Morgan Stanley, the uber bull of Amazon.com (NASDAQ:AMZN) is cutting their rating to Equal-Weight from Overweight with a $190 PT (down $30).

– Firm says they would be buyers of the stock at levels closer to $150 (~1x 2012E Net Sales) or toward the end of the more challenging year ahead.

Effect:

Amazon.com will most likely experience decelerating sales (and unit volume) growth rates throughout 2012, which may become clearer to investors with the CQ2:12 sales guidance to come on its CQ1 conference call. Interestingly, Amazon.com has an easy comp in CQ1 due to a 500 bps international sales impact from the earthquake / tsunami in Japan last year. However, when Amazon.com guides to CQ2 it will be doing so against a strong CQ2:10 comp of +44% y/y sales growth, and the firm expects investors may be surprised at the organic deceleration occurring in the business that may manifest itself within the CQ2 guide.

Cause:

The drivers of Amazon.com’s deceleration are numerous, some real and some optical, but all significant to the sales / unit growth story.

1. Apple (AAPL, $498, rated OW by Katy Huberty) may be having a significant and direct impact on Amazon.com’s EGM segment.

2. Apple and others are driving an accelerating digital shift in the Media category, and an increasing pace of change puts Amazon.com’s non-book Media business at risk (Music, Video and Video Games).

3. The console-based video game business is in a cyclically weak (possibly secularly weak) period.

4. The transition to 3P / FBA is being driven partially by the transition of eBooks to net sales accounting and while positive long-term, we do not think physical goods 3P is growing as fast as some investors believe.

5. Slowing sales growth and an overall shift to more 3P and digital goods may change the dynamics of working capital, a significant component of consolidated FCF that most investors currently capitalize at the same multiple as Amazon.com’s operating FCF

Details:

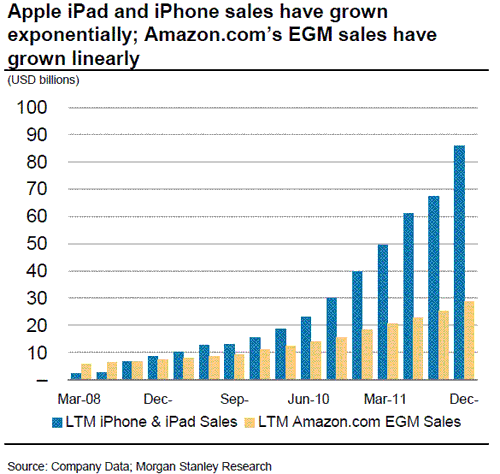

The Apple Impact:

In CQ4:11, Apple reported $33.6B of sales from two products – iPhone and iPad, which was more than 3x the size of Amazon.com’s entire EGM category. Importantly, Amazon.com is not a licensed retailer of iPhone and iPad, which has left a noticeable gap in Amazon.com’s consumer electronics portfolio. The true impact manifests itself in the sales growth deceleration of Amazon.com’s North America (“NA”) EGM sales line, which decelerated in CQ4:11 to +27% y/y growth (excluding Kindle Fire) from +44% y/y in CQ3:11. While most investors focused on Amazon.com’s Media sales deceleration, the EGM deceleration is more significant since it is the segment that investors expect the most share gains from over time.

The Digital Impact:

The second derivative impact of Amazon.com’s Apple issue is that mobile device proliferation is accelerating the shift of books, music, video and video games to digital distribution. Amazon.com is currently the market share leader in books but otherwise faces an uphill battle. We estimate that ~40% of Amazon’s media sales or ~16% of total sales comes from non-book media sales, and we believe this revenue stream is increasingly at risk to companies such as Apple, Netflix, Pandora, Spotify, etc. We believe Amazon.com is particularly focused on two of the four media categories – books and video. The books category has already been a huge success and given the media war that Amazon.com is now fighting to sustain its media business through the digital transition, we think Amazon.com will spend as much as it needs to in video to win top-spot within the second media category. With that said, we are incrementally negative on Netflix as we believe Amazon.com has competitive strengths that could aid in its war for video market share, namely its video streaming delivery infrastructure and its large, engaged customer base. Furthermore, Amazon.com has the necessary capital to ‘pay to play’ in this area (Netflix spends $1.5B-$2B per year on content). As it relates to music and video games, we believe Amazon.com is currently in a more difficult position and may choose to buy vs. build in these areas over time. Net / net, Apple is a problem for Amazon.com and the first / second derivative impacts will drive Amazon.com to continue spending aggressively for an extended period in the areas of discounted hardware devices, acquiring content, etc to sustain its competitive position within the media category.

Our views -> Numbers -> Value:

Our highest conviction views are around slowing unit volume growth, lower gross profit per unit and lower unit sell-through in the Media category. Those factors lead us to lower our 5-yr sales CAGR from 25% to 23% and our 10-yr CAGR from 18% to 16%. After factoring in slightly better gross margins due to 3P mix shift, our fair value estimate decreases by $42. Lower net Opex and Capex spend make-up ~$12 of positive value per share. Net, our fair value estimate declines by $30 and we shift to Equal-weight.

Notablecalls: Morgan Stanley has been a long-term supporter of AMZN & this cut will leave a dent:

– Note MSCO is also making a s-t call on the qtr saying investors will be ‘surprised at the organic

deceleration’ in CQ2 guide.

– I’m thinking we will see a 4-5% drop in the stock towards $177-$175 range.

PS: Look at what they did to AAPL yesterday.

Leave a Reply