A common question about the recent large expansions in balance sheets among central bank in advanced economies is about the exit strategy. How easy will it be for central banks to go back to balance sheets of a size consistent with historical levels? Because the expansion of balance sheets represents a fairly unique historical experiment, it some times generates a debate and, at a minimum, uncertainty about how the process will work.

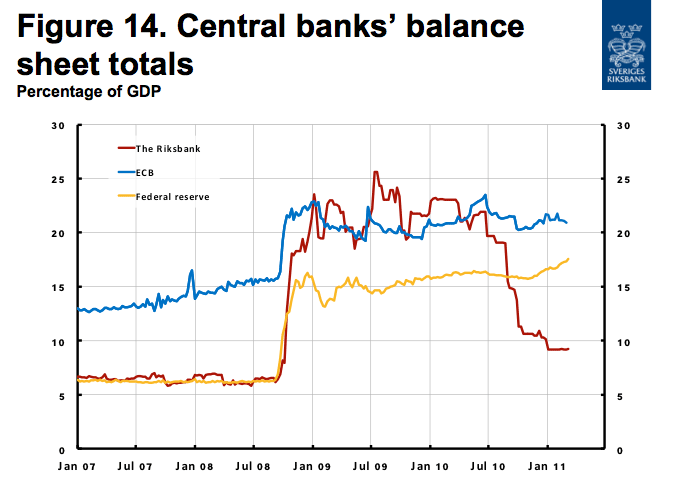

While it might not be an example for all advanced economies it is useful to point out that some central banks, such as Japan and Sweden have seen large declines in the size of their balance sheet in recent episodes (Japan in the mid-2000a, Sweden in the Fall of 2010) without any disturbance to the financial sector or interest rates. As an example, below is a picture borrowed from the Riksbank on the evolution of its balance sheet in comparison to the ECB and US Federal Reserve.

(click to enlarge)

The central bank of Sweden increased its balance sheet by a factor of 4 (from 5% of GDP to more than 20) in the Fall of 2008 mostly through an increase in loans to commercial banks. After the 2010 Summer, loans have been repaid at a very fast pace and we have witnessed over a very short period of time, just a couple of months, a reduction in the central bank balance sheet of more than 50%.

The exit strategy is likely to be different for other central banks that have relied more on asset purchases but it is useful to see a recent historical example of a large and quick reduction in the central bank balance sheet without negative consequences on financial or macroeconomic stability.

Leave a Reply