The minutes of the July 31 – August 1 FOMC meeting are out. In my opinion, they reiterated the importance of the data flow in assessing the Fed’s next move.

The money quote was:

Many members judged that additional monetary accommodation would likely be warranted fairly soon unless incoming information pointed to a substantial and sustainable strengthening in the pace of the economic recovery.

At first blush, this can be taken to indicate that easing is imminent, as early as September, in direct contradiction to what I wrote yesterday. The key, however, is how have conditions changed since the last meeting? The next line in the FOMC minutes is:

Several members noted the benefits of accumulating further information that could help clarify the contours of the outlook for economic activity and inflation as well as the need for further policy action.

Recall that as we headed into this meeting, the data had turned particularly weak. The pace of job growth had fallen dramatically from the start of the year, retail sales were flattening out, and GDP growth had slowed to 1.5%. This data combined with the downside risks from Europe raised genuine concerns that more easing was necessary. But they held back, instead waiting to see how the data evolved.

Since then, the data have turned upward, much more consistent with the Fed’s medium-term forecast. The July employment report was stronger, retail sales picked up, and overall growth is looking stronger, with Goldman Sachs’ GDP tracking estimate rising to 2.3% for the third quarter. In addition, equity markets are on firmer ground as the crisis in Europe has at least temporarily receded. While certainly not exciting, the better tone of the data is palpable. I think the better data influenced Atlanta Federal Reserve President Dennis Lockhart to shift his language away from his dovish July comments. In short, I would argue that the data since the last FOMC meeting has in fact pointed toward an improvement in the pace of the recovery, which I think will pull the middle ground back from the brink of additional asset purchases.

That said, the doves can still make a pretty good case for additional easing, even given the improvement in the data flow. But enough to pull Federal Reserve Chairman Ben Bernanke into their camp? I would guess that the data would pull him away from additional asset purchases as the threat of imminent recession has dramatically faded into the background. We will get a chance to hear his thoughts on recent data at Jackson Hole next week. I don’t think he will give an obvious clue; as a general rule, that isn’t his style. He will give us the data as he sees it and we will need to figure out what that means for policy.

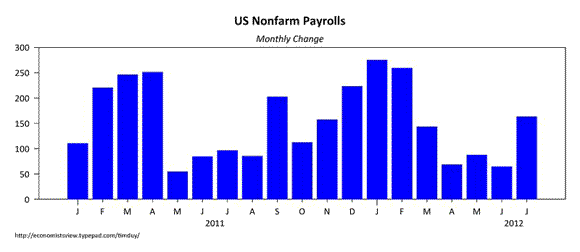

I would also note that we have plenty of data to chew on between now and September 15th. Notably, we will get another look at the employment situation. Note the pattern of the last two years:

Start stop, start stop, but on average, not inconsistent with the Fed’s forecast as interpreted by David Altig (my response to Altig here). The April-June slowdown in job creation certainly gave the doves the upper-hand, pushing us closer to QE3. A solid August number would give the hawks the upper-hand once again.

There was much discussion about possible additional tools. Communications could change:

One of the policy options discussed was an extension of the period over which the Committee expected to maintain its target range for the federal funds rate at 0 to 1/4 percent. It was noted that such an extension might be particularly effective if done in conjunction with a statement indicating that a highly accommodative stance of monetary policy was likely to be maintained even as the recovery progressed. Given the uncertainty attending the economic outlook, a few participants questioned whether the conditionality of the forward guidance was sufficiently clear, and they suggested that the Committee should consider replacing the calendar date with guidance that was linked more directly to the economic factors that the Committee would consider in deciding to raise its target for the federal funds rate, or omit the forward guidance language entirely.

I like the idea of tying policy to macroeconomic outcomes rather than dates. I think it would remove one source of uncertainty about policy. There was generally support for additional asset purchases, including this:

Many participants indicated that any new purchase program should be sufficiently flexible to allow adjustments, as needed, in response to economic developments or to changes in the Committee’s assessment of the efficacy and costs of the program.

I take this to mean that a new program would not be tied down by a specific date or amount, another policy shift I would like to see. Other options were received less enthusiastically:

Some participants commented on other possible tools for adding policy accommodation, including a reduction in the interest rate paid on required and excess reserve balances. While a couple of participants favored such a reduction, several others raised concerns about possible adverse effects on money markets. It was noted that the ECB’s recent cut in its deposit rate to zero provided an opportunity to learn more about the possible consequences for market functioning of such a move. In light of the Bank of England’s Funding for Lending Scheme, a couple of participants expressed interest in exploring possible programs aimed at encouraging bank lending to households and firms, although the importance of institutional differences between the two countries was noted.

Bottom Line: Lots of possibilities at this point. If you were looking for additional asset purchases at the last FOMC meeting, you were not crazy. There was obviously widespread concern about the mid-year slowdown and its implications for the stability of the Fed’s forecasts. Moreover, policymakers appear to have concluded that additional asset purchases could be effective. If the data had continued to progress as it had since the July/August meeting, I would say that another round of QE was a slam-dunk. But the data has not progressed in the same direction; rather than falling short of expectations, it has tended toward upside surprises. That of course could change over the next few weeks. In short, we need to ask ourselves what will constitute a “substantial and sustainable strengthening.” If Lockhart is a guide, I am thinking we have seen such a shift already. If so, I would expect that on the basis of current data the Fed would delay action until closer to the end of Operation Twist II and to see if Congress has come to any agreement on the fiscal situation in 2013. If the change in the data has not reached the threshold of “substantial and sustainable strengthening” then we would expect action. It will be interesting to see if any of the doves back off on their dreary forecasts in the coming days; such shifts in tone would be telling. Also note that there is a middle ground in the possibility of further changes to the communication strategy; something that could placate both the doves and the hawks until a clearer image of the path of the US economy emerges.

Leave a Reply