The Swiss National Bank move to eliminate the 1.2 EURCHF Peg has proven to be a big market/media event. Follows a few random thoughts on how this story played out. Caveat – Some of this is wonkish, some guesses on my part.

The Weekly FX Flows

The FX market has two different types of risk profiles depending on what day it is. The two risk periods are:

- Monday through Friday

- Friday night through Sunday night

There are risks that the FX market participants face every second of the week. But the risks of the weekend roll are much higher than the Monday through Friday trading period

The developments during any given week may cause wild gyrations in FX pricing, but there is also a very active FX market to lay off, or take on risk. The FX market runs 24/7 from Monday morning in Asia until the close in NY on Friday. From Friday night to the next opening in Asia there is no market to lay off risk.

The fact that there are two different risk periods creates two classes of participants in the FX market. Short-term players who are trying to make a buck, but have no interest in taking positions over the weekend. And those who are taking a long-term view of the world, and are happy to take the risks associated with liquidity over the weekend. For every player who takes a long view there are 20 who only dance from Monday through Friday. The bulk of the actors are squared up for the weekend.

There is a very logical reason for this. Over the past twenty years the vast majority of “surprise” critical steps taken by government authorities have been taken on Sunday evenings. (Devaluations/revaluations, Fannie and Freddie going bust, TARP etc., Plaza Accord, Louver Accord) If you’re in the FX Biz you pay very close attention to what surprises may have been released when the markets have gone dark. And depending on your risk profile you want to be square for the weekend.

The SNB broke the “rules”. It dropped its bomb on a Thursday. It did it at a time that insured that the NY market was still asleep.

The SNB could have held off for a few days and made their big announcement on Sunday. The amount of gross positions outstanding on Sunday would have been a fraction of the positions that were outstanding on Thursday morning. Obviously, the timing by SNB was very deliberate. They acted in what I consider to be a hostile manner – the SNB was a predator to the market participants. Not very sporting at all.

If the SNB had acted in a manner consistent with how Central Banks/Government make announcements of key changes to policy, the losses incurred by the market would have been far less than what they were. The retail accounts that have been blown away this week would not have suffered anywhere near the losses they did. I would add to this that if the announcement had come over the weekend there would not have been a 20% move in the CHF. The adjustment would have been closer to 10%.

My conclusion is that the SNB deliberately screwed the market, and in the process shot itself in the foot for 30-50 billion dollars. What were they thinking?

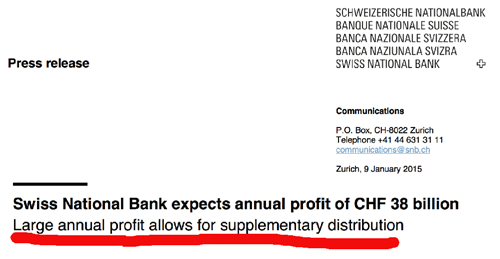

Did the 2014 Profits Play a Role in this?

Every January the SNB produces its annual profit and loss results. The surprise in 2014 was the size of the gains the SNB reported (CHF38B) . The headline from this year’s profit report:

38B Francs is a huge amount of money. This treasure chest is equal to about half of the losses the SNB incurred when it floated the franc. My question is did the folks at the SNB already know that they were going to pull the plug on the peg on January 9 when they released the profit report?

The huge profit report plays into the story, but I’m not sure if the way it was introduced allows for a definitive conclusion that the decision to float had been made six days before the actual event. My read of these tea leaves is that the SNB was, at a minimum, considering the float on January 9, but had not yet made a final decision on when to act. The “profits” gave the SNB the ammo to take the huge loss. My question – Were the 2014 “profits” pumped up so that it would be “easier” for the SNB to act? I think there is a real possibility that those big gains were largely fluff.

On the SNB communication of January 6th

A very curious element in this is that three days before the float an SNB spokesperson, Jean-Pierre Danthine, had this to say:

“We took stock of the situation less than a month ago, we looked again at all the parameters and we are convinced that the minimum exchange rate must remain the cornerstone of our monetary policy,”

What to make of this? Was Jean-Pierre lying through his teeth when he said these words? Had the decision to float already been made?

I’m 100% convinced that the decision to float was made prior to the time that J.P. spoke. In other words J.P. lied; he was part of a deliberate effort to set the market up to be short the CHF and to cause the maximum amount of pain to the market participants.

I doubt we will ever know the facts on this. However if JP was tied down and water boarded he might fess up to being the guy who deliberately set up the market. I’m as certain as I can be that good old J.P. would not have said these words without the blessings of the head of the SNB, Thomas Jordan. So it is quite possible that this critical lie was set up by the guy who is running the show.

