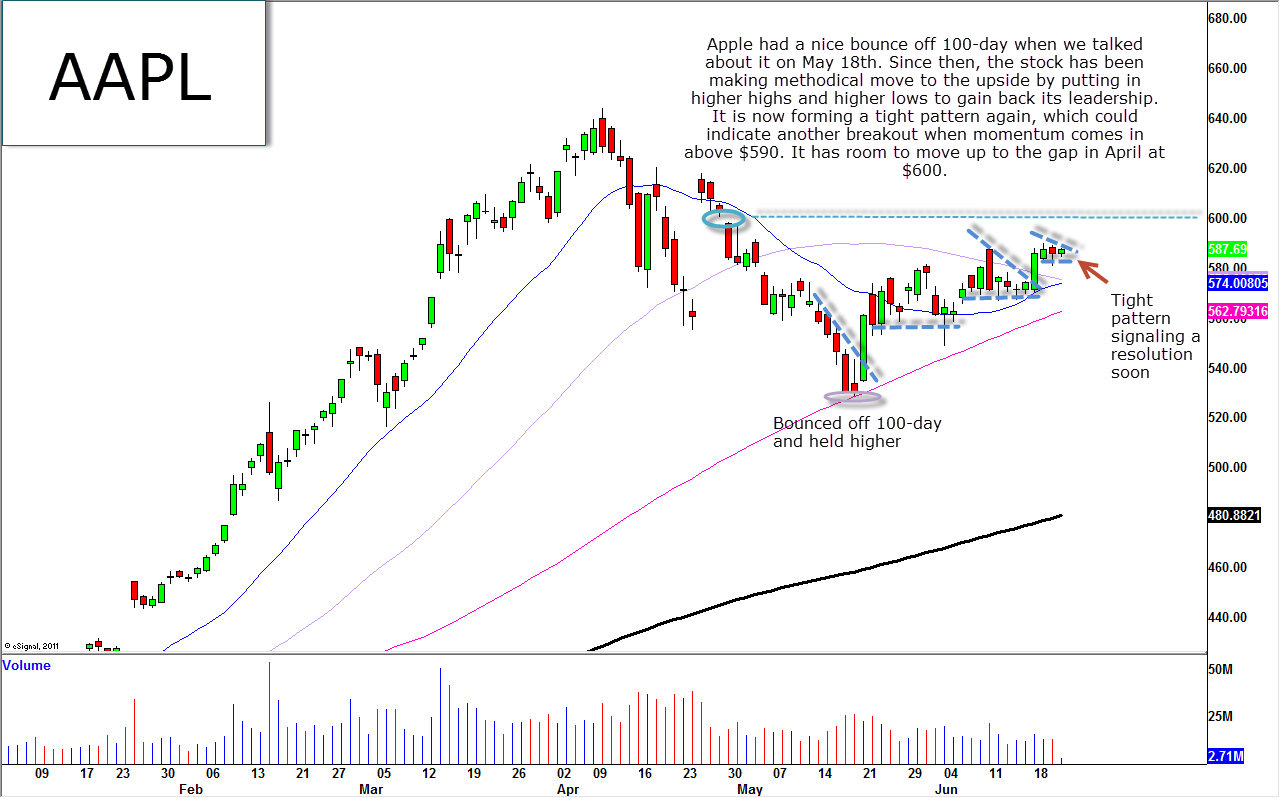

Apple (AAPL) has been trading in a tight range recently, but looks poised for another major break to the upside. Apple has been forming a series of higher highs and higher lows and holding higher on the charts. After finding strong support at 100-day moving average of $528.48 in May, Apple has been holding higher levels, and every time it has formed a tight pattern on the chart, the stock has resolved to the upside with strong volume.

(click to enlarge)

On Monday, AAPL showed its true colors by quickly trading from negative to positive during the first hours and reclaiming its 50-day moving average by end of the day. Since then, we have been seeing a constructive consolidation before another breakout. For micro level investors, look for continuation to the upside for a quick cash flow trade. As long as it holds $578.50, this stock has room to grow all the way to $600 – the bottom of the April’s gap. For macro level investors, if AAPL’s uptrend stays intact we should see this big name putting in a new high for this year moving forward.

Apple’s stock hit a high of $636 in early April, but soon fell off quite sharply. The stock is down 8% since then, compared to only 2% for the S&P. Now however, many investors feel Apple’s stock is actually somewhat undervalued. Apple currently trades at a trailing P/E of 14.2 and a forward P/E (based on analyst estimates) of 10.8. Both are significantly lower than the S&P averages of 15.2 and 12.8 respectively. That means Apple is cheaper than the broader market despite having stronger growth prospects than most other S&P companies. Even more surprising, Apple’s PEG is currently 0.6, where 1 is considered a fair valuation.

Apple has transformed itself into one of the most profitable companies in the world since the release of the iPhone five years ago. The iPhone quickly became the most popular smart-phone on the market, and Apple built on that success by completely rebooting its line of MacBook laptop computers and releasing the iPad tablet. With the iPhone 5 set to debut later this month, and chatter of Apple TV only somewhat diminished after not being mentioned at the WWDC, continued growth still seems a definite possibility for Apple.

Disclosure: Scott Redler is long QQQ.

Interesting analysis. The slump in price recently can probably best be attributed to the belief that the current quarterly sales in the U.S. will experience the typical flattening prior to the launch of an odd-numbered iPhone-generation launch.

The huge unknown is China sales during the quarter. While dozens of pundits try their best to get leads on the technical specs of forthcoming phones, tablets and even TV, there’s no equivalent mining of Chinese and other international sources on ex-U.S. sales. I saw the lines of customers waiting for 4s phones and doubled my AAPL investment, even as the “experts” were panning the product – and sensed similar opportunity when I figured out that Apple stores were sending early iPad “3” customers (even business customers like me) to the Apple online store.

Pundits noted no lines for the “new iPad” and forecast a bust…only to have Apple announce that their online-store sales strategy racked up 3 million unit sales within the first 5 post-launch days.

Bottom line: no one outside a few top execs knows what’s really going on in the markets driving AAPL now. All we can do is wait and be prepared to be amazed.

Are you kidding? What volume? This week saw increasing on LIGHTER volume and that means no conviction. Now, it’s sliding. Also, the high was actually $644. I am bullish longterm, but we’re seeing a possible dip coming and then it may be time to buy long. Waiting to go long some more.