Today former Federal Reserve Chairman Paul Volker pulled out the specter of the 1970’s to rail against those suggesting room for a higher inflation target, holding special contempt for the obviously insidious President of the Chicago Federal Reserve Charles Evans:

So now we are beginning to hear murmurings about the possible invigorating effects of “just a little inflation.” Perhaps 4 or 5 percent a year would be just the thing to deal with the overhang of debt and encourage the “animal spirits” of business, or so the argument goes.

It’s not yet a full-throated chorus. But remarkably, at least one member of the Fed’s policy making committee recently departed from the price-stability script.

Not so remarkably given that this idea has been making the rounds for some time – Olivier Blanchard suggested a 4% inflation target early last year, and Greg Mankiw wrote this in early 2009:

Having the central bank embrace inflation would shock economists and Fed watchers who view price stability as the foremost goal of monetary policy. But there are worse things than inflation. And guess what? We have them today. A little more inflation might be preferable to rising unemployment or a series of fiscal measures that pile on debt bequeathed to future generations.

Of course, Volker’s amazement that someone might suggest a higher inflation target is a consequence of his conviction that the 1970’s was the worst economic decade ever:

…Economic circumstances and the limitations on orthodox policies are indeed frustrating. After all, if 1 or 2 percent inflation is O.K. and has not raised inflationary expectations — as the Fed and most central banks believe — why not 3 or 4 or even more? Let’s try to get business to jump the gun and invest now in the expectation of higher prices later, and raise housing prices (presumably commodities and gold, too) and maybe wages will follow. If the dollar is weakened, that’s a good thing; it might even help close the trade deficit. And of course, as soon as the economy expands sufficiently, we will promptly return to price stability…

…Some mathematical models spawned in academic seminars might support this scenario. But all of our economic history says it won’t work that way. I thought we learned that lesson in the 1970s. That’s when the word stagflation was invented to describe a truly ugly combination of rising inflation and stunted growth…

…It is precisely the common experience with this inflation dynamic that has led central banks around the world to place prime importance on price stability. They do so not at the expense of a strong productive economy. They do it because experience confirms that price stability — and the expectation of that stability — is a key element in keeping interest rates low and sustaining a strong, expanding, fully employed economy.

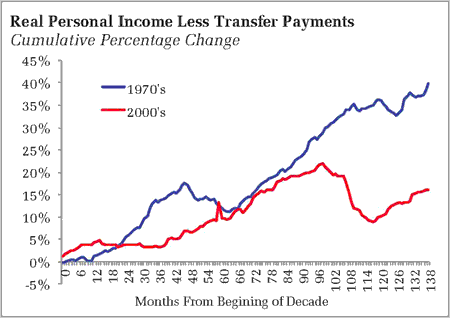

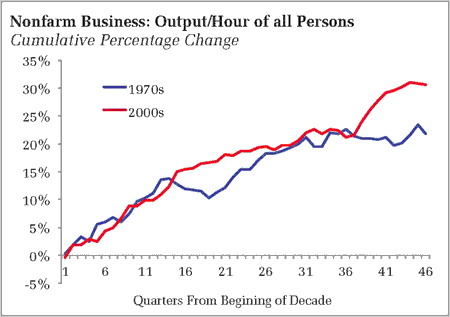

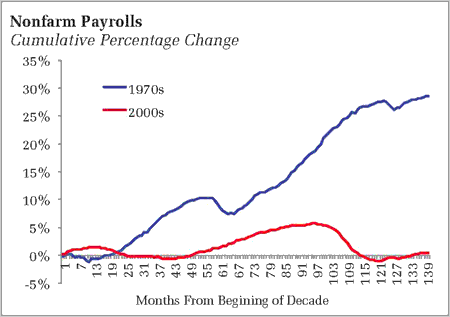

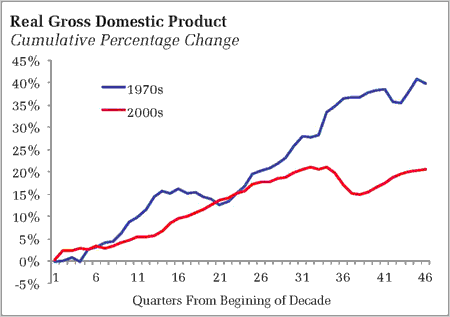

Note the conviction that high inflation is not compatible with strong growth. Now take a quick look at some of the economic outcomes of periods beginning with 1970 and 2000:

I don’t want to romanticize the 1970s. I think we all recognize that the 2.5% unemployment rate at the end of the 1960’s was below the natural rate and thus incompatible with low inflation. The subsequent decade of economic mismanagement did permit both inflation and unemployment to rise, although certainly some of the latter can be attributed to the unusually low unemployment at the beginning of the decade. That said, the above numbers stack up pretty impressively compared to the 2000s. Arguably in recent years productivity did accelerate, at least temporarily, but didn’t appear to translate into better job or wage growth. But overall, I am thinking the inflationary 1970s look pretty good right now relative to the price stability of the last decade.

