Citigroup is out positive on Netflix (NASDAQ:NFLX) after their survey revealed surprisingly stable and improving customer satisfaction.

– Firm reiterates their Buy rating and $120 target.

Netflix remains one of the most controversial stocks they cover, Citi notes. It’s their “Screaming” Buy –they say “Buy,” people Scream. Risks here remain significant and include: a) Substantial Content Acquisition Requirements; b) Significant Competition; and c) Significant Uncertainty Re: NFLX’s International Investments. But they will stick with their Buy – highlighting what the firm views as a highly reasonable valuation, a generally positive execution track record, and the still early market opportunity for Internet Video Streaming. Three Updates:

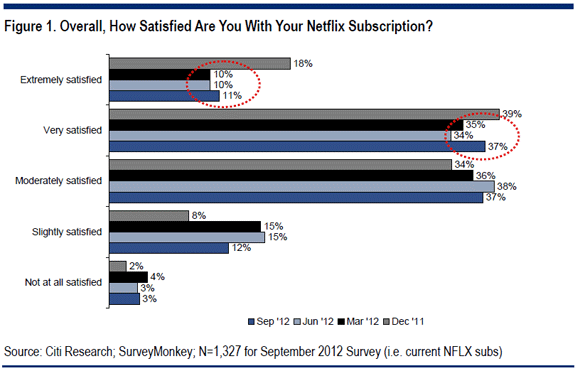

1. Latest Proprietary Consumer Survey Suggests Satisfaction Inflection Point — Citi very recently re-ran their consumer survey (approx 3,800 U.S. Internet users, incl. 1,200+ current & 700 past NFLX subs). Key Takes: 1) Overall customer satisfaction with Netflix has begun to improve for the first time since last Summer’s “Apocaflix” – 48% of current NFLX subs are Very or Extremely Satisfied vs. 44% to 45% levels observed in Q1 & Q2; 2) In terms of Online Video destinations, Netflix’s competitive position continues to rise – the % of respondents listing Netflix as a top destination has increased from 25% in Q2:11 to 30% in Q1:12 to 35% today – although YouTube and Amazon are also showing gains; 3) Churn propensity appears to have improved YTD – the % “Not At All Likely To Churn” has reached a YTD record high of 57%; and perhaps most surprisingly…4) The perceived Streaming content selection appears to have improved – 37% believe that Streaming content availability has improved over the last 12 months vs. only 16% who believe it has worsened.

2. Relatively Neutral Q3 Traffic Trends To Netflix.com — Per comScore, Netflix’s U.S. Website visitors have declined 3% Y/Y in Jul & Aug, or a less worse trend vs. Q2’s 7% decline. And, 12.4MM unique visitors visited Netflix via Smartphones in Jul & Aug. That’s 43% Mobile traffic penetration. And a bit of a reminder that as a subscription service, NFLX benefits from Mobile usage growth – better consumer value proposition with no drag on monetization.

3. The Valuation Case – They continue to see NFLX generating almost $5.50 in U.S. EPS in 2013. That means one can buy NFLX U.S. at 10X P/E, with a free call option on NFLX International. That’s highly reasonable, in Citi’s opinion.

Notablecalls: As many of you recall NFLX was a $200 stock when last summer’s Apocaflix began. Not saying the decline was solely due to Qwikster etc. but with subs starting to accept the reduced level of content offered by the company, the extreme negative sentiment toward NFLX stock may start to fade.

If churn goes down -> net adds go up. And that’s what people are looking for. That’s material new info that may actually show up next time NFLX reports.

There is always the issue with international expansion but if the U.S. ops can carry the weight while international moves toward profitability, NFLX may indeed become investable again. NFLX seems at least on track to add 6MM Domestic Streaming subs in ’12 off a 22MM base (that’s hard-to-match growth & size);

This call has a fair chance to generate some meaningful buy/cover interest in the stock n-t.

I’m thinking toward $60/share today.

Leave a Reply