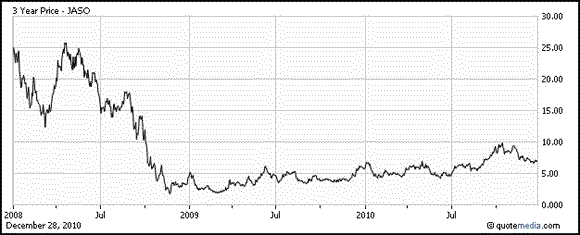

The solar sector has been highly volatile in 2010. JA Solar Holdings Co. (JASO) has seen its shares battered this year but with strong growth projections and cheap valuations it is trading with a PEG ratio of just 0.4.

China-based JA Solar manufactures solar cells which are then sold to solar module manufacturers who assemble the solar cells into the modules.

It has 2 main solar cell manufacturing facilities in Hubei Province and Jiangsu Province. It also has a module factory in Shanghai.

Record Quarter in Third Quarter of 2010

So far, the 2010 results have been strong. On Nov 9, JA Solar reported its third quarter results and saw a record quarter across nearly all metrics including revenue, net income, earnings per share and shipment volume.

It surprised on the Zacks Consensus by 47.1% as earnings per share were 50 cents compared with the consensus of 34 cents. The company made just 18 cents in the third quarter a year ago.

Revenue soared 174.3% to a third quarter record of $541 million from $197.2 million in the third quarter of 2009. This was also a 52% increase over the second quarter.

Shipments were a record at 418MW, well above the company’s guidance of 375MW.

JA Solar’s customer base is diversifying. Sales to international customers were 53% of total revenue in the quarter, up from 46% in the second quarter and up from 23% in the same quarter a year ago.

Full Year Shipment Guidance Raised

JA Solar continues to see strong demand and good visibility regarding the fourth quarter. For that reason it raised its full year shipment guidance to an excess of 1.45GW from 1.35GW.

Shipments in the fourth quarter are projected to be about 450MW.

Analysts Cautious About 2011

JA Solar had a rough 2009 on its way to losing 12 cents per share. The 2010 Zacks Consensus is up 22 cents to $1.33 per share in the last 60 days. This is earnings growth of 1211%.

But the earnings machine is expected to grind to a virtual halt in 2011. While the 2011 Zacks Consensus Estimate has moved higher by 20 cents to $1.41 in the last 2 months, this is earnings growth of just 6%.

JA Solar is scheduled to report fourth quarter results on Feb 10, 2011.

Shares Are Dirt Cheap

While JA Solar has rebounded from its financial crisis lows in the past year, recently the stock has traded lower once again on fears of oversupply in Europe.

That means shares have gotten even cheaper. JA Solar is now trading with a forward P/E of just 5.2.

That is right in the mix with several of its peers. LDK Solar (LDK) has a forward P/E of 6.0. China Sunergy (CSUN) trades at 4.1x. Canadian Solar’s (CSIQ) forward P/E is the highest of the group at 10.2x. But all of them are under the S&P 500 average of 15.2.

JA Solar also has other attractive value characteristics. Its price-to-book ratio is just 1.3, well within the range of a value stock.

The company also has a stellar return on equity (ROE) of 22.1%, above its peers at 16.2%.

JA Solar is a Zacks #1 Rank (strong buy) stock.

Leave a Reply