U.S. Treasuries over the last two years have served as sort of a safe-haven for investors (something that still has gold bugs scratching their heads). But with the worst of the financial crisis over, and growing evidence of U.S. and world economic expansion, there is good reason to believe that long-term real interest rates are likely on the way up (reflecting the increasing world demand for investment).

Ceteris paribus, higher real rates also imply higher nominal rates. That’s bad news for treasuries. And though the Fed has promised to keep inflation in check (around 2% per annum), the market might have different ideas concerning the Fed’s willingness and/or ability to deliver on its promise. Market expectations of inflation appear to have risen lately. Via the Fisher relation, one would expect this to put further upward pressure on nominal interest rates. Again, this is bad news for treasuries.

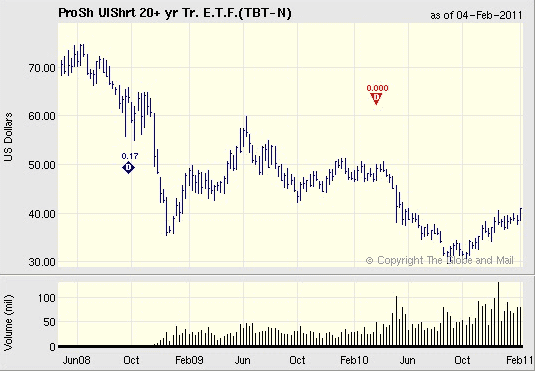

Note that I am not personally making any forecast about where interest rates are likely to go in the future. All I want to say is that IF you believe nominal interest rates are likely to continue their way upward, you may want to play this by shorting U.S. treasuries. And an easy way to do this is to go long on the Proshares Ultrashort 20+ Treasury ETF; see recent performance below (on Canadian exchanges, try ticker symbol HTD).

What could go wrong with this trade? Well, the fact remains that U.S. treasuries are likely to retain their role as a safe-haven instrument, at least for the near future. So, surprise events in sovereign debt markets, for example, may very well make TBT tumble again. And then there’s the Middle East…what could possibly go wrong there?

Leave a Reply