Amazing drop in gold this morning. First Bitcoin last week, now Gold. It hasn’t declined this sharply since the prior all-time peak in 1980. One of the major goldbugs, Dennis Gartman, has written that in four decades of gold trading, he has never seen such a bloodbath.

Of course, if you follow this blog, you were well prepared, as Yves called this months ago.

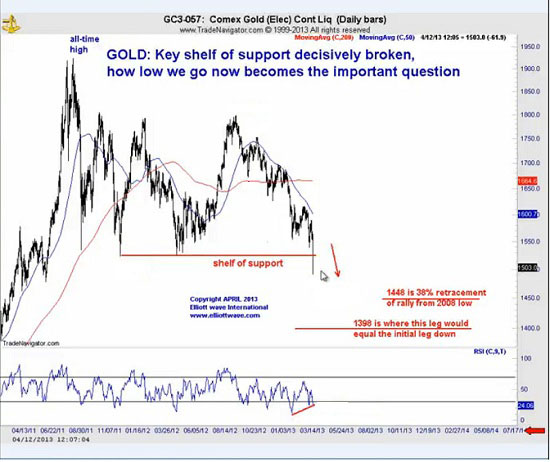

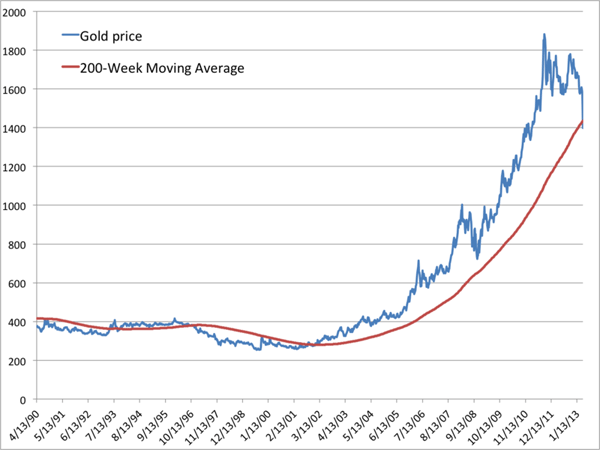

It now is entering what Prechter calls free-fall territory, as it has has busted below a support level (first chart) and a technical level (second chart):

Goldenfreude is the pleasure of seeing goldbugs lose their shirts. A lot of prosaic punditry trying to explain this, and getting it worng. Most of the immediate selling was out of Asia, and was caused by Abenomics, the shock and awe of massive QE by the Bank of Japan. Buyers of Japanese bonds may have been leveraging their purchases by using gold as collateral, and now are liquidating to cover as the Japanese bonds plunge. The proximate cause for the two-day rush to the doors is likely Friday’s China GDP report, showing a slowdown. Commodities are also taking a bath.

This should not have been “unexpected”, the common word used by mistaken punditry. We had two large gold sell-offs during the Great Recession, both driven by expectations of massive central bank intervention:

1) July 2008, right before the Lehman debacle and following on the heels of a parabolic blow off top in oil

2) September 2011, as the Euro crisis hit and central banks intervened

You cna see what the gold plunge is predicting: another bout of central bank intervention to keep the wheels from flying off the global ecopnomy. The first out of the blocks is the Bank of Japan’s QE. The punditry expects the massive BOJ QE to respark inflation. Gold is signaling the opposite, of deflation.

Milton Friedman got the punditry thinking that inflation was due to the increase in base money (central bank money and reserves), but this is too simple:

1) The Quantity Theory of Money had inflation as based on quantity times velocity of money. Velocity has plummeted in the Great Recession to levels BELOW those of the Great Depression.

2) Modern Monetary Theory has popularized the view that the quantity of money is not based much on base money, but on bank lending, as banks create the quantity of money. Put another way, banks do NOT lend out of reserves; they lend out of opportunity and then scramble to find reserves if needed.

The striking increase of bank reserves, and QE, have done little to spur bank lending; the reserves sit in the vault so to speak. Instead, QE has spurred excessive speculation in assets, what Minsky called the Ponzi Finance stage. Asset bubbles rage back and forth across commodities (oil! corn! coal! Bitcoins!), debt and margin are used to juice returns, and as each bubble collapses the velocity of money shrinks and the speculators fall back.

Japan is now (as John Mauldin aptly puts it), a “bug in search of a windshield.” Abenomics is leading to money washing back and forth across the globe, much as Hoover wrote in his memoirs about the sovereign debt crises of the 1930s. Is Cyprus the new CreditAnstalt? This is not how a real recovery begins, but how a false recovery ends.

Leave a Reply