Is the Fed responsible for the pernicious low-interest rate environment? Yes, but not for the reasons you think. I explain why in a new National Review article:

While this absolves the Fed of direct responsibility for the low-interest-rate environment, it does not absolve it for its indirect influence. Through its control of the monetary base, the Fed can shape expectations of the future path of current-dollar or nominal spending. Thus, for every spike in broad money demand, the Fed could have responded in a systematic manner to prevent the spike from depressing both spending and interest rates. In other words, the Fed could have adopted a monetary-policy rule that would have committed it to maintaining stable growth of total-dollar spending no matter what happened to money demand. A promise from the Fed to do “whatever it takes” to maintain stable nominal-spending growth would have done much by itself to prevent the money-demand spikes from emerging at all. Why hold a greater number of safe, liquid assets if you believe the Fed will keep the dollar value of the economy stable?

[…]The Fed’s failure to adopt something like a nominal-GDP target in 2008 meant that the central bank would not be able to adequately respond to the subsequent money-demand shocks that arose over the next four years. That is, the Fed’s inaction allowed the pernicious low-interest-rate environment to develop. So while the Fed did not directly cause the low-interest-rate environment, our central bank allowed it and all of its associated problems to emerge. For that it should be blamed.

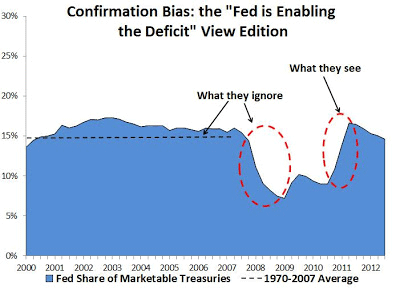

Readers of this blog will be familiar with this argument (e.g. see here, here, and here). Here are some figures that corroborate the points made in my article. First,the figure below shows the Fed’s share of treasuries over the past twelve years. It has been overall relatively stable around 15%. Observers who blame the Fed for pushing down treasury yields, though, often note the Fed’s relatively large share of treasury purchases in 2011. What they ignore is the Fed also sold a similar proportion in 2007-2008. By their logic the Fed should have caused treasury yields to rise during this time. But this period is when the long decline in treasury yields actually begins.

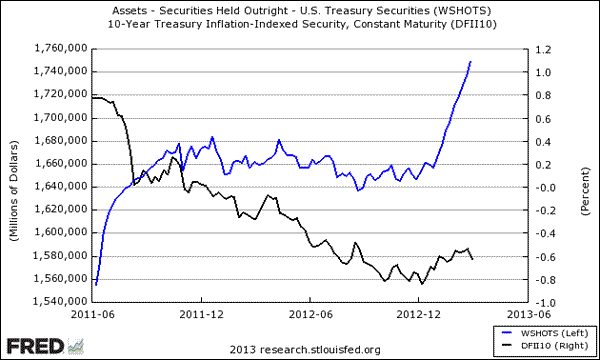

When confronted this fact, some of these critics will then point to long-term treasury yields and say the market is “front-running” the Fed stated plans to buy long-term treasuries. But if that is the explanation for the falling long-term yields then this next figure should not be possible. It shows the Fed’s treasury holdings were relatively stable between the end of QE2 in mid-2011 and the beginning of QE3 in late 2012. It also shows that real interest rates on 10-year treasuries continued to fall. There was no front-running during this time since there were no QE programs. There were, however, ongoing global economic problems that can explain the decline.

Finally, it is worth pointing out that as the U.S. economic recovery has begun to appear more firm, long-term treasury rates have also started to gradually rise. The Fed has not changed its pace, but yields are now rising. The easiest explanation is that the long-term yields are directly reflecting the expected state of the economy. Indirectly, though, the rising yields can be traced in part to the Fed actions which under QE3 has become more closely to tied to the state of the economy. Too bad it took the Fed almost four years to get here.

Leave a Reply