Most people refer to US business cycles in terms of the recessionary episodes identified by the NBER business cycle dating committee. Their dating of cycles which goes back to the original work of Burns and Mitchell in 1946 consists in identifying periods of “significant decline in economic activity” which are labelled recessions. When the economy is not in a recession we call it an expansion phase. Business cycles are the succession of expansions and recessions.

In the NBER characterization of cycles there is no mention of a recovery phase. The recovery phase starts the day the recession ends (what we call the trough) but there is no explicit discussion on how long or how fast the recovery is. The original work of Burns and Mitchell referred to a “revival” phase but this phase was never made explicit in the dating methodology of the NBER.

I just wrote a paper (with Ilian Mihov) that produces a date for the end of the recovery for US business cycles. We look at business cycles as a succession of three phases: expansions that are followed by recessions, which are followed by recoveries leading to the next expansion. Our expansion phase corresponds to the notion of an economy that is growing along its balanced growth path with a level of employment and output consistent with the notion of full employment. The recovery is the time that it takes for the economy to go back to full employment.

The task of producing those dates is not easy because it requires establishing a measure of full employment or equilibrium (if you are using an economic model). We go through several methods and establish the pros and cons of each of the methods. To our surprise we find that there are quite a lot of similarities across different methods and as long as some judgement is exercised reading the data, one can produce some reasonable dates for the end of the recoveries (the NBER business cycles dating committee also refers to the use of judgement to establish the recession dates).

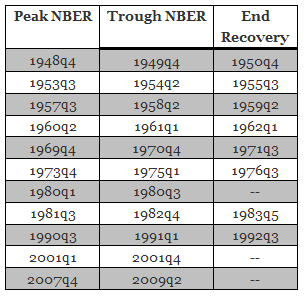

Below is a table with the end-of-recovery dates for each of the US business cycles after WWII.

The first column of this table is the quarter where an expansion ends (the beginning of a recession). The second column represents the end of the recession. These two dates are provided by the NBER. The third column is the innovation in our paper, the date when the recovery ends. As an example, in the fourth quarter of 1973 an expansion ended, a recession started. That recession ended (according to the NBER) in the first quarter of 1975. At that point the recovery started. This recovery finished in the third quarter of 1976 where an expansion phase takes over until the next recession in the first quarter of 1980.

There are three recessions for which we cannot provide an end-of-recovery date. The 1980q1 recession ended in 1980q3. But the recovery that started then was never completed because before the economy went back to full employment a new recession started (1981q3). The 2001q1 recession is a special one. It is very short and shallow and it difficult to identify a proper recovery — some argue that this does not constitute a recession — so we have decided not to provide a date for the end of this recovery at this point. And the 2007q4 recession that ended in 2009q2 has produced a slow recovery that is not over yet (it is far from being over according to our methods).

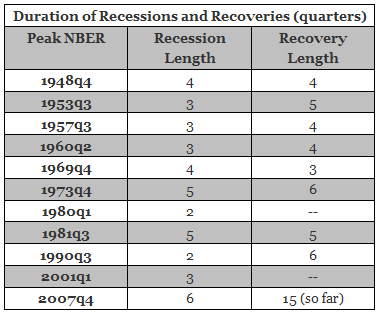

One way to summarize the evidence above is to look at the length of the recession and compare it to the length of the recovery as identified by out dates.

The first column of this table is the quarter where an expansion ends (the beginning of a recession). The second column represents the end of the recession. These two dates are provided by the NBER. The third column is the innovation in our paper, the date when the recovery ends. As an example, in the fourth quarter of 1973 an expansion ended, a recession started. That recession ended (according to the NBER) in the first quarter of 1975. At that point the recovery started. This recovery finished in the third quarter of 1976 where an expansion phase takes over until the next recession in the first quarter of 1980.

There are three recessions for which we cannot provide an end-of-recovery date. The 1980q1 recession ended in 1980q3. But the recovery that started then was never completed because before the economy went back to full employment a new recession started (1981q3). The 2001q1 recession is a special one. It is very short and shallow and it difficult to identify a proper recovery — some argue that this does not constitute a recession — so we have decided not to provide a date for the end of this recovery at this point. And the 2007q4 recession that ended in 2009q2 has produced a slow recovery that is not over yet (it is far from being over according to our methods).

One way to summarize the evidence above is to look at the length of the recession and compare it to the length of the recovery as identified by out dates.

Leave a Reply