If this is correct, it is a heinous act. I would think that there would be lawsuits if it could be proven that the SNB deliberately set up the market – billions were lost as result of the J.P. statement. (where is that water-board when you need it?)

Jordan Acts Old School Style

Jordan must have read from Paul Volker’s playbook. Volker was famous for his “surprises”. During those years I was on an FX trading desk. We were always afraid of the “Volker Factor”. Markets were under siege by the Fed. As a result, positioning was kept light, and market liquidity suffered. The “fear factor” worked to Volker’s advantage, but even he would would admit that he was responsible for a great sucking noise in the markets. Volker succeeded, but the costs were very high.

Central Bank communication policy has morphed over the past 20 years. The changes were led by Greenspan who established the concept of ‘guidance’. The Fed became more open as a result. By communicating its intentions the Fed was able to steer capital markets in a way that suited it. The strategy of communication was designed to minimize the market shocks of unanticipated policy changes. For the most part, the policy of providing forward guidance has worked. Ben Bernanke took another leg up on the idea of communication as a means of guiding markets. Most other central banks have followed this policy.

But the SNB went entirely in the other direction. On Tuesday it said, “That will not happen”, three days later it happened. Thomas Jordan and his merry men at the SNB turned the clocks back 40 years.

There was No Crisis on Thursday

When the SNB established the Peg in 2011 there was a true market crisis going on. In a short period of time the EURCHF fell from 1.5 to parity. The SNB introduced the Peg in the same manner that they have taken it off. It came as a surprise to the market, it caused an immediate 20% jump in the EURCHF. Pretty much the exact opposite of what happened on Thursday. One could argue that if the SNB went “Shock and Awe” when the peg was established, it is equally fair that they took it off with the same Shock and Awe.

BUT – There was no market panic last Thursday. There was no crisis that forced the SNB to act on that day. The EURCHF was trading above the peg, it had been for days prior. The SNB had some bids in the market to ensure that there was no move to the 1.2000 level. The intervention required to maintain the Peg in the days just prior to the float was very small – under 10b CHF.

My point is that there was no compelling reason to act on a Thursday. Therefore the only conclusion I can draw is that the SNB acted in a malicious way. It took actions with the express intent of hurting the markets. It achieved its objectives. In the process the SNB incurred losses that are 50% higher then they might have otherwise taken.

What are the Other CBs Thinking?

As of last Thursday every Central Bank on the globe hates the SNB. Not only did the SNB destroy its own credibility, it undermined the credibility of every other CB. How many headlines like this have we seen the past few day? (hundreds).

I’m convinced that the SNB move has put the ECB (Mario Draghi in particular) in a very difficult position. I expect that we will see markets converging on the ECB in the not too distant future. The empty promises of Uncle Mario are now just that – empty promises. Draghi’s job has just become incredibly more difficult – if not impossible.

The Japanese CB is now quaking. They have just observed first hand what happens when CBs take a U-turn. The BoJ has made more promises than any other CB. If the markets come to doubt the resolve and promises of the BoJ then you can kiss off any chance that the BoJ will succeed. A loss of confidence means that Japan will soon slip into another lost decade.

Any CB who is now managing a fixed currency is at risk. Hong Kong, China and Korea come to mind. If (when) any of these CBs come under attack they will face the same fate as the Swiss. The reality is that the global markets are much larger and more powerful than the CBs. What happened in Switzerland will be repeated elsewhere. It’s likely that these attacks will happen fairly soon.

What About the Players?

I do feel a bit sorry for those who lost big on the CHF move. I think they were set up, and lied to by the SNB. If the SNB had acted on a Sunday we would not be reading about all of the retail losses. The same is true for the big banks that got whacked (JPM, Citi, Deutsche, Barclays, and the many more who will soon be fessing up.

But – The losers were idiots! What were those thousands of retail investors thinking? In any market a player must think about risk and reward. The “reward” of being long the EURCHF on Thursday was maybe 25BP. This was obvious as the EURCHF had traded the last three days a few ticks away from the intervention zone. There were caution flags flying. Anyone who thought there was some free money on the table made a huge mistake. The downside risks of the short CHF was at least 100Xs what might have been realized if the SNB had not acted. YOU NEVER DO THIS! Never take a 100 to one shot. To bet $100 to make $1 is just stupid.

The retail brokers providing FX executions for retail have been buried with losses. I couldn’t be happier with this result. These clowns were providing 50X leverage to unsophisticated investors who did not understand the risks? They deserve to be wiped out.

There might be a few of these brokers left standing in a week – but I promise you the the days 2% margins on retail FX are over. Want to play in the FX sandbox? Be prepared to put 20% down. There are no profits left with that leverage, so the retail FX biz will disappear for a few years. (It will come back – greed trumps logic every time.)

Leave a Reply