I’ve been doing some work on gaining a better understanding of the root causes of eurozone (EZ) debt crisis. As a point of departure, let’s take a couple of dueling quotes. First, Wolfgang Schäuble, Germany’s finance minister, from his recent piece in the Financial Times:

Whatever role the markets have played in catalysing the sovereign debt crisis, it is an undisputable fact that excessive state spending has led to unsustainable levels of debt and deficits that now threaten our economic welfare.

Next, here’s an excerpt from a statement recently made by Greece’s Deputy Prime Minister and Minister of Finance, Evangelos Venizelos:

We should not be the scapegoat or the easy excuse that will be used by European and international institutions in order to hide their own lack of competence to manage the crisis and give a definitive and complete answer to the attacks against euro, the world’s strongest currency.

These two statements capture the essence of two radically different views about the origins of the EZ debt crisis. Which one is right?

Local Causes or Systemic Causes?

Some believe that the crisis was fundamentally caused by profligate, irresponsible behavior by governments and individuals in the EZ periphery. (Note: by the “EZ periphery” I mean Greece, Portugal, Ireland, and maybe Spain. Italy has not really been accused of such behavior, to my knowledge, and it seems generally accepted that it is much more the victim of contagion rather than the cause of the crisis.) Let’s call this the local causes point of view: government deficits and debt in the periphery were so large that once the Great Recession of 2008-09 hit, investors lost confidence in the ability of those countries to remain solvent. So they tried to dump the bonds from those countries, triggering the crisis.

An alternative point of view is that, while the crisis may have had some peculiarly local triggers (the Greek government’s admission that it fudged some official statistics certainly didn’t help), much of the current mess is the result of forces and decisions outside the control of peripheral Europe’s governments. In other words, the crisis could have non-local, systemic causes.

For example, suppose that the adoption of the euro suddenly made it more attractive for investors in the rest of Europe to buy assets in the periphery. This could have caused a large, exuberant capital flow from Europe’s core to periphery, much like NAFTA helped to spark a surge in capital flows from the US to Mexico in the early 1990s. But we know that such “capital flow bonanzas” (so named by Reinhart and Reinhart) are notoriously susceptible to changes in investor attitudes, and can come to an abrupt halt. These sudden stops in capital flows, as they are referred to in the literature, typically trigger a financial crisis. (See this paper by Calvo, Izquierdo, and Mejia for much more about sudden stops.) As noted by Rudi Dornbusch in the context of the Mexico crisis of 1994, it’s not speed that kills; it’s the sudden stop.

Crucially, sudden stops may happen even when a country is following all the right macroeconomic policies. As a result, financial crisis may be largely outside the control of a country that’s on the receiving end of a capital flow bonanza. Mexico in 1994 is a good example of that, I think. And it could be that some of the peripheral EZ countries also fit this characterization. If so, then it’s not appropriate to lay the blame for the crisis entirely at the doorstep of the peripheral EZ’s governments; while they may have done some things that contributed to the crisis, the odds were significantly stacked against them to begin with.

Evidence

Which view of the EZ crisis – the local causes view or the systemic causes view – better matches the evidence? There are a few different types of clues we can look for.

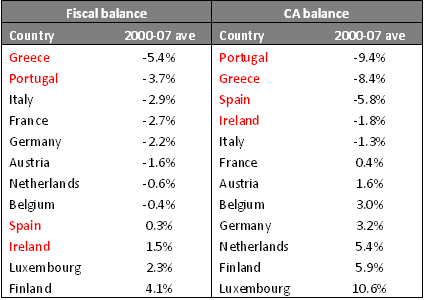

1. Which deficit predicted the crisis?

If the crisis is due primarily to local causes, then we would expect the best predictor of crisis to be government deficits and debt. On the other hand, if the systemic causes view is correct, then a better predictor of the crisis would be large current account deficits, which necessarily happen when there’s a capital flow bonanza.

The following table shows both fiscal (i.e. national government) budget balances and current account balances during the period after the adoption of the euro and before the worldwide financial crisis and recession struck in 2008. All figures are from the OECD and expressed as a % of GDP.

The factor that crisis countries have in common is that, without exception, they ran the largest current account deficits in the EZ during the period 2000-2007. The relationship between budget deficits and crisis is much weaker; some of the crisis countries had significant average surpluses during the years leading up to the crisis, while some of the EZ countries with large fiscal deficits did not experience crisis. This is one piece of evidence that a surge in capital flows, not budget deficits, may have been what laid the groundwork for the crisis.

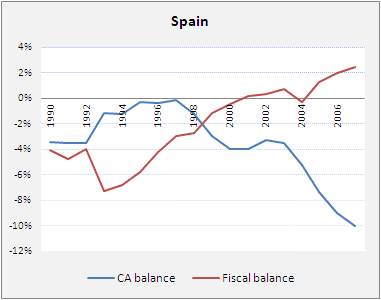

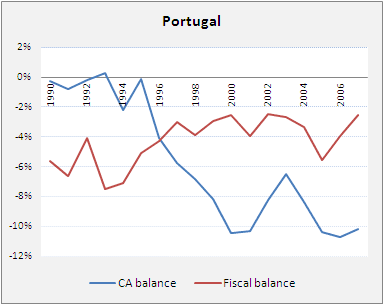

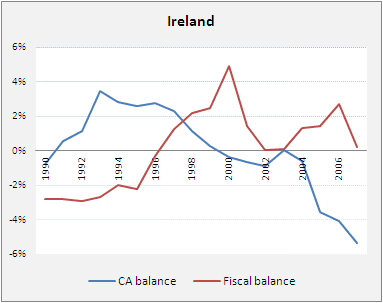

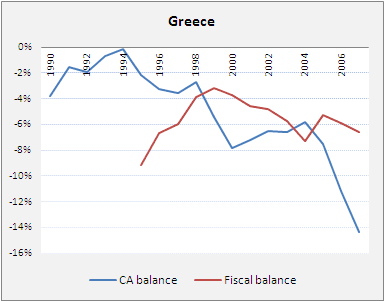

2. Which deficit grew after euro adoption?

If the crisis is due to the profligacy of governments in the peripheral EZ that took advantage of EZ membership to increase spending, we would expect to see budget deficits grow in the periphery after the common currency was introduced in 1999. But if the crisis was really the result of a post-euro adoption surge in capital flows from the EZ core that then came to a sudden stop, we would expect current account deficits (i.e. capital flows) to have grown more after adoption of the euro.

