Goldman Sachs is upgrading U.S. Steel Group (NYSE:X) to Buy from Neutral with a 6-month price target of $75 (prev. $61) representing upside of $28%.

Firm notes they believe that rising steel prices and increasingly positive leading indicators of demand are pointing to a steel industry that should see its earnings markedly improve in near to medium terms. With a high leverage to steel prices and demand, and one of the best cost positions on the raw materials, they see potentially significant upside to US Steel’s share price.

Goldman believes that markets’ concerns about recent dip in scrap prices are over done. The domestic steel prices should get strong support from rising global steel cost curve, which in turn should push global steel prices further up. We see companies with vertical integration into raw materials as the best investment option in this environment. US Steel, thus fits the best among our coverage. Additionally, its high fixed cost structure (or high leverage to rising utilization rate) puts it in an advantage as steel demand and thus the utilization rate are expected to continue to rise in coming months. They estimate US Steel’s utilization rate to rise to 85% in 2011 from 76% in 2010.

US Steel’s earnings have suffered and the company has struggled to generate profits as the utilization rate has remained below optimal level. As both prices and production rates are rising, its favorable cost structure on raw materials provide it relatively better opportunity than its peers to generate strong earnings.

US Steel’s iron ore costs in the US is less than $65 per tonne (vs. current global spot price of $191 per tonne) and its 2011 coking coal contract price is set at about $200 per tonne (vs. current global spot price of $312 per tonne). These favorable input costs imply that as utilization rate rise and fixed costs are spread over higher tonnage, X should have one of the highest leverage to improving conditions.

But scrap price is falling, shouldn’t steel follow

An obvious risk in this scenario is the scrap price. In recent months, it was rising scrap prices that heralded in the current round of price increases. This was exacerbated by a seasonal uptick in demand. Once the weather improves and scrap flow into the yards increases, scrap prices usually fall. That said, the firm believes that the market is missing the point that although raw material prices have been the primary source of rising steel pries, demand (both real and apparent) has also strengthened and thus they see less risk from a modest dip in scrap prices, at least in the near term

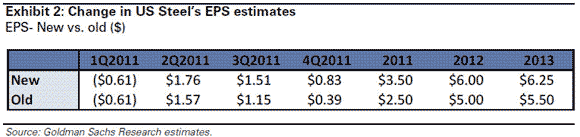

– Goldman still expects the 1Q2011 loss at $0.61 for X due to the lag in contract prices as compared to the spot prices but consider this as a timing issue.

The same contracts will help US Steel sustain earnings beyond 1Q. Goldman now expects higher shipment volume (an increase of 13% year over year vs. 9% earlier) with estimate of the utilization rate of 85% (up from 82% earlier) for US Steel’s Domestic Flat Rolled division. This should help offset some of the fixed costs per ton. They are also lowering their coking coal cost for US Steel to $185 per ton from $200 they had estimated earlier. This is in line with the guidance provided by the company in its 4Q conference call. As such Goldman’s 2011 estimates have moved up to $3.50 from $2.50.

They are also raising their 2012 and 2013 estimates on higher than expected utilization rate and hence higher shipment volume, particularly for its Flat Rolled Division.

Notablecalls: Goldman is essentially saying Tanners, the UBS analyst is wrong on her Scrap Steel call. Tanners left a 5% dent on the space but looks like the shorts are now trapped as the group is back to its highs.

X may see $63 level today on this call, I suspect. Let’s see how it goes.

Leave a Reply