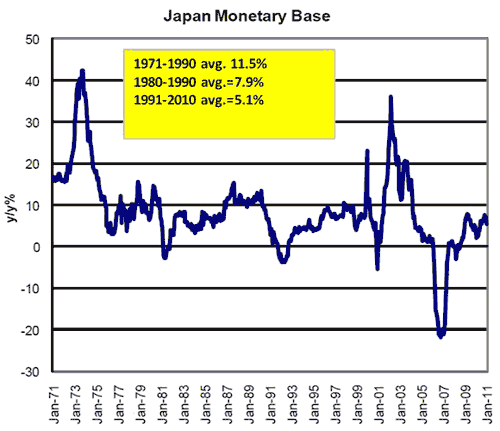

Michael Darda sent me some interesting information about the Japanese monetary base:

There are several ways of looking at this data. The growth in the base over the past 20 years has been much slower than during the previous 20 years. Thus it would be hard to claim QE didn’t work in Japan, as they didn’t even increase the base half as fast as when they weren’t doing QE.

On the other hand during the past 18 years Japan’s NGDP has been relatively flat. So the growth rate of the base was much higher than NGDP, suggesting a falling rate of base velocity. That does make QE look ineffective. Especially when you consider that there were brief periods when base growth soared to nearly 40%.

But an even closer look as the data shows that these spurts in base growth were temporary, and were partially rescinded just a few years later. Note the QE in the late 1990s when deflation first became a major problem. Then the small drop in the base just a year or two later. There was an even bigger bout of QE in the 2002-03 recession, followed by a much bigger drop in the base after the economy picked up a bit. This doesn’t show that QE doesn’t work; it shows that temporary monetary injections don’t have much impact on NGDP. But we already knew that, in fact it’s rather obvious if you think about it.

How do I know that the base declines in 2000 and 2006 were not just random? How do I know the BOJ was intentional tightening policy? Because on both occasions the BOJ raised interest rates, which is something no central bank does in a liquidity trap. Ever.

Some people look at these facts and see a central bank that was powerless to boost NGDP. That seems crazy to me. Why would a central bank trying to raise NGDP reduce the monetary base? Why would they raise rates? Here’s an alternative view. Suppose the BOJ was trying to prevent inflation. Then every time the CPI inflation rate rose up to zero, they would tighten policy. If my hypothesis is correct, then what type of path would one predict for the Japanese monetary base? The answer is surprising; almost exactly the path that we actually observed. Here’s why:

- Because the trend rate of inflation fell sharply between 1970-90 and 1991-2010, nominal interest rates fell close to zero (the Fisher effect.) This would produce a large increase in the real demand for base money, or a large fall in velocity. And that’s exactly what we observed in Japan after 1990.

- When near the zero bound, the demand for base money will not be stable. When conditions are depressed, the demand for money will pick up somewhat, and the BOJ will have to inject large amounts of base money to prevent severe deflation. That’s the late 1990s, and 2002-03. When things pick up a bit the demand for money will fall, and the BOJ will have to remove a significant amount of base money to prevent inflation. And that’s what happened in 2000 and 2006.

- But they won’t remove all the base money injected earlier. Recall that at near zero interest rates there is that permanent increase in the demand for liquidity.

Bennett McCallum once proposed that the Fed adjust the monetary base to offset changes in velocity during the previous quarter. That would keep NGDP relatively stable. I seem to recall McCallum proposed that NGDP be allowed to grow at a modest but steady rate. The Japanese seem to have basically adopted this policy, but with a zero percent NGDP growth target. No, I don’t believe they are consciously behaving this way, but it is interesting to consider that this is almost exactly the way the BOJ should behave if it wanted to keep NGDP constant, or the NGDP deflator falling at about 1% per year.

So QE did work in Japan. They got steady NGDP. The next question is why they acted as if they had such a peculiar policy target. Some people tell me that “Japan” likes low inflation because they have lots of old people on fixed incomes. But “Japan” isn’t a person, it’s a country. Japan didn’t decide to follow a policy of stable NGDP, the BOJ did. At the very same time the BOJ was deflating the economy the Japanese fiscal authorities were aggressively trying to boost NGDP through expensive construction projects, which have put Japan deeply in debt. The BOJ sabotaged those efforts. No, “Japan” did not adopt a stable NGDP target (or mild deflation target), the BOJ did. That’s even more peculiar.

This story doesn’t get told nearly enough. IMHO. It will be interesting to see how it ends…