Last week gold hit a new record high, and the business press is now breathlessly reporting that gold futures broke $1,600 per ounce for the first time. Should we care?

There are a couple of reasons why we might care about the price of gold: if it tended to make other things more expensive, as oil does; if it told us something about market psychology, e.g. inflation expectations; if it was a good leading indicator for something. While some or all of these may have been true at times in the past, I don’t think that any of them hold today, so the short answer to my question is no, I don’t see any reason to care about the price of gold.

Wait a minute, you’re thinking: gold is a classic hedge against inflation, and so the price of gold has always been viewed as a good indicator about where market participants think inflation is going. It turns out that the relationship between gold and inflation expectations is rather out-of-date; as shown in the chart below, the price of gold has not shown any correlation with inflation for the past 15 years or so. (Note that the green line shows one explicit measure of inflation expectations, by measuring the interest rate difference between bonds that are indexed against inflation compared to those that aren’t.)

So the dramatic rise in the price of gold over the past couple of years does not seem to tell us anything about average market inflation expectations. Then what has caused that amazing price rise?

In looking at the data I was struck by how small (relatively) the worldwide market for gold really is. That means that relatively small inflows of funds into the market for gold could potentially have very large effects on the price of gold. And that in turn means that the price of gold could be very sensitive to a number of factors that have nothing to do with economic conditions or inflation.

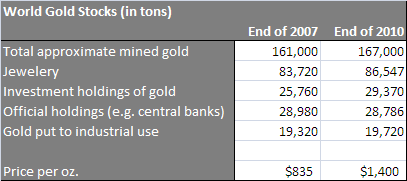

The table below shows how much gold exists in the world, and its distribution. (Data is from the World Gold Council.) Most gold that has been brought above ground on Earth has been turned into jewelery. And even over the past couple of years, roughly 2,000 tons per year of new gold jewelery is produced. (Though keep in mind that a certain amount of gold jewelery is also recycled each year, so the net increase of gold that is in jewelery form is smaller than that.)

Surprisingly, over the past couple of years investment holdings of gold have risen by only about 3,500 tons. Comparing the total value of all investment holdings of gold at the end of 2007 with the end of 2010, we find that such holdings have risen by about $600 billion in value over that time, about $150 billion of which was due to a rise in the actual quantity of gold held for investment purposes, and the remaining effect due to the rise in the price of gold.

How much of a net inflow of money into the market for investment gold would have been necessary to cause the rise in the price of gold that we’ve witnessed recently? We can’t say for sure without having a lot more specific data about supply and demand with which to estimate how sensitive the price of gold is to various factors. But we can put an upper limit on it: at most, the net influx of funds into the market for investment gold that lead to a near-doubling of the price of gold since 2007 was $600 billion (since that was the total increase in the value of investment gold).

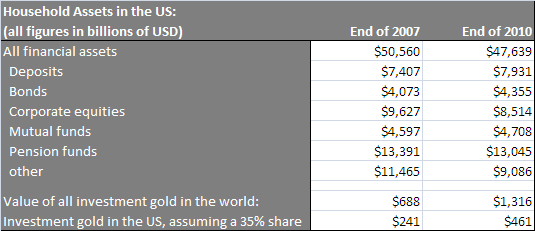

In reality, it was almost certainly far, far less than that. If it takes an inflow significantly less than $600 bn to double the price of gold, it’s reasonable to guess that a net influx of $100 bn, or probably even $50 bn per year into the market for gold investments would be enough to push the price of gold significantly and steadily higher. This is a small number, compared to the tens of trillions of dollars worth of other sorts of financial assets owned by households. See the table below for a summary of the financial assets owned by US households in recent years. (Source: Federal Reserve Board Flow of Funds data: pdf.)

So moving just 0.1% of the financial wealth of US households into gold could be enough to have a substantial impact on the price of gold. Note that the same can not be said of other asset prices that we care about; it would be difficult to discern any price effects whatsoever of a move of $50 billion more or less per year flowing into the stock market (valued at over $50 trillion around the world), the bond market (also with a total value in the tens of trillions of dollars), or real estate.

Given all this, what can we say about the steady rise in the price of gold in recent years? This analysis suggests that seemingly small phenomena could have big effects on the price of gold. For example, the increased demand for gold jewelery among millions of newly well-to-do households in China and India could be enough to do it — if 5 million families per year each acquire a couple of pieces of gold jewelery (say perhaps 3 oz of gold), that would represent an increase in the demand for gold of $25 bn per year.

It’s also conceivable that a good advertising campaign by gold producers could be enough to move the price of gold. Imagine that an effective, sustained advertising campaign, targeted at wealthy, conservative individuals in the US, is able to persuade 25,000 of them per month to switch a portion of their financial assets into gold. (Note that the target audience would be those roughly 3 million US households that have over $1 million in financial assets.) Suppose for the sake of argument that each of them is persuaded to shift just 5%, or $50,000, of their portfolio into gold. Such an advertising campaign would have the effect of pushing $15 bn per year into the market for investment gold — very possibly enough to have a significant impact on the price of gold, given how small the overall market for gold is.

Note that a very similar thing happened to the market for diamonds in the middle of the 20th century. The DeBeers diamond cartel used an incredibly successful advertising campaign in the 1950s to cement the idea of the diamond as the premier gemstone, and in so doing permanently changed the value of diamonds.

Whether or not you like that analogy, the central point here is a very simple one. Since the market for gold is so small, its price may be strongly affected by things that have nothing to do with the economy. And since the price of gold tells us nothing about the state of the economy, it should no longer be considered to be a meaningful economic indicator. So I think that it’s time to drop the price of gold from our daily headlines.

I find it funny that a professor straight out of the heart of academia, as well as someone who has specific ties to the Federal Reserve and the HUD which played such a serious role in destroying the American housing market, would come out and dismiss gold so specifically. Similarly, his blatant smear that it’s merely rich, conservatives that are buying gold is pretty telling.

Hey Mr. Mason, you statist, You’re an idiot. How about central planners such as yourself quit destroying the value of the labor of working citizens such as myself? How about you and your ivory tower friends quite debauching the country with your fiat currency schemes so that some modicum of freedom and liberty still exists for our children and grand children.

The rise in gold has correlated with the rise of real inflation. Core inflation which is referred to in this chart and often used by the government is not a true indicator. So far this year, Gold has lost value against the Swiss Franc because it has not devalued it’s currency. The dollar, euro, and other currencies have lost their purchasing power due to excessive debt and the money printing to service that debt. Yes, there is a fear factor involved as people diversify into gold, but this is real, brought on by the overprinting of fiat paper money.

Should We Care About the Price of Gold? Sir, we SHOULD very much care about the price of gold, cheifly because OTHERS CARE about the price of gold. They cared so much, that my portfolio is now back on track, I can retire, AND I can pay off my debts. That would not have happened should I have kept my savings in invested in stocks.

i think one of the most MISinforming articles…..articles like this should be dropped from the headlines

‘small’ market?

From wikipedia:

The average daily volume of gold and silver cleared at the London Bullion Market Association (LBMA) in November 2008 was 18.3 million ounces (worth $13.9 billion) and 107.6 million ounces (worth $1.1 billion) respectively. This means that an amount equal to the annual gold mine production was cleared at the LBMA every 4.4 days, and to the annual silver production every 6.2 days.[1]. The Gold Anti-Trust Action Committee claims that clearing data substantially understates the true amount of gold traded, due to the netting of trades in the calculation of Clearing Statistics.[2] They claim the LBMA market is $5.4 trillion a year.