Skystar Bio-Pharmaceutical (SKBI) announced a record-setting quarter in November, which led to sharp estimate increases.

Shares now have a Zacks #1 Rank (Strong Buy) and the dirt-cheap valuations show potential for huge returns.

Company Description

Skystar develops and makes veterinary and medical care products and is based in China. Over 170 products are spread though out 4 divisions; veterinary medicines, micro-organisms, vaccines and feed additives.

Record Revenues

Skystar announced third-quarter results on Nov 16 that showed record organic revenue of $18.5 million, which is up 45%. Margins improved slightly from 52% to 54%. The company’s balance sheet is quite liquid with $41.1 million in current assets compared to just $9.1 million in current liabilities.

Earnings per share came in at 93 cents, which was about double the 47 cents the sole covering analyst was expecting. This was the company’s third consecutive earnings surprise

Outlook Jumps

While we only have 1 covering analyst that reports to Zacks, that analyst has become even more bullish on the earnings news. The estimate for the last quarter of 2010 is up 13 cents, to 57 cents.

Next year’s projection is up 44 cents, to $2.25. Last year Skystar made $1.62 which means annual forecasted growth rates are 22% and 14%, respectively.

China Raises Interest Rate

Over the Christmas weekend China raised its interest rate a quarter point. While this was likely the first of many moves to tighten the monetary supply and reign in prices, the extremely cheap valuations still make Skystar attractive.

The P/E ratios are in the low single digits and the PEG is only 0.7. Given the low capitalization, under $70 million, the P/S is definitely worth noting. While trading at 1.4 times sales is not that great, it is in line with the peer group.

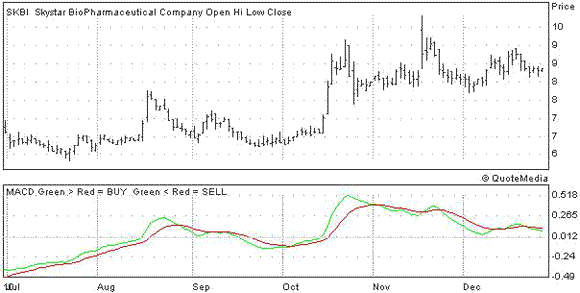

The Chart

You can see below that this is far from a smooth ride, but given the growth rates, valuations and potential for the region, SKBI could post some outsized returns.

Leave a Reply