Today’s bank system adheres to a very simple principle. When you want to borrow money, you promise the banker you will pay him back and with that promise the banker creates a balance for you. You owe interest on it.

Because so few people know how the system works, nearly nobody sees how – in an almost mechanical way – banking with thin air parasites society like a cancer tumor and reduces people to cogs to appease its financial hunger.

The European Central Bank (ECB) obliges bank to have 2 cents in reserve for each euro they owe to their customers. Our balances are now backed for a few percent by real money, the rest of the money does not exist. So we don’t have real money at the bank, but a balance, a promise of the banker that we can have real money for it, if we ask for it.

Banks borrow the real money from the ECB against securities. The real money is what we have in our purse. The real money is also used in cashless form in the payments between banks.

Customers have a balance, but that is not money with which they can pay. And they don’t pay with it. (Although everybody thinks he does.) They gave payment orders to their bank. The banks then change the balances and pay the amounts to each other. In the daily payment traffic between banks, all payments incoming and outgoing are crossed out against each other and at the end of the day only the differences are transferred. This way, with a tiny little bit of money, banks can pay millions to each other.

The borrower receives a balance from the bank and spends it. This way the balance arrives in another bank account. The receiver will spend it on something else and so the balance goes around in the society. And at the moment the borrower pays back his loan, the bank will reduce the amount from his balance. This way the created balance disappears again. Each time new loans have to be supplied to keep sufficient pseudo-money in circulation. If the quantity decreases, borrowers cannot pay back the banks anymore and the banks will fail massively.

But not all balances keep going around. There are also people who park a part of their balance in a savings account. Parked balances in savings account do not participate in the “money”-circulation anymore and to replace them, extra loans must be put into circulation. And of course, a part of these supplementary loans will also end up as parked savings. For all the loans, those parked and those in circulation, lenders must work to find the money to pay installments and interest. They cannot find that money in the savings accounts. That cannot be earned. So more and more installments and interest have to be paid out of the money that still goes round. In the end these sums would even exceed the money in circulation. The solution of the bankers? Still more loans!

If you keep the money in circulation growing at the same pace as the savings, there will always be enough money for paybacks and interest. That is why we have inflation. In the “money” in circulation the loans keep piling up.

The interest for the savers is paid by the borrowers. These are often enterprises like shops, wholesalers, transporters, producers, subcontractors and suppliers of services. They count the costs in the prices of their products. Ultimately, they are paid by the consumers. 35% of all prices consist of interest and that percentage is increasing all the time. [1]

The interest the savers receive comes, in first instance, as an extra balance from the hat of the banker and is added in the savings account. This interest too bears interest. At 3% interest the savings double in 24 years, at 4% in 18 years. The rich become richer faster and faster and meanwhile the 10% richest Europeans own 90% of all wealth.

With the continual growth of the pseudo-money mass, around 1970 the balances surpassed the Brute Internal Product. There was much more pseudo-money in circulation than needed for the normal economy. This lead to the development of a financial sector, in which money is earned with money, so with interest and blowing bubbles on the stock market. The bankers knew that in the long run it would become harder and harder to keep the “money”-growth going and to find trustworthy borrowers.

