It’s odd, but the best way to forecast price inflation is to look at wage inflation. In the years leading up to the Lehman crisis wage inflation ran about 3.4% and price inflation (PCE core) ran around 2.4%. The gap reflects productivity (and changes in the share of national income going to labor.) Headline inflation reflects core inflation plus food and energy. However food and energy are essentially unforecastable, at least if you look out more than a few months. So core inflation is the best way to forecast headline inflation. And core inflation is mostly wages, minus productivity gains.

For some reason core inflation slowed a bit less rapidly than wages over the past 4 and 1/2 years. PCE core inflation has run about 1.4%, whereas wages are rising at a tad less than 2.0%. But in the past 12 months the predictable pattern is coming into view. PCE core inflation has dropped to 1.05% (the lowest ever recorded), which is roughly 1% under wage inflation. Headline PCE inflation is down to 0.7%.

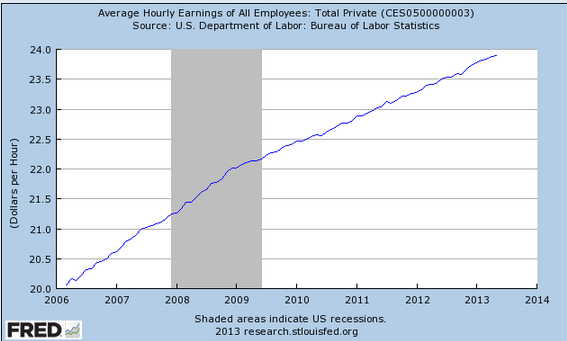

The following graph of average hourly wages tells you all you need to know about inflation since late 2008:

You can clearly see the inflection point in late 2008, when the asset markets crashed. Markets saw the huge disinflationary shock, but the Fed did not. It takes a lot of unemployment to suddenly drive nominal hourly wage growth down to 2%.

The trend in nominal wage growth seems unlikely to change soon. That means PCE core inflation will stay close to 1%, or a bit higher, and headline inflation will fluctuate unpredictably above and below 1%, because commodity prices are unforecastable.

The Fed will gradually become aware of the fact that money is too tight for it to hit its inflation target. That will give the doves the upper hand, and if I didn’t believe in the EMH I’d tell my readers to buy long term bonds—I think rates will stay low for longer than the markets currently seem to assume.

It’s odd that James Bullard is the only FOMC member who sees what’s going on.

Leave a Reply