The current wave of monetary expansion by central banks has reignited calls for a return to the gold standard. But would this monetary system work today? This column argues that it probably would not. The successful pre-1914 gold standard was based a very peculiar gold-market microstructure, which provided central bankers with non-negligible discretionary power. Such microstructural foundations would be neither replicable nor desirable today.

The gold standard is an evergreen in monetary-policy debates. The current expansionist stance adopted by central banks has provoked its return to centre stage (see e.g. Harrison 2013):

- Admirers of the gold standard depict it as a self-regulating and transparent system, credibly anchoring the value of money to the price of an inherently sound asset (see e.g. Bordo and Redish 2013).

- Thus, the recent substantial drop in gold prices has appeared somewhat shocking to many.

The gold market today

At a time of massive liquidity injections by central banks, gold should be a one-way bet. Yet that hasn’t been the case in recent months, when gold lost nearly one quarter of its value. In order to explain this puzzling phenomenon, fundamental changes in the nature of the gold market have been evoked. In fact, today’s gold market has become entirely driven by derivative trade, not by physical orders (Kaminska 2013). As a result, valuation appears to have completely divorced from fundamentals, so that gold itself has turned from a commodity to ‘a brand’ (El-Erian 2013).

What microstructure for a restored gold standard?

All this suggests that the microstructure of the gold market plays a crucial role in determining the financial properties enjoyed by this asset. Therefore, it is legitimate to wonder what kind of gold-market microstructure should be attached to a restored gold standard in order for the system to work efficiently. The question is less straightforward than it might seem at first sight.

Proponents of the gold standard imagine it alongside a central bank that buys and sells physical gold at a fixed spot price, so that market prices cannot deviate from official ones. Yet historically, the gold standard did not actually feature fully fixed gold prices, but bands of fluctuation constraining market prices (see Hotson 2013 for a long-term view). A parallel can be drawn with fixed-exchange-rate regimes, which have not generally featured fully fixed exchange rates but ‘target zones’. In fact, the existence of these bands of fluctuation provided central bankers with some room for discretion in the conduct of monetary policy (Svensson 1994). In the light of historical precedents, how should central bank intervention in the gold market be designed in order to be successful?

The microstructure of the classical gold standard

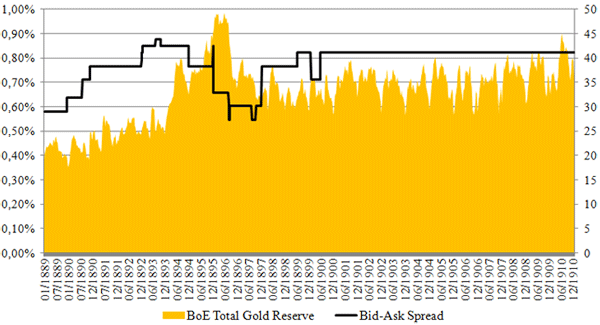

Given the deceptive performance of the interwar gold standard, looking for successful central-bank intervention in the gold market inevitably means going back to the pre-1914 international monetary system. This system emerged ‘spontaneously’ in the 1870s around the UK’s national gold standard, which had been established in 1821 (Bordo and Redish 2013). Because of this historical lead and because of Britain’s close commercial ties to gold-producing countries, London was already host to the world’s gold market when the international gold standard became a matter of fact. In a recent paper (Ugolini 2012), I analyse the microstructure of this market. I find that it basically was a spot market (forward transactions were not yet standardised), featuring one market-maker of last resort (the Bank of England). By modifying its bid and ask prices for gold, the Bank attempted to maintain its inventories (i.e. its gold reserves) at an optimal level. Microstructure theory suggests that bid-ask spreads can be interpreted as an indicator of the degree of suboptimality of the market-maker’s inventories (Stoll 1978). Figure 1 shows that the Bank’s bid-ask spread actually increased in times of monetary tension (the Baring crisis, the Boer War). Interestingly, they remained fairly high after 1900: this may be interpreted as evidence of the Bank’s difficulties in maintaining adequate gold reserves.

Figure 1. Bank of England’s bid-ask spreads for gold (in percentage, left scale) and total gold reserves (in million pounds, right scale)

Source: Ugolini (2012).

