In proper analogy format, today’s news that the Swiss National Bank (SNB) is going to buy “unlimited quantities” of foreign currency in order to keep the Swiss Franc (CHF) from appreciating beyond 1.20 CHF/euro can be expressed as follows:

China:US :: Switzerland:Eurozone

Just as China has for years steadily purchased US dollars in order to keep its currency from appreciating, Switzerland has now promised to buy euros in order to keep the CHF from appreciating. To help understand what that means, here are some FAQs:

1. Why did the SNB decide to do this?

The SNB had to act because the strong CHF had basically been strangling the Swiss economy by making Switzerland a horrendously expensive place to manufacture or buy things. So it’s not surprising that the SNB decided it was time to take steps to prevent a dangerous deflationary spiral from taking hold.

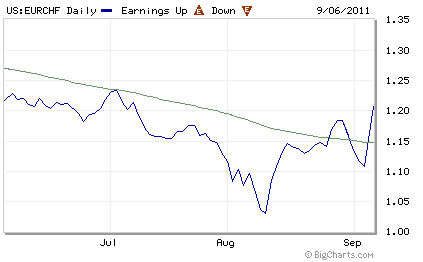

2. Is the SNB’s new exchange rate policy credible?

Yes, it is absolutely credible. There’s no technical or economic limit to the ability of the SNB to sell CHF and buy euro to keep the exchange rate above 1.20, simply because the SNB can create as many CHF as it wants. So the exchange rate will only go below 1.20 if and when the SNB decides to allow that to happen.

3. What will this do to the Swiss money supply?

Chances are high that Switzerland’s money supply will explode. There’s probably no getting around this one; the only way the SNB can keep its exchange rate at the desired level is to offer unlimited CHF at an exchange rate of 1.20 CHF/euro to anyone who wants to use Switzerland as a safe haven for their money. Given that lots of people are seeking safe havens for their money right now, it’s likely that there will be a lot of takers, which means that the SNB will have to create lots and lots of new CHF.

However: please remember that this doesn’t matter. I know, I know, lots of people are going to immediately jump to the possibility that this will cause rampant inflation in Switzerland. But it won’t. Inflation is not determined by the amount of money in the economy — it’s determined by the amount of demand. That’s why gigantic increases in the US money supply in recent years have had no effect on US inflation. The same will be true for Switzerland.

4. But what if (just for the sake of argument) inflation did start to pick up in Switzerland?

In that case — which could happen if demand for Swiss goods and services picks up in a serious way — then investors will begin to realize that all those CHF they accumulated are losing purchasing power, and they will start to sell them. And the process of the SNB creating CHF to buy euros can simply be reversed. Furthermore, in that case the SNB will be perfectly content to let the CHF appreciate again, if there’s still a tendency for it to do so.

5. Will this stem the flow of cash into Switzerland? At the announced exchange rate floor of 1.20, I doubt it. Banks and other financial institutions are still seeking refuge from perceived risks in Europe, and they seem to be moving their money out of other European countries at a rapid clip. Much of that is going to the US, but not all of it, so investors will continue to seek other safe places to park their funds. Switzerland’s attractiveness as a safe haven will not be diminished just because the SNB is enforcing what will effectively be a fixed exchange rate. However, there is one possible additional step that the SNB could take to help stem the tide of cash…

6. Will the announced exchange rate floor of 1.20 CHF/euro be modified?

It’s possible, and in fact, the announcement by the SNB indicated that they would like the CHF to weaken further over time. This is a very sensible strategy by the SNB, and I wouldn’t be surprised if they soon make an explicit promise to gradually ratchet up the exchange rate from 1.20. The reason is because only by promising investors that their CHF portfolio will suffer exchange rate losses over time can the SNB really do something to staunch the flow of funds into Switzerland — a fixed exchange rate of 1.20 won’t do it. The SNB will probably give it a little time to see if the flow of funds into Switzerland slows as a result of today’s action, but if it doesn’t, then look for the SNB to set a gradually rising target exchange rate going forward.

7. How will this affect the eurozone?

That depends in part on what the SNB decides to do with all of those euro it will be accumulating. Some reports suggest that the SNB (typically cautious) had decided to only buy German and French government bonds with those euro, and not bonds from other eurozone countries. That will have the effect of exacerbating the interest rate differentials between the eurozone core and periphery, potentially making things worse. It would be reasonable to interpret this as indicating that the SNB believes that there’s a good chance that eurozone is going to lose the periphery countries.

Alternatively, the SNB could decide to place a bet on the survival of the eurozone, or at least on continued Spanish and Italian inclusion. If so, then it could help to make that positive outcome happen by using some of its growing stash of euros to buy Spanish and Italian government bonds. Not only would this directly help to narrow interest rate spreads between the core and periphery, but it would be interpreted by the markets as a major vote of confidence.

Either way, Switzerland’s fate is now substantially tied to the eurozone. This was always true to some degree, of course, but the linkages will now be even deeper and more explicit, as the SNB begins rapidly accumulating a big pile of eurozone bonds. It’s yet another example of how the eurozone debt crisis has had, and will continue to have, effects far beyond the eurozone itself.

Leave a Reply