Friday’s jobs report was unquestionably a disappointment. But other recent U.S. economic indicators are more encouraging.

One of the big concerns of many analysts was that rising oil prices of the last 5 months might significantly slow down economic growth. My view is that the main mechanism by which oil prices can sometimes have a disproportionately disruptive effect on the economy is if they result in sudden shifts in the patterns of spending. One typical channel is a plunge in sales of the larger vehicles manufactured in the U.S., which then leads to further losses of income and jobs in the auto sector. But the evidence suggests that an oil price increase that just reverses a previous oil price decrease– and that is basically what we’ve experienced so far in 2012– is not nearly as disruptive as if the price were rocketing into uncharted territory. One reason for this is that recent consumers’ vehicle purchase plans were already taking into account the possibility that $4 gas could soon return.

The latest data confirm that sales of domestically manufactured light trucks (a category that includes SUVs) in March were still lower than they were in 2008, the first time we saw gasoline prices moving up to the values that now seem pretty normal. In 2008, sales at those levels came as a shock to Detroit. Today, they’re about the best anybody was expecting.

Data source: Webstract

On the other hand, sales of the lighter cars manufactured in North America were at the highest level of any March over the last decade. The Wall Street Journal reported on Wednesday:

Last month, consumers’ thirst for small and fuel-efficient cars was a prime factor in driving light car and truck sales nearly 13% higher than a year ago. General Motors Co. GM said it sold more than 100,000 cars that get 30 or more miles on a gallon, its highest ever and nearly half of the 231,052 vehicles it sold.

Data source: Webstract

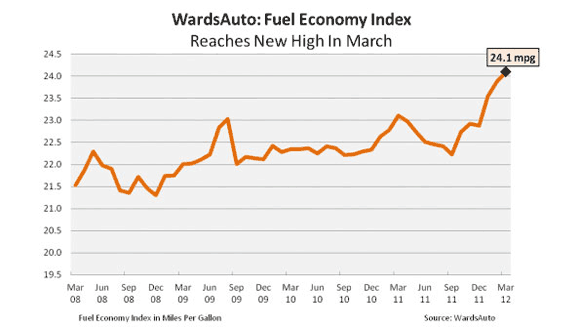

Thus despite rising gasoline prices, the auto sector should make a nice contribution to 2012:Q1 GDP growth, mainly because what’s happening now did not catch U.S. automakers or consumers by surprise. Mark Perry calls attention to this interesting graphic from Wards Auto showing that U.S. new light vehicles achieved record fuel-efficiency for the third month in a row in March.

Source: Wards Auto

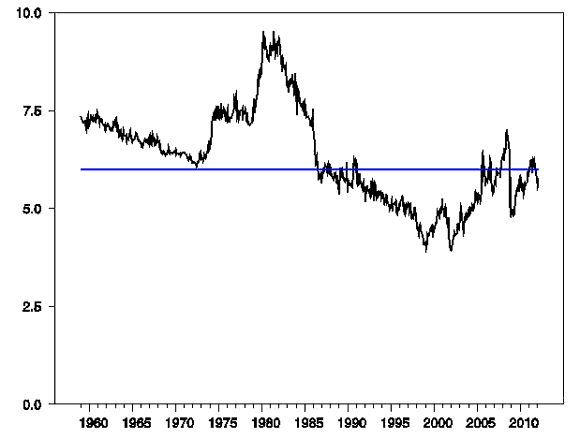

Even if this spring’s high gasoline prices aren’t preventing Detroit from selling cars, they are still an undeniable drag on household budgets. However, improved fuel economy, low natural gas prices, and a mild U.S. winter have all helped cushion the effects of that, with spending on energy goods and services still only 5.8% of total consumer spending for February, lower than the values we saw this time last year.

Energy expenditures as a percentage of consumer spending, 1959:M1 to 2012:M2. Calculated as 100 times nominal monthly consumption expenditures on energy goods and services divided by total personal consumption expenditures. Data source: BEA Table 2.4.5U. Blue line is drawn at 6.0%.

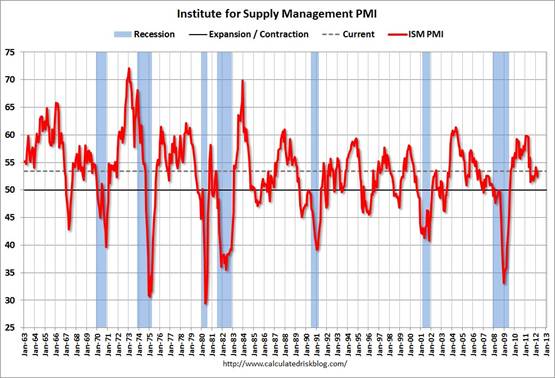

Some other recent U.S. economic data are also mildly encouraging. The latest national income accounts allow us to calculate a separate measure of real GDP growth based primarily on income data rather than purchases. The income-based measure suggests that U.S. real GDP grew at a 4.4% annual rate in 20011:Q4, compared with the 3.0% growth implied by the traditional GDP calculation. That discrepancy raises the possibility that when the 2011:Q4 GDP numbers are subsequently revised, they could well be revised upward from the current 3.0% estimate. Another favorable indicator was a modest improvement in the manufacturing PMI for March, consistent with a view that growth is accelerating.

Source: Calculated Risk

The big disappointment (and unfortunately the single most important number) was Friday’s report from the BLS that the number of Americans on nonfarm payrolls only increased by a seasonally adjusted estimate of 120,000 workers in March, well below the 246,000 average gains over the preceding 3 months. The separate BLS survey of households actually recorded a seasonally adjusted drop in employment of 31,000 workers. There was an even greater drop in the number of working-age Americans looking for jobs, which produced the somewhat misleading impression of an improvement in the labor market in the form of a drop in the reported unemployment rate from 8.3% in February to 8.2% in March.

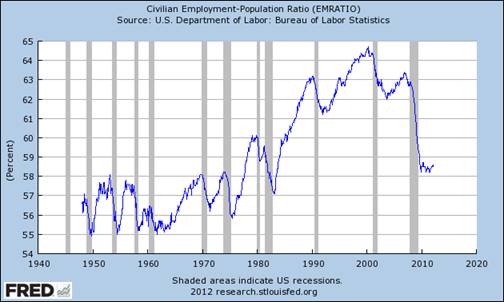

Source: FRED

A steep decline in the employment-population ratio is very often seen during a recession, and usually it picks back up when the economy starts to grow again. This time it has not. As John Mauldin notes, partly this is due to long run trends of a falling labor participation rate for men and reversal of a previous trend of rising labor force participation by women. Notwithstanding, with a healthier economy, we expect to see at least some resurgence of this indicator. The fact that no such rebound is yet in sight confirms that while the economy undeniably continues to grow, the rate of that growth continues to disappoint.

Leave a Reply