The following charts show the path of both types of deficits during the years before and after adoption of the euro. (Data from the OECD, expressed as % of GDP.)

Capital flows (i.e. current account deficits) increased substantially in all the EZ periphery countries in the period after adoption of the euro. Meanwhile, the peripheral countries generally tended to have tighter fiscal policies after adopting the euro than before euro adoption.

Note that the capital flow bonanzas in evidence in these charts were directly the result of the adoption of the euro by the peripheral EZ countries, which made it easier for capital in the core EZ countries to find investment opportunities in the periphery. In fact, this was exactly what the advocates of the common currency intended and expected, and has always been touted as a selling point for the euro project – it’s called “financial integration”. The problem is the sudden stop that frequently follows such a capital flow bonanza.

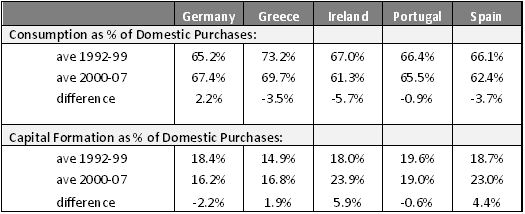

3. What did the periphery countries spend their money on?

If the crisis is due to irresponsible behavior by governments and individuals in the EZ periphery, then one indicator of that would be a rise in government spending and/or personal consumption after euro adoption. On the other hand, the systemic causes view would suggest that crisis could strike even if a country is behaving ‘responsibly’ (in a macroeconomic sense) by spending more on investment goods (i.e. capital formation) and less on personal consumption.

The next table shows the fraction of domestic purchases spent on consumption and investment goods in each of the EZ periphery countries. Germany is included in the table for comparison.

There is a clear tendency for investment spending to rise in the periphery countries (with the exception of Portugal), and for consumption to fall. Meanwhile, investment spending fell and consumption rose as a proportion of total spending post-1999. This is all consistent with the convergence story; capital flowed from the core to the periphery to take advantage of and fund investment opportunities there. Meanwhile, with the periphery countries experiencing fiscal contraction, a smaller share of purchases going to personal consumption, and a higher share of purchases going to investment goods, it is hard to see evidence for the story that the capital inflows were simply frittered away on a spending binge either by individuals or governments.

So… What Really Caused the Crisis?

Putting it all together, it seems that the EZ crisis is more consistent with the systemic causes view than the local causes view. In other words, while they didn’t necessarily make the right decision every time, the peripheral EZ countries were up against powerful exogenous forces – capital flow bonanzas and sudden stops – that tended to push them toward financial crisis. They were playing against a stacked deck.

It’s useful to reevaluate the macroeconomic history of peripheral Europe in light of this interpretation. Rather than large current account deficits being the result of fiscal mismanagement or excessive consumption, the current account deficits were the necessary and unavoidable counterpart to the surge in capital flows from the EZ core. Rather than above-average inflation rates and deteriorating competitiveness being signs of labor market inefficiencies or lax fiscal policies in the peripheral countries, appreciating real exchange rates were inevitable as the mechanism by which those current account deficits were effected.

The eurozone debt crisis is big enough that there’s plenty of blame to go around, and some of it certainly should go to the crisis countries themselves. But it must also be recognized that as soon as those countries adopted the euro, powerful forces were set in motion that made a financial crisis likely, and very possibly unavoidable, no matter what the governments of the peripheral euro countries did. Irresponsible behavior by the periphery countries did not set the stage for the eurozone crisis; the common currency itself did.

Coming soon: Part 2 of this series, in which I examine some policy implications of this analysis.

Interesting insight. I am not sure I am convinvced that you can let local governments and consumers off the hook, but the capital bonanza followed by the capital cut-off is part of the puzzle.

It might be interesting to look at opening positions as well. Greece did fudge their numbers to achieve the Maastricht conditions. They started with a per capita debt burden that was larger than the other eurozone members. As such they should have been more diligent than Germany for example in eliminating deficits.

And it’s not like waves of capital come flooding in and can’t be controlled. Governments and individuals still have responsibility for responsibly financing consumption with debt, even though these costs might be lower than they weer accustomed to. Peripherals solicited funding to meet consumption. Current accounts were not in deficit because cash washed up on shore, and they were then forced to go and spend it. They spent first, knowing that they could find a market for the debt to finance it.

Finally a thoughtful and, especially, documented article on this crisis. If the author found a way to communicate this insight to some popular – but hideously misinformed and prejudiced – sites, such as WSJ or CNBC, the level of discourse and understanding would make a quality leap upwards. Maybe even sanity would return.

I mention this, simply because I see this crisis being used as an excuse to bring forward, as “acceptable”, attitudes (witch-hunts and racial bigotry) and methods (e.g wholesale looting of countries) that we had not seen on planet earth since the late 17th century. We all know that, less than 10 years after the Boer War, Europe pressed the self-destruct button. I know they are not smart/interested to not do the same again, but maybe, an informed public opinion could force them to be logical, instead of following their “Leaders”, with torches and hay-forks.