The Bear’s bear, David Rosenberg, opines that it is not earnings but changes in earnings expectations that drives the market:

The Bear’s bear, David Rosenberg, opines that it is not earnings but changes in earnings expectations that drives the market:

[T]he peak in earnings forecasts coincided with the peak in the market [in April].And guess what? The forecast peak in the last cycle was in October 2007, again right when the S&P 500 was hitting its highs. Before that, earnings estimates were starting to get cut in August 2000, just ahead of the peak in the market.

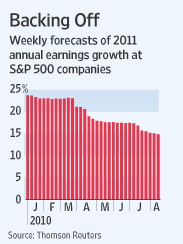

In Ahead of the Tape this morning, the WSJ supported this point of view. Q2 earnings were strong across the S&P: up 38%, well above the expected 27% YoY increase. Yet the market is dropping – and began to fall just as earnings forecasts began to be revised downward for 2011 (see chart). 2011 earnings estimates started in January at 25% growth, were reduced to 20% in April, and now are hovering at under 15%. The change of view:

[T]allies with the outlook for broader economic growth, which has weakened considerably.

Even the 15% prediction may be revised downward, as it is nearly triple the expected GDP growth for 2011, which itself is being revised downward. Goldman this morning is urging analysts to cut GDP estimates even further, to the range of 1.5% in 2H10 and early 2011. Yet as recently as the last week of June, before the poor GDP report, the WSJ was touting only modest decrease in earnings expectations:

At the time earnings were expected to rise in the second half of 2010. No longer.

We may be at “Peak Earnings“:

If the macro economic data continues to disappoint to the downside (as JP Morgan suggests) then it’s clear that analysts have been fooled into believing that the stimulus and 80% rally are self sustaining.

Clearly analysts have not yet fully embraced the economic slowdown. Why not? Using an expectations model from The Pragmatic Capitalist, they may have overshot mean reversion on expectations too much to the positive, and are due for a double dip there, too:

Leave a Reply