New home sales in November rose by 5.5% from October, but that puts them at a dismal rate of 290,000. The percentage increase is a bit exaggerated as well, since the October numbers were revised down to 275,000 from 283,000. Thus relative to where we thought we were, the increase is more like 2.5%.

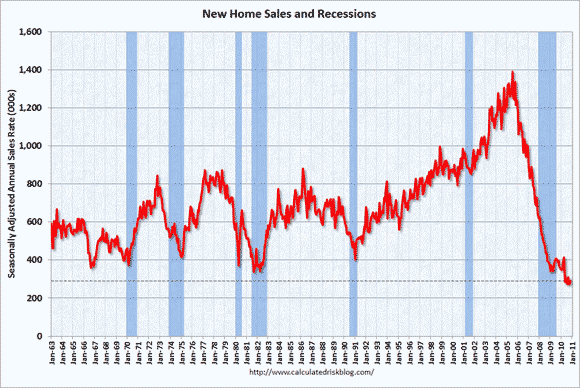

The seven lowest months on record (back to 1963) for new home sales have all been in the last seven months. About the only good thing you can say about this report is that it was not the absolutely worst month on record. That dubious honor is still held by August 2010, with a seasonally adjusted annual rate of 274,000.

Relative to a year ago, sales are down 21.2%. It’s not like a year ago was a great time in the homebuilding industry, either. Relative to the peak of the housing bubble (July 2005) new home sales are down 78.8%.

The very low May sales rate (282,000) was due to the end of the homebuyer tax credit. New home sales are recorded when the contract is signed, not at closing, as is the case with used home sales. Thus the post-tax credit hangover came in May for new home sales, not July, as was the case for existing home sales. That effect should have long ago worn off, so you can not attribute the weakness to the temporary distorting effect of the tax credit.

The graph below (from http://www.calculatedriskblog.com) shows the history of new homes sales. Keep in mind that the population of the country has almost doubled since the early 1960’s.

Take a very close look at the relationship between new home sales and the blue recession bars. New home sales fall sharply before all recessions (with the exception of the dot.com bust caused recession of 2001) and then start to increase sharply in the middle of, or towards the end of, the recession. That clearly is not happening this time around.

If you want to know why the recovery has been anemic so far, look no further than the graph above! New home sales are vital to the overall economy. If new homes are not selling, then home builders have no reason to build more of them. After all, that is very expensive inventory to sit on.

Each new home built creates a huge amount of economic activity. Not only are low new home sales bad for the big homebuilders like D.R. Horton (DHI), they are also bad for all the companies that make the products and supplies that go into making a new house. They range from Berkshire Hathaway (BRK.B) for bricks, roofing materials, and insulation to Fortune Brands (FO) for plumbing fixtures and cabinets to USG (USG) for wallboard to PPG Industries (PPG) for glass and paint to International Paper (IP) for lumber.

In terms of employment, it is not just all the roofers and framers who lose jobs due to weak new home sales, but employees at all the firms that make the stuff that goes into making a new home. Of course, if those employees are out of work, they are not spending on other goods and services dragging down a host of seemingly unrelated businesses. Not that the direct impact of construction jobs should be underestimated. Since the recession started, one out of every four jobs lost has come from the construction industry.

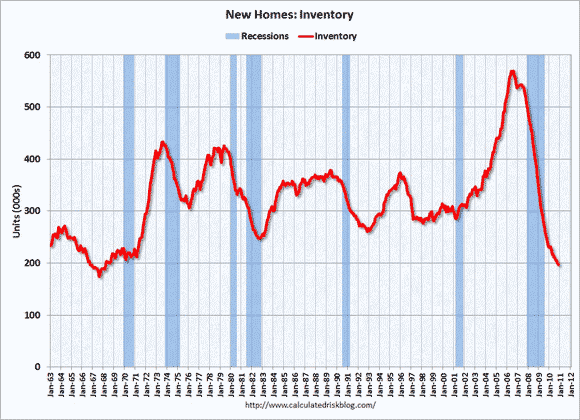

Inventories of new homes declined by 2.0% on the month and are down 16.5% from a year ago. In absolute terms, new home inventories are in very good shape, at the lowest levels since the late 1960’s. This can be seen in the second graph (from http://www.calculatedriskblog.com).

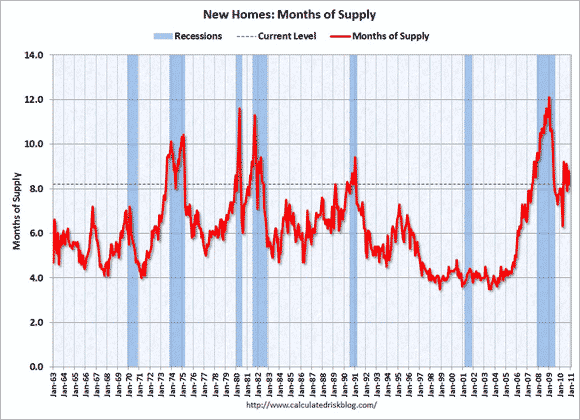

However, inventories must always be evaluated relative to how fast they are selling. The current rate puts the months of supply at 8.2 months, down from 8.8 months in October, but up from 7.7 months a year ago. While that is well off the peak of 12.0 months, it is still well above normal. A healthy market has about a six month supply of new houses, and during the bubble four months was the norm, as is shown in the graph below (from http://www.calculatedriskblog.com).

Of course, used homes are very good substitutes for new homes, and yesterday we found out that the months of supply for used homes was 9.5 months (see “Used Home Sales Rise Everywhere“). That means that prices of existing homes are going to continue to fall, making life even tougher.

Regionally, things were all over the map. New home sales in the West soared by 37.3% on the month but are down 16.5%% year over year. The South is the biggest and therefore most important of the Census regions when it comes to housing data it was up 5.8% on the month, but down 12.7% from a year ago.

Worst hit for both the month was the Northeast. There sales plunged 26.7% on the month and are off 29.0% from a year ago. Sales in the Midwest were off 13.3% from September and are down 53.5% from a year ago, easily making it the hardest hit on a year-over-year basis.

In Summation

Overall, this was a very depressing report. Not just in absolute terms, but it was also far below the consensus expectations of a 305,000 pace. Eventually, we will see a recovery in new home sales and thus homebuilding. However, first we have to clear out all the existing inventory overhang of both new and existing homes. That includes the shadow inventory of homes that have been foreclosed upon, or are about to be foreclosed on, but which are not yet listed for sale.

That remains a daunting task. On the other hand, a doubling in new home sales would bring us back to approximately the same level of sales we average in 1964 when the population was just 191 million, relative to today’s population of 310 million. When — not if, but when — that happens, the economy will be set to boom.

The main problem right now for housing demand is the very low rate of household formation. Instead of moving out to get their own place, people in their 20’s are being forced to live with Mom and Dad, since they don’t have a job that will pay the rent or support a mortgage. Since residential investment is such an important swing factor in creating jobs in the country (both directly and indirectly) that sets up a huge “chicken and the egg” problem.

We are not in a robust recovery yet, but the seeds have been planted. It is unlikely that they will germinate before next spring — and it may take longer than that — but eventually they will sprout.

Leave a Reply