Of course, in the background, the unexpected inflation of the 1970s drove a redistribution of wealth, and it is this that is probably Volker’s real complaint. My first undergraduate economics professor told a story of how all the student loans he took out in the late 60s and early 70s evaporated in real terms a decade later. Perhaps Volker would have preferred that he had been weighed down by those debts instead – a situation not unlike today, were the debt overhang is a weight on household spending.

What is even more sad is that Volker fails to recognize why some argue for higher inflation:

My point is not that we are on the edge today of serious inflation, which is unlikely if the Fed remains vigilant. Rather, the danger is that if, in desperation, we turn to deliberately seeking inflation to solve real problems — our economic imbalances, sluggish productivity, and excessive leverage — we would soon find that a little inflation doesn’t work. Then the instinct will be to do a little more — a seemingly temporary and “reasonable” 4 percent becomes 5, and then 6 and so on.

I don’t think I have heard anyone who believes that inflation is a cure to sluggish productivity. Indeed, see above – during the recession productivity was anything but sluggish. No one thinks that higher inflation will spark higher productivity, only that higher inflation can be a tool to lift the economy from the lower bound allowing output to rise to the productivity-enhance level of potential output. Excessive leverage is a real problem, and in fact one that can be addressed via inflation. A commenter on an earlier piece notes that even what I perceive as lower levels of inflation could quickly erode the debt overhang, albeit not as quickly as I might like. How a central banker cannot recognize that unanticipated inflation erodes real debt loads is simply unfathomable.

And Volker uses the general term “economic imbalances,” but offers no explanation to what he is referring. Arguably, the major economic imbalance is the foreign central bank-induced trade deficit, which has contributed to a global imbalance in patterns of production and consumption. Recall that he appears to recognize the role of the Dollar in any rebalancing:

If the dollar is weakened, that’s a good thing; it might even help close the trade deficit.

But seems to lose sight of this later:

At a time when foreign countries own trillions of our dollars, when we are dependent on borrowing still more abroad, and when the whole world counts on the dollar’s maintaining its purchasing power, taking on the risks of deliberately promoting inflation would be simply irresponsible.

I thought the purpose of the Federal Reserve was to promote the economic interest of the United States – that is its primary responsibility. And how can any economic imbalances be resolved if we remain dependent on borrowing from abroad? Wouldn’t we be better off discouraging those capital flows and allowing for export and import-competing industries to expand? And wouldn’t the rest of the world be better off if the US helped ease their inflationary pressures by providing additional goods and services to the global economy rather than attempting to absorb the excessive production of other nations? (And if you believe that those capital inflows represent confidence in the US economy, I have a bridge to sell you. Take out the purchases by foreign central banks and see what happens.)

Bottom Line: The constant comparisons to the 1970s are increasingly tiresome. At the end of the day, in the 1970s we were not in a liquidity trap. Today we are. The world is simply different. And we need policymakers that recognize that difference, not dinosaurs who refuse to do anything but live in a narrow view of their youth.

I think Tim Duy is letting his emotions and his psychological baggage dictate his respect for history. I am a GenXer, and while I was just a baby during the 70s, I see everyday on the streets of the city where I live people of my generation and younger discounting and tiring themselves of the older generation. It is all due to their own psycho problems growing up and their perception of those older than them. Anyone with a brain, a respect for history, and a competency in economics knows deep down inside that encouraging inflation – even if *only* 4-5% would be a disaster for this economy. Go ahead, cause inflation – and economic disparity will rise even more, we´ll need to raise more taxes and transfer payments will intensify. What we need is price stability or deflation. Tim Duy is a psycho idiot.

Part 2 – I forgot to mention that in this technologically fueled fast evolving economy speed is everything, unlike the 70s. Tim Duy is probably feeling unfulfilled and would probably benefit at an accelerated rate the bounty of higher inflation. He is probably well-positioned for it. But what about those who are not? Self-interest rules the mind of Tim Duy.