For some time, financial observers have been discussing the large positions in bond-index derivatives amassed by a trader known as the London Whale, now revealed to be Bruno Iksil working for JP Morgan Chase (JPM). On Thursday we learned that JP Morgan has lost over $2 billion in the space of two weeks as a result of the trades. On Friday the stock price fell by 9.3%, wiping out $14.4 billion of the company’s value.

How do you lose so much money so quickly? The short answer is, leverage. Although details are not known, one likely scenario ([1], [2]) involves derivatives constructed from the riskier components of some European corporate bonds. Using derivatives, you can buy or sell securities or pieces of securities that you do not yourself own, involving a potential promise to deliver more money than you even have. If the market moves against you, you’ll have to deliver substantial real cash to unload your commitment, and this process appears to be what produced the sudden losses. The Whale’s notional exposure in one index was speculated to have been $100 billion in April.

The total notional exposure of all of JP Morgan’s trades has been estimated to be $79 trillion. That’s “trillion”, with a “T”, from a company with an equity value of $140 billion, and falling quickly.

Paul Krugman suggests that in the case of the trades by the London Whale, JP Morgan “was just engaging in financial tricks of little or no social value”. One could argue that the role of leveraged bets through derivatives is to allow those who really know what the value of the underlying security should be to help guide the market to that correct valuation. But if you’re making your bet with somebody else’s money, where the deal is you get the upside and somebody else gets the downside, those leveraged bets aren’t so likely to be in the public’s interest.

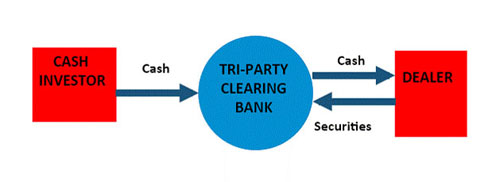

In any case, we would want to weigh any potential social benefits of such trades against their possible social costs. Is JP Morgan “too big to fail”? I think so. A recent paper by Stanford Professor Darrell Duffie highlights an unresolved weakness in the U.S. financial system centered on the tri-party repo market. This is a key mechanism whereby institutions with funds to lend overnight, such as money market funds, provide funds to those with short-term borrowing needs, namely dealer banks who are prepared to pledge securities as collateral for a one-day loan. Each day something like $100 billion in such short-term lending is intermediated by two clearing banks (JP Morgan Chase and Bank of New York Mellon). Dealer banks deposit securities as collateral with the clearing bank in exchange for a one-day loan, which funds the clearing bank in turn receives later that day from the ultimate lender.

Source: Duffie (2012).

Duffie believes the system is inherently unstable, as dealer banks depend crucially on the ability and willingness of the clearing banks to provide short-term financing each new day:

A dealer whose solvency or liquidity come into question may be unable to find cash lenders that are willing to roll over a sufficient quantity of its repos. In that case, concerns over a dealer’s liquidity might be self-fulfilling. The dealer could fail, or its securities might need to be liquidated in a fire sale, or both….

A fire sale of a dealer’s securities caused by the dealer’s inability to roll over its repo financing on a given day could temporarily depress the prices of some of the affected classes of securities, particularly those securities that lack transparency or whose credit- worthiness depends on the stability of the financial sector. This could have spillover effects to other dealers and more broadly.

Between the unwinding of the previous day’s repos and the roll into the next day’s repos, money market funds and other cash investors claims are in the form of demand deposits at the clearing bank. In extreme scenarios and in the absence of sufficient transparency, cash investors could become concerned that a clearing bank could be destabilized by its intra-day secured-lending exposure to a dealer. A run of these intra-day demand deposits could indeed destabilize the balance sheet of a clearing bank in the worst case.

Here is Duffie’s recommendation for how to make the tri-party clearing system more stable:

Given the systemic importance of tri-party clearing agents, and given their high fixed costs and additional economies of scale, tri-party repo clearing services for U.S. dealers and cash investors should probably operate through a dedicated regulated utility. Although this would likely increase operating costs for market participants, it would enable investment in more advanced clearing technology and financial expertise, allowing greater resilience of the tri-party repo market in the face of financial shocks such as the default of a major dealer. The moral hazard associated with lending of last resort to a dedicated utility is much reduced relative to the case of a financial institution with a wide scope of risk-taking activities.

If nothing else, this week’s news should remind us that more needs to be done to ensure financial stability and that the incentives of private participants align with the public’s best interests.

Leave a Reply