depression, the Treasury Department was responsible for this particular policy error.

The recession of 1937-38 occurred long ago, but it does have policy lessons for today. It suggests that, in a weak recovery, a pre-emptive monetary strike against inflation (which was very low at the time, as it is today) is capable of producing a devastating recession.

References

•Brown, E Cary (1956), “Fiscal Policy in the ‘Thirties: A Reappraisal”, American Economic Review, 46: 857-879.

•Calomiris, Charles W, Joseph Mason, and David Wheelock (2011), “Did Doubling Reserve Requirements Cause the Recession of 1937-1938? A Microeconomic Approach”, NBER Working Paper No. 16688, January.

•Irwin, Douglas A (2011), “Gold Sterilization and Recession of 1937-38”, Working paper.

•Romer, Christina D (1992), “What Ended the Great Depression?”, Journal of Economic History,52:757-784.

•Romer, Christina D (2009), “The Lessons of 1937”, The Economist, 18 June.

_______________

1 A famous paper by E. Cary Brown (1956) finds that the fiscal changes explain less than a quarter of the downturn.

![]()

Leave a Reply