A new paper from the San Francisco Fed “The U.S. Content of ‘Made in China‘” has been getting a lot of blog attention, see Matt Yglesias, Doug Henwood and Tim Fernholz (HTs to Steve Bartin and Jonah Goldberg). One of the main points of the article is:

“Whereas goods labeled “Made in China” make up 2.7% of U.S. consumer spending, only 1.2% actually reflects the cost of the imported goods. Thus, on average, of every dollar spent on an item labeled “Made in China,” 55 cents go for services produced in the United States. In other words, the U.S. content of “Made in China” is about 55%.”

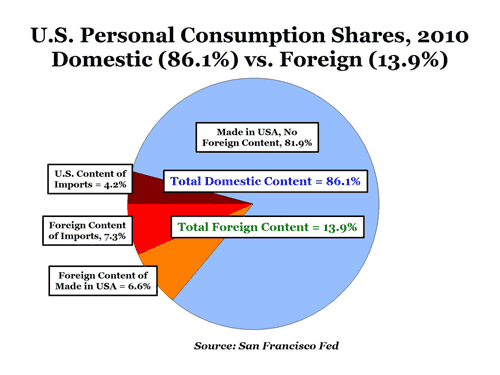

Expressed in dollar amounts, that means that of the $276 billion spent by consumers in 2010 on goods “Made in China” (or 2.7% of total consumer spending of $10,245 billion), only about $123 billion (0r 1.2% of consumer spending) reflects the contribution of Chinese content, and the other $153 billion (or 1.5% of consumer spending) actually goes to American companies and workers for value added in the U.S. from transportation, distribution, marketing, wholesale and retail activities.

For those goods “Made in the USA” with parts imported from China, the contribution of the Chinese content represents only 0.7% of total consumer spending.

Bottom Line:

1. The total share of U.S. consumer spending on: a) “Made in China” imports (1.2%, see chart) plus b) the value of Chinese inputs used to produce goods labelled “Made in the USA” (0.7%, see chart) together represents less than 2% (1.9%) of personal consumption expenditures (or $194.65 billion out of $10,245 billion).

2. The SF Fed concludes that because the “share of consumer spending attributable to imports from China is less than 2%, it is unlikely that recent increases in labor costs and inflation in China will generate broad-based inflationary pressures in the United States.”

3. Doug Henwood adds that “it’s also an antidote to the widespread belief that the U.S. is hollowed out and all the action is in China.”

Leave a Reply