Krispy Kreme Doughnuts (KKD) has gone through a massive turnaround, and both analysts and investors are noticing. Shares have surged lately and should be garnering more attention as it recently passed an important price point.

While the growth rates are fantastic, they are also reasonably priced for this Zacks #1 Rank (Strong Buy).

Company Description

Krispy Kreme is a popular chain, selling signature doughnuts and coffee. The company has been around since the 30’s and now as more than 630 locations in 20 countries.

Unexpected Profit

In the most recent quarterly report, on Sep 2, Krispy Kreme reported EPS of 1 cent, while the analysts polled by Zacks were expecting a 3 cent loss. Revenue for the period was up more than 6%, to $88 million. Same store sales for company owned stores were up for the 7th consecutive quarter, rising 5.7%.

Krispy Kreme also raised its full-year guidance in that same press release. Operating income is now expected to land between $13 million and $17 million, lifting both ends of the range by $2 million.

Consensus Doubled

After the earnings release, the Zacks Consensus Estimate doubled, to 14 cents for fiscal 2011. Last year the company earned 6 cents, making the anticipated growth rate 133%.

Next years forecast rose 6 cents, to 24 cents, projecting a 71% growth rate.

Valuation Picture

The foreword P/E is a tough pill to swallow for some, at 38 times. However, the value in KKD comes from the expected growth. The PEG ratio is just 0.8, which is well ahead of its peers.

Krispy Kreme is the highest rated restaurant, out of 43, on Zacks.com.

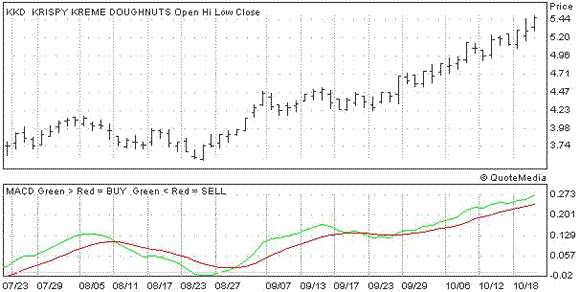

The Chart

Krispy Kreme has been through a massive transformation and is now back on the upswing. Now that shares have headed back above the $5 mark, they should see some more institutional attention. Many funds can not invest in stocks below $5, so we could see an uptick in volume adding fuel to the rally.

Leave a Reply