Peter Capelli has looked at the skills gap explanation for labor market weakness and sees more myth than fact:

“Indeed, some of the most puzzling stories to come out of the Great Recession are the many claims by employers that they cannot find qualified applicants to fill their jobs, despite the millions of unemployed who are seeking work. Beyond the anecdotes themselves is survey evidence, most recently from Manpower, which finds roughly half of employers reporting trouble filling their vacancies.

“The first thing that makes me wonder about the supposed ‘skill gap’ is that, when pressed for more evidence, roughly 10% of employers admit that the problem is really that the candidates they want won’t accept the positions at the wage level being offered. That’s not a skill shortage, it’s simply being unwilling to pay the going price.”

To some extent, the issue is semantic:

“But the heart of the real story about employer difficulties in hiring can be seen in the Manpower data showing that only 15% of employers who say they see a skill shortage say that the issue is a lack of candidate knowledge, which is what we’d normally think of as skill. Instead, by far the most important shortfall they see in candidates is a lack of experience doing similar jobs. Employers are not looking to hire entry-level applicants right out of school. They want experienced candidates who can contribute immediately with no training or start-up time…”

In the language of economists, Capelli is defining skill as the possession of generalized human capital, while businesses are defining skill as the possession of firm- or job-specific human capital. In more familiar language, Capelli appears to be focused on innate skill levels and education, while businesses are looking for the types of skills that would be attained through past on-the-job training. In even more colloquial language, Capelli wants businesses to appreciate book-learning, and businesses prefer those who have already survived the school of hard knocks.

We have recently completed our own version of the Manpower survey Capelli references. Our results are based on the responses of about 100 businesses in the Sixth Federal Reserve District represented by the Atlanta Fed, and we do not claim that they are conclusive. But we do think they are instructive.

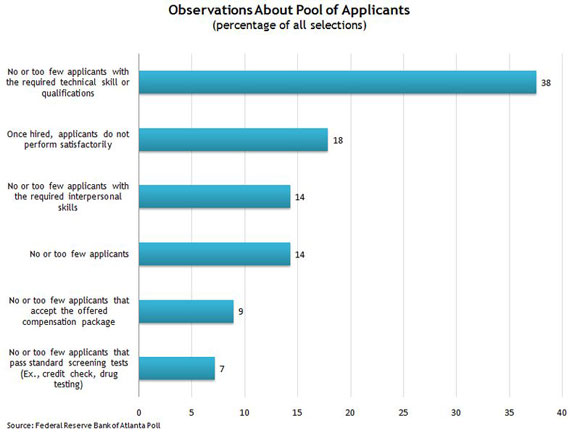

Of those firms that said they experienced an increase in hiring difficulty over the last year, our poll respondents confirm the notion that businesses are looking for candidates with specific skills:

The lack of technical skills is the only factor that really jumps out as an issue that businesses have with the pool of job applicants. We often hear anecdotal complaints about job seekers’ lack of “soft skills,” or the difficulty in finding applicants who can pass required background checks. But only 14 percent of all selections indicated too few applicants with required interpersonal skills, and only 7 percent indicated a problem with applicants passing screening requirements like drug-use or credit checks.

On the other hand, our poll found scant support for Capelli’s claim that businesses are “unwilling to pay the going price.” Only 9 percent of respondents reported that too few applicants would accept the offered compensation package.

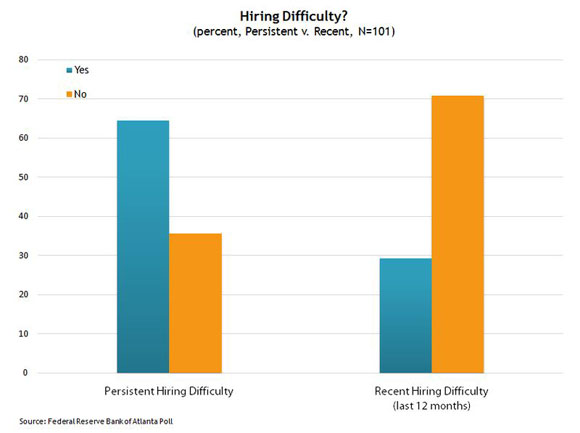

Despite the fact that we see some evidence consistent with skill mismatch, it is far from clear that this issue is the smoking gun that explains the current anemic state of job growth. When asked if a dearth of skilled applicants is a persistent problem, our survey respondents overwhelmingly answer “yes.” But when asked if they have had more difficulty hiring over the past 12 months, the overwhelming majority answered “no”:

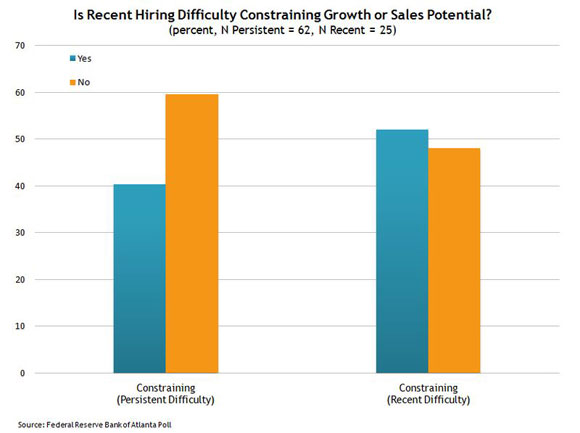

Even among the minority of businesses that report recent hiring difficulties, only half indicate that this difficulty is restraining growth:

We infer a couple of lessons from all of this information. First, it does appear that there is a long-term skill level problem in the U.S. economy. Adopting Capelli’s definition of skill does not mean the existence of skill mismatch is a myth.

But turning to the short run, we’ve been pretty sympathetic to structural explanations for the slow pace of the recovery. Nonetheless, we have yet to find much evidence that problems with skill-mismatch are more important postrecession than they were prerecession. We’ll keep looking, but—as our colleagues at the Chicago Fed conclude in their most recent Chicago Fed Letter—so far the facts just don’t support skill gaps as the major source of our current labor market woes.

Leave a Reply