A research paper by Eyal Dvir of Boston College and Ken Rogoff of Harvard suggests some interesting parallels between the recent behavior of oil prices and what was observed at the very beginning of the industry. I’ve been doing some related research on the history of the oil industry that looks into the events behind historical oil price shocks. Here I describe the first oil shock, which occurred a century and a half ago.

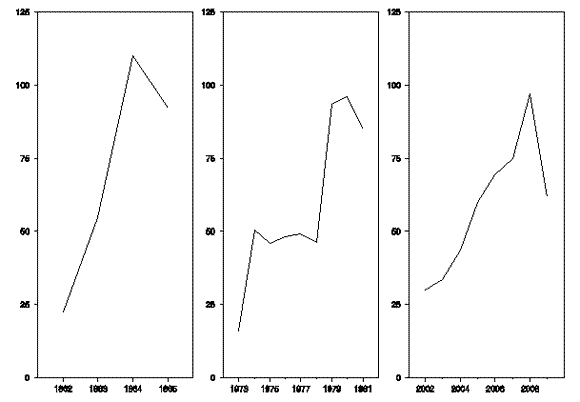

Price of oil measured annually in 2009 dollars per barrel. Left panel: 1862 to 1865. Middle panel: 1973 to 1981. Right panel: 2002 to 2009. Data source: BP Statistical Review of World Energy 2010

The far-right panel above displays the most recent behavior of the real price of oil, following the price as it rose from about $30 a barrel in 2003 to almost $100 a barrel on average during 2008. In terms of the magnitude of the real price increase, that’s pretty similar to what happened over the decade of the 1970s (middle panel), and amazingly also very similar to what happened during the U.S. Civil War, a century before OPEC even existed (left panel). I was interested to take a look at what happened to produce the first oil shock of 1862-1864.

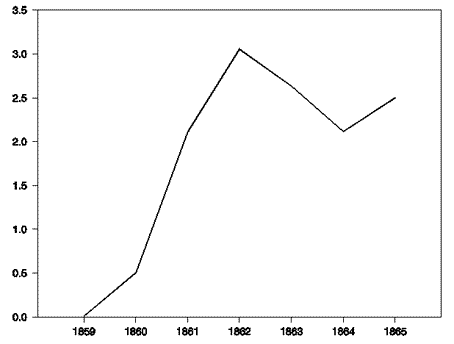

Edwin Drake had drilled the first commercially successful oil well in Pennsylvania in 1859, three years before the left panel begins. Prior to that discovery, people had been getting illuminants from sources such as whale oil, grain alcohol, and gas and liquids derived from coal, asphalt, and shale. Then as now, obtaining liquid fuel by these methods was a very expensive proposition, and Drake had no trouble selling his crude for $20 a barrel, which would correspond to $476/barrel in 2009 dollars. Needless to say, the discovery that such precious stuff could be obtained just by drilling into the earth stimulated a frenzy of drilling in the vicinity of Oil Creek, Pennsylvania. Many of these wells also successfully produced oil, and the price had plummeted below 50 cents/barrel (about $12 in 2009 dollars) by 1861.

But it turned out that in each new well, the flow rate dropped fairly quickly as oil was removed, and the drillers also had difficulty figuring out how to prevent water flooding. After an initial phenomenal rate of success, total production from all wells in Pennsylvania declined in 1863 and fell further in 1864.

Annual production (in millions of barrels per year) from all fields in Pennsylvania and New York, 1859-1865. Data source: Derrick’s Hand-Book of Petroleum (1898)

At the same time, the demand schedule was shifting to the right, due to war spending and most importantly a new tax on alcohol (a competitive source of illuminants) of $2/gallon, which gave a $40/barrel competitive advantage to crude. The result was that the real price of oil quintupled by 1864.

Fortunately, Oil Creek turned out not to be the only place oil was to be found in Pennsylvania. Yields from other, much larger fields in the state ended up dwarfing the modest volumes of the pioneer wells, driving the price back down. Production from the state as a whole would end up increasing by an order of magnitude from the levels of 1865 until reaching what proved to be its true peak in 1891. Today Pennsylvania produces only 1/5 as much oil as it did in 1891.

And, again fortunately, much larger fields were discovered in other states that ended up dwarfing the volumes produced in Pennsylvania. Oil production from the United States as a whole would continue to rise until reaching what proved to be its true peak in 1971. Oil production from U.S. fields today is about half what it was in 1971.

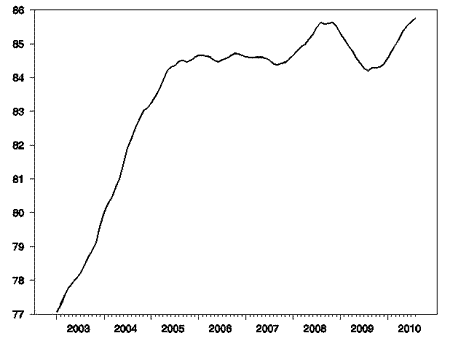

And, again fortunately, even larger fields were exploited outside the United States. World oil production continued to increase until reaching a bumpy plateau in 2005. Just as the price path since 2005 parallels that seen in the 1860s, so does the graph of world oil production.

World oil production, 2003:M1-2010:M9. Includes lease condensate, natural gas plant liquids, other liquids, and refinery process gain. Data source: EIA

As for where world production is headed from here, if optimistic projections from Iraq are borne out, the global peak is still ahead of us. But when the global peak will arrive is a bigger question than I want to take on at the moment, so let me just make two quick observations now. The first is that, although economists are used to thinking about increased production as coming from technological progress, in the case of the oil industry the biggest factor has instead been the exploitation of alternative oil fields that proved to be much bigger and better than the originals. As production from each one fell, so far there has been something better to replace it. But I do not understand those who conclude that this will always be the case, or who assume that the outcome is necessarily subject to the control of technology or incentives. Second, I submit that when demand booms and production is stagnant, it is possible for the price of oil to quadruple in a short period of time.

I say that because that’s exactly what we’ve seen happen on three different occasions.

Leave a Reply