In the most recent economic forecasting survey by the Wall Street Journal, 23 percent of the surveyed economists said consumers spending more readily than anticipated is the biggest upside risk of their growth forecast for the second half of the year. So anything that can shed light on future spending habits is of particular interest. Two of the most commonly cited measures of consumer attitudes are the Conference Board’s Consumer Confidence Index and the Thomson Reuters/University of Michigan’s Index of Consumer Sentiment. A key question is, do these indicators improve consumption forecasts?

Previously, economic researchers have looked at the predictive power of these indexes for consumer spending, and they generally found that the ability of consumer confidence measures to predict consumer spending largely disappeared once some other measures of economic conditions were taken into account. One such example is a study by Sydney Ludvigson, which examined the forecasting record of these confidence measures through 2002 (for other examples, see here and here). Much has happened since then, of course, and a simple inspection of the two series reveals that both confidence measures fell fairly steadily starting in August 2007 until reaching near-record lows by June 2008. Therefore, a look at the more recent predictive track record of these indicators seems warranted.

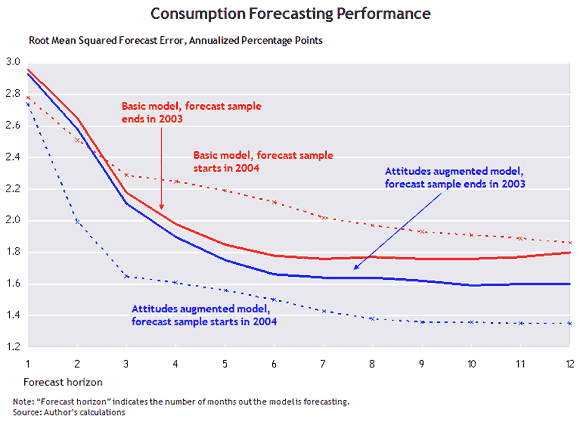

For this examination, we conducted an out-of-sample forecasting experiment using a pair of statistical models (technically, Bayesian vector autoregression models). The first model predicts real personal consumption expenditures as a function of its own past values and past values of other variables such as real measures of stock market prices and disposable personal income. The second model includes all of these variables augmented by the two measures of consumer attitudes. At each point in time we use only the data that would have been available to forecast real consumption data anywhere from one to 12 months out. (For example, in the middle of February 2009, consumption data would have been available through December 2008 while some of the other variables would have been available through January or February 2009. The experiment is not “real time” in the sense that we use the latest vintage of data, which include revisions to the historical data that would not have been available to forecasters at the time.) Forecasts of consumption are made for the 1990–2003 period and then again for the period from 2004 to the present. The root mean squared forecast error is used to gauge the accuracy of the forecasts, with smaller numbers corresponding to smaller misses on average. As the accompanying chart shows, adding the two measures of consumer attitudes improves the forecast much more in the post-2003 sample than in the earlier period.

We experimented with some variations in specifications of the model, and we were unable to overturn the general finding that adding attitude measures to the model resulted in an improvement in forecasts in recent years. We found this fact intriguing and somewhat surprising.

A recent paper by Barsky and Solon argues that the Index of Consumer Sentiment reflects the public’s awareness of economic conditions. In fact, the survey used to construct this index asks respondents about recent news they have heard related to changes in economic conditions. From August 2007 to June 2008, news of “unfavorable higher prices” was frequently mentioned in the survey. A study by James Hamilton showed that part of the deterioration in the Index of Consumer Sentiment during this period could be explained by rising energy prices. However, adding a measure of oil prices to our model did not overturn the basic finding of improved consumption spending forecasts in models that included measures of consumer attitudes.

It remains an open question why these measures of consumer attitudes have become more useful in recent years. A statistical anomaly, greater or more accessible news coverage of the economy, and a generally more aware public are all possibilities. If it is just luck, then time will eventually overturn the result. But if these consumer attitude indicators have become a more useful summary of a wide variety of developments in the economy, then their forecasting power will persist. Time and further research will help sort this out.

Leave a Reply