A self-regulating, transparent system?

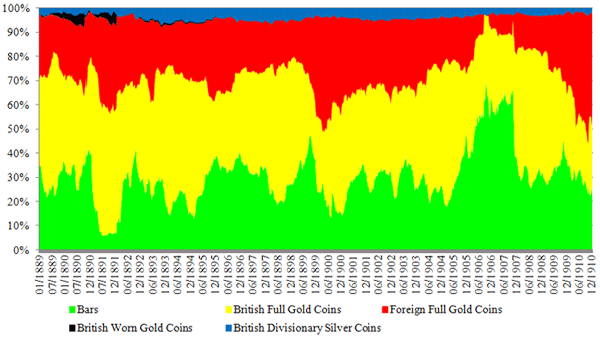

Archival evidence suggests that the Bank of England struggled to perform its role as gold market-maker of last resort. In particular, the Bank heavily resorted to ‘unconventional’ gold policy – i.e., offering a higher bid price for foreign-minted gold coins in order to attract them directly from other countries’ circulation. Figure 2 shows to what extent ‘unconventional’ gold items compensated for shortages of ‘conventional’ ones: in some periods, foreign coins rose to more than a half of total gold reserves. Note that the composition of reserves was undisclosed, so that the public did not know how much of them consisted of ‘unconventional’ gold items – into which the Bank was not allowed to convert its banknotes.

The discretionary power left to central bankers in the conduct of gold policy allowed them to smooth the functioning of the international monetary system by easing gold coin arbitrage between countries. When the gold standard was re-established in 1925, these margins for flexibility had disappeared: gold coins no longer circulated in any country, and the Bank of England’s bid-ask spreads were fixed by law at 0.16% only. It is tempting to speculate that this was one of the reasons that the interwar gold standard failed to work as smoothly as the pre-war one.

Figure 2. Composition of Bank of England gold reserves, by kind of asset (in percentage)

Source: Ugolini (2012).

Conclusions: The devil is in the details

My findings are in line with the conclusions of that branch of the literature which has long maintained that the pre-1914 international gold standard was far from self-regulating and transparent. But this literature also brings in an innovative element: the system was based on very peculiar microstructural foundations. Such preconditions would not only be hardly replicable, but also probably undesirable today.

Would a restored gold standard actually work in the context of today’s gold markets, instead? An answer to this question may perhaps be found by drawing a parallel with the fate experienced by fixed-exchange-rate arrangements. Over the last decades, the microstructure of major currency markets has evolved in such a way that the fixing of prices has become an extremely complex process (Lyons 2001). This has prompted major central banks to give up exchange rate targets, either by switching to inflation targeting or by resorting to monetary unification. It is difficult to see how central banks’ intervention in a sophisticated gold market might be more successful than foreign exchange intervention has been. If some solution to the ailments of the international monetary system is to be found, it should definitely be searched for elsewhere.

References

•Bordo, Michael, and Angela Redish (2013), “Putting the ‘System’ in the International Monetary System”, VoxEU.org, 20 June.

•El-Erian, Mohamed (2013), “We Should Listen to What Gold Is Really Telling Us”, Financial Times, 20 May.

•Harrison, Mark (2013), “Is the Gold Standard as Good as It Sounds?”, Financial Times, 16 June.

•Hotson, Anthony (2013), “Currency Stabilisation and Asset-Price Anchors: An Examination of Medieval Monetary Practices with Some Implications for Modern Policy”, VoxEU.org, 23 April.

•Lyons, Richard (2001), The Microstructure Approach to Exchange Rates, MIT Press.

•Kaminska, Izabella (2013), “Gold as Collateral, Not Stock”, FT Alphaville Blog, 1 May.

•Stoll, Hans (1978), “The Supply of Dealer Services in Securities Markets”, Journal of Finance 33:4, 1133-51.

•Svensson, Lars (1994), “Why Exchange Rate Bands? Monetary Independence in Spite of Fixed Exchange Rates”, Journal of Monetary Economics 33:1, 157-99.

•Ugolini, Stefano (2012), “The Bank of England as the World Gold Market-Maker during the Classical Gold Standard Era, 1889-1910”, Norges Bank Working Paper 2012/15.

![]()

Leave a Reply