A friend noted an interesting indicator yesterday of a growing split among FOMC participants. The clue is found in the little-read minutes of the Board of Governors’ meetings on the discount rate. For those who don’t know, each Federal Reserve Bank board of directors is required to make recommendations every two weeks on where they would like to set the discount rate. The recommendations are staggered so that the Board of Governors has a “live” recommendation should it desire to change the discount rate. Legally it may not change the rate without a recommendation from at least one reserve bank.

The discount rate recommendations are those of the bank’s board of directors and not the president, who simply discusses proposed changes with his or her board. On the other hand, the president’s vote or position at the FOMC is not that of the bank’s board of directors. Nevertheless, the president and bank’s board are usually in sync, and it is unusual to find significant differences on policy that persist. Furthermore, because the discount rate has for some time now been set at a fixed spread above the funds rate, a movement in the discount rate provides a strong signal about the reserve bank’s board’s preference for the federal funds rate and presumably the president’s preference as well. Right now the discount rate is 50 basis points above the upper range of the FOMC’s funds rate target of 0–25 basis points.

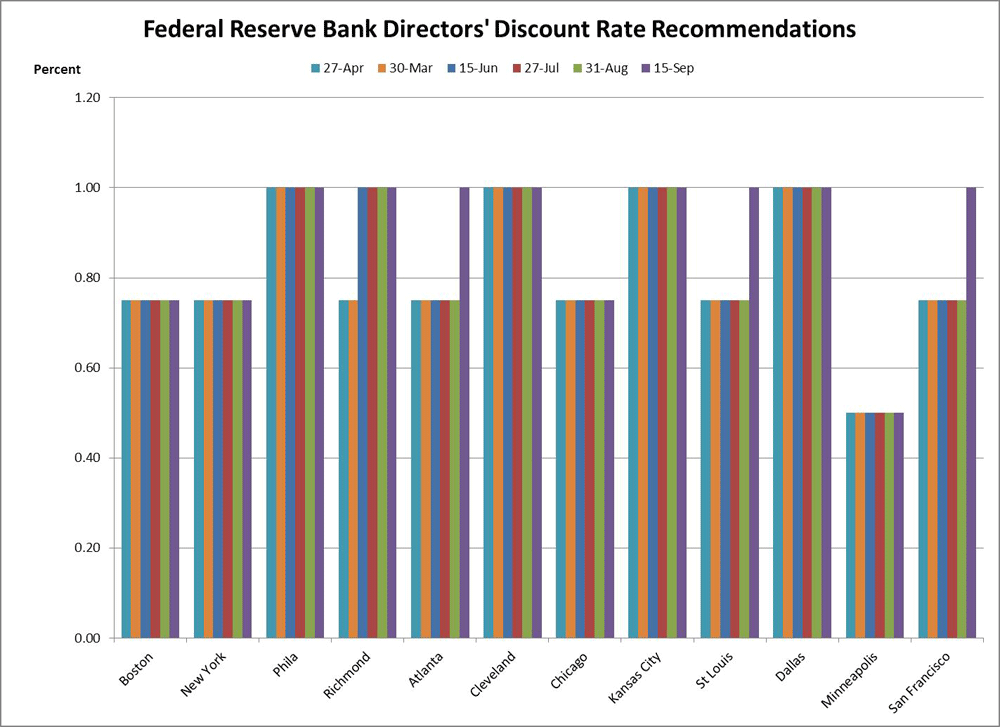

Because of the close relationship between a reserve bank president and his or her board of directors, the recommendations on the discount rate provide an important clue as to where each Federal Reserve Bank president may lie on the spectrum of those favoring a more prompt move in the federal funds rate and those who may be more dovish. The following chart shows the time path of the discount rate recommendations for June through September. The recommendations in September were made prior to the FOMC’s September meeting.

(click to enlarge)

The chart reveals several interesting facts about the views of the various Federal Reserve Banks and how those views have evolved. First, five banks (Philadelphia, Richmond, Cleveland, Kansas City, and Dallas) have all been submitting proposals to hike the discount rate since June, and four of these have been consistently recommending discount rate increases at least since April. Not surprisingly, the presidents of those banks have, for the most part, been outspoken advocates for moving sooner rather than later, with Jeffrey Lacker of the Richmond Fed dissenting from FOMC decisions because he favored raising the funds rate. Similarly, three banks (Boston, New York, and Chicago) have consistently favored keeping rates at their present levels since April. Again, their presidents have openly advocated a cautious approach. The interesting change in September is that the boards of directors of Atlanta, St Louis, and San Francisco joined the five others favoring a discount rate hike. Their presidents in recent speeches have also gradually signaled their willingness to consider rate hikes sooner than later. Finally, the Minneapolis Fed has consistently over the entire period urged a 25-basis-point cut in the funds rate, and this likely matches the negative funds rate that the Minneapolis bank president most likely submitted in his recent SEP projection.

What this means is that there is now a solid majority of eight bank presidents favoring a move. They are positioned opposite the Board of Governors, who have consistently rejected the proposed rise in the discount rate. Thus we see an interesting split of eight reserve banks presidents on one side and a coalition of four bank presidents and the Board on the other. That New York would be so positioned is no surprise because President Dudley is vice chairman of the FOMC. This split suggests a fractured committee, and to some this is a big concern.

Finally, it is noteworthy that both Governor Brainard and Governor Tarullo have publicly argued in recent speeches and interviews that caution and risk management argue for delay and perhaps postponement of a funds rate increase this year. Indeed, Governor Brainard expressed confidence in the FOMC’s ability to counter any unanticipated acceleration in inflation. However, she probably has little knowledge of the protests, picketing, and shipments of nail kegs of keys and two-by-fours that flooded the Board in the wake of Chairman Volcker’s policies to break the back of inflation in the early 80s. These governors’ remarks reflect perhaps too much confidence in the FOMC’s ability to react to inflation and suggest that the gap between the presidents and governors may be widening.

Another view, especially for those who are prone to count dissents and harp on such disagreements, is that the existence of differing views is not a sign of a lack of leadership or a problem. At a time like this, when the FOMC is in unchartered waters, one would expect and hope that reasonable people would disagree. The existence of a wide range of views is to be expected. Furthermore, it is clear that those differences are being aired and openly discussed. This is a sign of a healthy institution. Debate takes place, and consensus is reached. This also suggests, however, is that there is no reason why all the presidents should not have an equal vote? The voting composition of the FOMC will change significantly, and the new mix of views will likely shift the balance of power significantly more towards those favoring a policy move. There is little justification for changing policy just because the composition of voting members changes.

Leave a Reply