Back in the early 2000s, the world economy was buffeted with a series of positive aggregate supply shocks: the opening up of Asia, rapid technological gains, and the ongoing liberalization of the real economy in many countries. These shocks expanded global economic capacity and implied higher future economic growth. In turn, there should have been a higher global natural real rate of interest given the higher expected economic growth. These shocks also should have resulted in more benign deflationary pressures that would have kept real wages up in advanced economies.

The Fed, however, did not allow this to happen because it feared the deflationary pressures. It loosened U.S. monetary policy and through the many countries that link their currency to the dollar, it also loosened global monetary policy. Even the ECB and Bank of Japan followed suit to some degree since they were mindful of letting their currencies become too expensive relative to dollar and the all the currencies pegged to it. In short, the Fed’s monetary superpower status allowed it to lower global real interest rates below the global natural real interest rate level during this time.1 This was an important part of the global housing boom story and the Bank for International Settlements (BIS) was all over it. It repeatedly told the Fed that its misguided fears of deflation were causing it to create a global liquidity glut. The BIS was spot on during this time.

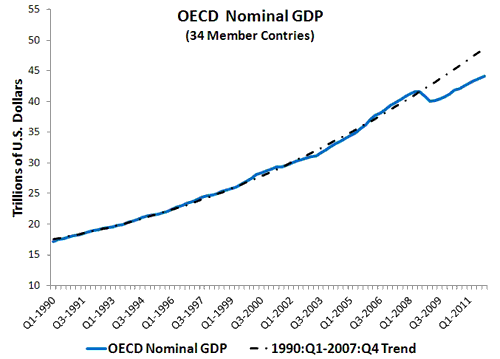

But that was then and this is now. The global economy is now being hit with negative aggregate demand shocks in Europe, Asia, and the United States. The economic outlook is dim and consequently the global natural real interest rate is depressed and is most likely negative. This time around the Fed, with help from the ECB, is keeping global real interest rates above the natural real interest rate level. In other words, global monetary policy is too tight now. This is evident in the figure below which shows that total current dollar spending for the OECD region is depressed.

The only way for such a drop in aggregate nominal spending to occur is for either the stock of money asset to decline or the velocity of money to decline. Central banks can meaningfully reverse both through better expectation management (e.g.. by raising the expected path of aggregate nominal income and spending). The fact that this has not happened and that OECD nominal GDP remains depressed is thus prima facie evidence that global monetary policy has been too tight.

The BIS, however, seems to be operating from the same manual it used in the early 2000s. It tries to argue that global monetary policy is actually accommodative. From its 2012 annual report:

In the major advanced economies, policy rates remain very low and central bank balance sheets continue to expand in the wake of new rounds of balance sheet policy measures. These extraordinarily accommodative monetary conditions are being transmitted to emerging market economies in the form of undesirable exchange rate and capital flow volatility. As a consequence, the stance of monetary policy is accommodative globally.

How could central bank policy be “extraordinarily accommodative” if measures of the money supply in both the Eurozone and the United States are declining? The BIS is falling for the interest rate fallacy here that Milton Friedman warned us about. Low interest rates only indicate loose monetary policy when they are low relative to the natural interest rate, as in the early 2000s. As noted above, this is note the case now.

Put it this way: does the BIS really think that fall in yields on 10-year treasuries from about 5.25% before the crisis to a low of 1.50% recently has been due to the Fed? It is more likely that global slump can explain most of the drop in yields. The fact that yields have remained so low is, if anything, an indication that monetary policy has been too tight. For were the Fed and ECB to raise expected nominal growth, yields would start rising again.

The BIS calls for monetary restraint are therefore way off. It needs to quit thinking like this is 2002 when global monetary policy was too loose and realize that it is 2012, the fourth year of tight monetary policy. The global economy is a far different beast today and policy makers need to respond appropriately.

P.S. Paul Krugman, Scott Sumner, [update: Ryan Avent,] and Isabella Kaminsky also raise questions about the BIS report. Kaminsky notes that what is really needed are more safe assets, something that U.S. Treasury could provide. I agree with her, but would note that if the Fed were to return nominal GDP to trend then it is likely that there would be far more privately-produced safe assets and thus less need for government securities. See here for more on this point.

Leave a Reply