West Texas Intermediate crude oil, which had been selling for $105 a barrel at the end of March, fell to $80 a barrel last week, while Brent has come from $125 down to near $90. These price declines will translate into substantial savings for U.S. consumers in the weeks ahead.

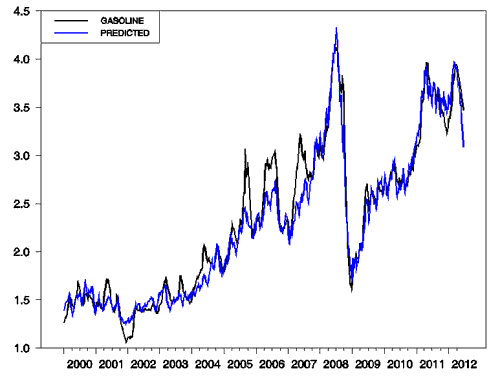

Since Brent and WTI diverged, it has been Brent that matters for U.S. retail gasoline prices; this fact and the reasons for it were discussed here. A regression of the average U.S. retail gasoline price on the price of Brent over 2000-2012 captures the close relation (OLS standard errors in parentheses):

The price of gasoline and price of Brent turn out to be cointegrated, meaning that any permanent change in the price of Brent eventually shows up as a permanent change in the price of gasoline. The coefficients of the above relation are very much what you’d expect. A barrel holds 42 gallons, and the estimated coefficient (0.025) is 1/40. The intercept (0.84) captures an average state and federal tax of 50 cents per gallon plus a bit over 30 cents in markups and other costs.

Black: average U.S. price of regular gasoline, all formulations, in dollars per gallon, weekly Jan 10, 2000 to Jun 18, 2012 (data source: EIA) with Jun 22 value estimated from NewJerseyGasPrices.com. Blue: 0.8 plus 0.025 times price of Brent, in dollars per barrel, weekly Jan 7, 2000 to Jun 15, 2012 (data source: EIA) with Jun 22 value estimated from Oil-Price.net.

With Brent on Friday at $91.50 and an average retail gasoline price about $3.47, we’d thus expect gasoline prices to come down another 35 cents a gallon or so from where they were on Friday. Historically those adjustments usually come pretty quickly. For example, last December U.S. gasoline prices temporarily fell about 25 cents/gallon below the long-run relation, but by March they were right back on track.

If gasoline prices do fall from their value in April near $3.92 to $3.12, that would be an 80 cents/gallon swing. With Americans buying about 140 billion gallons of gasoline each year, that translates into an extra $112 billion over the course of a year that consumers would have available to spend on other things besides gasoline.

So should we be celebrating? I’m afraid not. The primary reason that oil prices have come down is because of growing signs of weakness in the world economy. I am very concerned about where events in Europe are going to lead, and recent U.S. data indicate some weakening. Cheap gas helps, but not so much if you don’t have a job.

But I will offer this advice: wait another week or two if you can before filling up the tank.

Leave a Reply