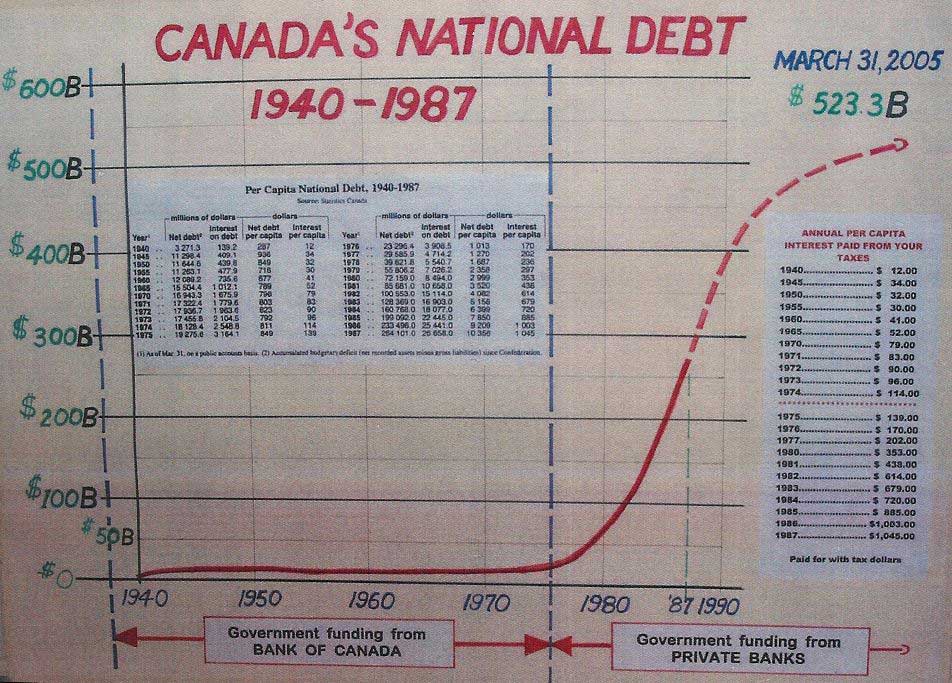

They succeeded in convincing governments it would be better when they would not borrow from their central banks anymore (which meant, in practice, borrowing without interest), but would borrow from commercial banks, so at interest. In all countries that agreed with it, the public debt grew exponentially. Not because these governments made more debts, but because of the interest on interest on the existing debt. [2]

(click to enlarge)

The governments had to cut budgets to face the growing interest burden. But there is no way to cut budgets against the working of an exponential growing interest. Governments had to privatize public services to pay off the debts. A long wave of privatizations followed, all of them big projects for which the banks could supply loans to private parties. Already in 1970 the Luxembourgian banker Pierre Werner presented the first blue print for the euro, that would give the banks the opportunity to supply loans in a much bigger area. Prominent economists warned that a common currency in an economically heterogeneous area would lead to big problems. They predicted, that countries with less possibilities for productivity, would be flooded by cheaper products from the most productive countries, like Germany. The enterprises in the weaker countries would fail, while the money would leave the country in payment of import products. [3] Exactly as it has turned out.

The weaker countries slide into debt and have no possibility to get out. The banks profit from these raising mountains of debts and roll off the risks on the tax payers. In 2012 the governments of the Euro zone together have founded the European Stability Mechanism (ESM), a bank with unlimited tax money as capital that will pay all losses money lenders will run in the weak countries.

The weaker countries slide into debt and have no possibility to get out. The banks profit from these raising mountains of debts and roll off the risks on the tax payers. In 2012 the governments of the Euro zone together have founded the European Stability Mechanism (ESM), a bank with unlimited tax money as capital that will pay all losses money lenders will run in the weak countries.

The solution of all these problems is as simple as its cause. We have to create a bank that is of all of us, a state bank with the exclusive right to create money. There must be a prohibition on creating balances out of thin air and on lending out balances. A state bank does not need capital and does not need profits. The interest can stay very low, or be compensated by fiscal measures. The interest flows back to the community. A money system with such a state bank does not need money growth, profitability growth, inflation, productivity growth, competition, exploitation and unemployment. When decided democratically, the government can take over the collective services again and execute them in the interest of the citizens. Also, investments can be directed to where such is desirable for society and not where the safest and fastest financial gains can be obtained. The government wont depend on the bankers anymore. The public debt will be of the past. Collectively we can turn to sustainability and well being, in stead of devouring, wasting and pressing out employees to please money-lenders.

We will have time and money left to erect a wax-statue museum, where we can preserve the money wolves and their political accomplices as a warning for future generations: beware of banksters!

Sources:

[1] Helmut Creutz & http://www.vlado-do.de/money/index.php.de[2] Ellen Brown: A tale of two monetary systems

[3] Out of the euro, and then? http://www.courtfool.info/en_Out_of_the_euro.htm

[4] See ESM-treaty articles 10.1 and 10.2

Leave a Reply