Rather, there is a 2% upper bound to the Fed’s inflation target. This is an argument that Ryan Avent, Matt Yglesias, Paul Krugman, and others have been making for some time. I am sympathetic to this view and have made the case that the Fed has been effectively targeting a core PCE inflation corridor of 1% to 2% over the past five years. The evidence continues to mount in favor of this view.

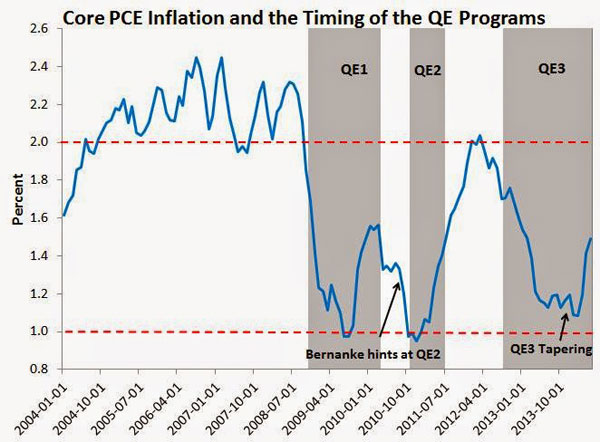

First, consider the timing of the Fed’s QE programs and changes in the core PCE inflation rate as seen below. The figure suggests that the FOMC iniatiates QE programs when core inflation is under 2% and has been falling for at least six months. It also indicates the FOMC tends to end QE programs when core inflation is above 1% and has been rising for at least six months. That ending of QE3 in October later this year follows this pattern.

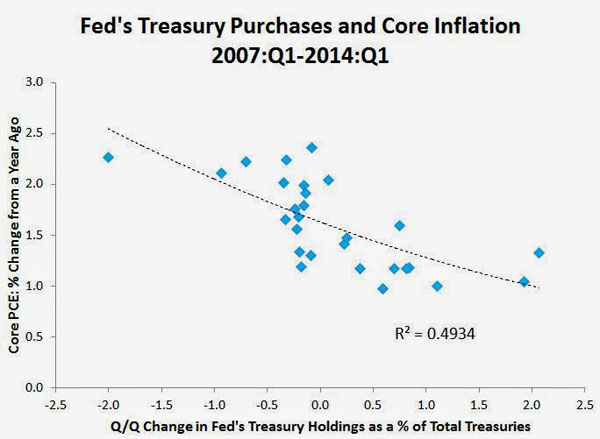

Reinforcing this point, the Fed’s purchases of treasuries since the crisis started is correlated with changes in core PCE inflation. Specifically, changes in the Fed’s holdings of treasuries as percent of all treasuries can explain almost half of the variation in core PCE inflation since 2007 as seen below:

Source: St. Louis Fed

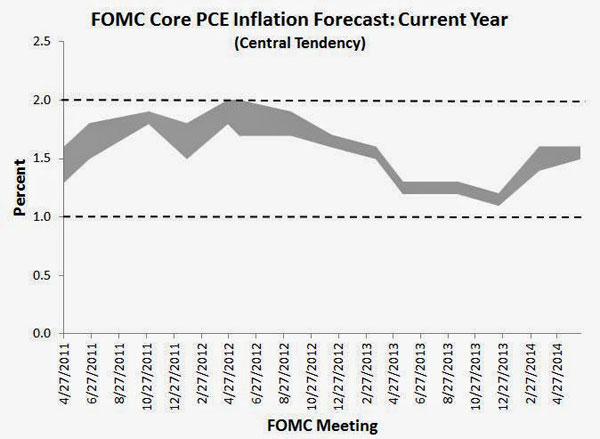

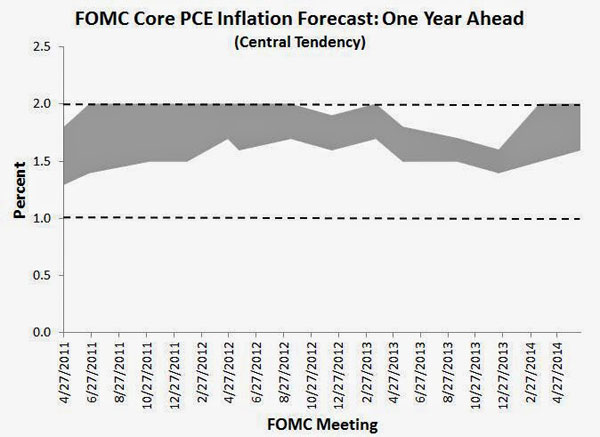

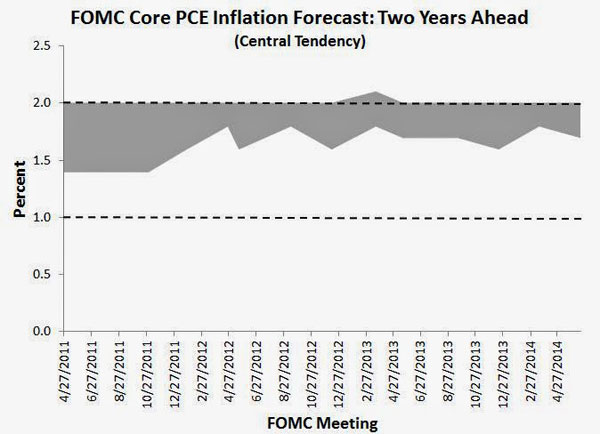

Second, consider the central tendency ranges of inflation forecasts provided by members of the FOMC. This information can be found in the ‘projection’ material. These forecasts are consistent with the observed core PCE inflation data highlighted above. They consistently show 2% as an upper bound.

Though it gets clearer with longer forecast horizons, the 2% upper bound can be seen in the current, one-year, and two-year inflation FOMC forecasts shown in the figures blow. A 1% lower bound is most evident in the current year forecast, but slowly gets higher at longer forecast horizons. (Note: not every FOMC meeting has projection materials, but for every meeting that does provide them they are lined up chronologically in the figures.)

FOMC members are predicting inflation no higher than 2% even two years out. Since the FOMC has meaningful influence on inflation this far out, this forecast reflects FOMC members’ beliefs about current and expected Fed policy. They see the Fed doing just enough to keep core PCE inflation under 2%. The actual core PCE inflation evidence provided above suggests the Fed is doing just that.

So it is all but official. There is no 2% inflation target.

Leave a Reply