It appears the answer to both questions is “yes.” The real question is why this seems so counter-intuitive. This post tries to explain some stylized facts discussed recently by Nick Rowe. He pointed out that Canada went into recession during 2008-09, despite no banking crisis. And inflation stayed stable at about 2% despite a significant output gap.

I’ll argue that an adverse supply shock caused by the plunge in global trade reduced Canadian AS, and pushed Canada into recession. Then the Bank of Canada tightened monetary policy in order to hold inflation down to the 2% target.

Many would argue the opposite; that a fall in global trade reduced Canadian AD, and the Bank of Canada did an expansionary monetary policy that kept inflation up around 2%, which is their target.

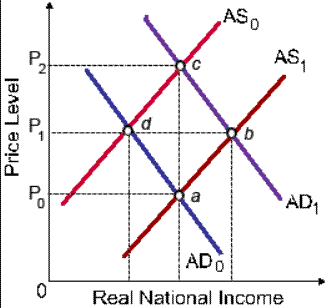

I wasn’t able to find a good AS/AD diagram, but this one will work, if we make a few assumptions:

1. Suppose we start with point b being the initial equilibrium; this is time=1.

2. Then Canada falls into recession, and both AS and AD decline at time=0. I.e. we reverse the graph’s dynamics.

3. Let the price level represent the rate of inflation. Hence steady prices on this graph imply a steady rate of inflation, at 2%.

In that case, Canada moved from point b to point d. Output fell but the inflation rate stayed stable. How can this be explained?

It turns out that the explanation is incredibly easy, incredibly straightforward. But only if you stop thinking like a Keynesian and start thinking like a market monetarist.

Let’s suppose that the BOC had been targeting NGDP in 2008, when global trade fell off a cliff. How would the Canadian economy have been affected? Many would see the drop in global trade as a demand shock hitting Canada, as there would have been less demand for Canadian exports. In fact, it would be an adverse supply shock. Even if the BOC had been targeting NGDP, output would have probably fallen. Factories in Ontario making transmissions for cars assembled in Ohio would have seen a drop in orders for transmissions. That’s a real shock. No (plausible) amount of price flexibility would move those transmissions during a recession. If the assembly plant in Ohio stopped building cars, then they don’t want Canadian transmissions. If the US stops building houses, then we don’t want Canadian lumber. That’s a real shock to Canada, i.e. an AS shock.

If the BOC had insisted on targeting NGDP, despite the huge drop in Canadian exports, then Canadian inflation would have risen. Canada would have moved to point c on the graph. A classic adverse supply shock. But they didn’t. The BOC targeted inflation. To keep inflation stable at 2% they had to reduce AD, which meant a tight monetary policy shifting AD to the left. This is why many economists support NGDP targeting; it makes output more stable when there are supply shocks.

I doubt that most people see the situation the way I do, even though the AS/AD model is quite clear, indeed given the fall in output and stable inflation, there’s not even any room for dispute. Both the AS and AD curves shifted left.

I think people disagree because they are affected by two common fallacies. In the comment section of the previous post John Papola pointed out that many people don’t understand that AS and AD shocks are basically real and nominal shocks:

The language of AS/AD may work well among economists who have a careful understanding of the distinction between monetary effects and real effects, but I believe strongly that it is difficult, even destructive, for non-economist readers precisely because nominal vs. real distinction becomes entangled. This is made worse by the fact that Keynesians explicitly discuss “demand” in terms of targeting real variables.

. . .

You said recently that macro students should only be taught two concepts: Say’s Law, and NGDPLT. I generally agree (even if I have concerns about NGDP being a sufficiently broad proxy for the flow of nominal spending). AS/AD doesn’t aid this understanding without it being HEAVILY caveated.

When the public hears about “demand”, they think about “consumers” buying stuff. They think about wrong-headed ideas like the often-repeated notion that consumers “drive” economic growth, rather than production and investment. They think about the Keynesian approach, which is all they hear. And the Keynesian approach rolls in with it the conflation between saving and hoarding that has plagued macro since Malthus.

I think John is on to something here. Most people think of AD in terms of the real quantity demanded, not a given nominal quantity of spending. As an aside, most economics students make the same mistake in basic supply and demand. They think the big boom in PC sales during the 1990s occurred because there was more “demand” for PCs. Consumers piled into the stores and bought more PCs. Of course economists know that the supply increased, reducing price, and increasing quantity demanded. The same is true at the aggregate level. The real shock hitting Canada in 2008-09 looked like a drop in AD, because real output fell. But we know that even if the BOC had targeted NGDP, output would have fallen. Targeting NGDP doesn’t magically make Ohio automakers want more Canadian transmissions. It doesn’t make American home-builders want more Canadian lumber. Yes, the Canadian dollar fell somewhat, but not enough to prevent a fall in exports.

Canada had a “reallocation recession.” Labor had to re-allocate out of declining sectors into other sectors—like Canadian home-building.

But the BOC then made it worse; they reduced AD to keep inflation from rising above 2%. Here’s where the other source of confusion comes in. Most people have trouble envisioning that the BOC ran a tight money policy. After all, they cut interest rates!! If you don’t know the fallacy of that assumption by now then GET THE HELL OUT OF MY BLOG.

The proof’s in the pudding. NGDP growth fell significantly; hence the BOC ran a tight money policy, at least tight relative to the policy that would have provided macroeconomic equilibrium. That is, they failed to provide a steady growth rate of NGDP; a policy that would have allowed labor re-allocation to occur in an accommodating environment.

Canada was hit by a double whammy; a reallocation recession, plus a demand shock recession. The net effect was a deeper than necessary recession, and no change in inflation. Still it could have been worse. Money wasn’t as tight as in the US and Europe.

Since then (former BOC governor) Mark Carney has become more receptive to NGDP targeting, and I’d guess for much the same reason that Nick Rowe has become more receptive. It seems like Canada could have benefited from more AD in 2009. But inflation targeting didn’t provide that signal. The NGDP data was sending a “warning, too little AD” signal loud and clear.

John’s pessimistic about the AS/AD approach:

Can we find a way to talk about these monetary issues that illuminates good policy without steering readers in the Keynesian cul-de-sac?

I’m less pessimistic. The problem John observes is just as common with ordinary S&D. Yet we don’t give up on that model. I’d suggest relabeling the AD curve as “NE,” meaning nominal expenditure. That might reduce the tendency to equate “AD” with “quantity of output bought and sold.”

This approach would also fit in with how we teach the “classical dichotomy.” Teach students how NGDP gets determined, and then teach students how changes in NGDP get partitioned between inflation and real output. That’s the essence of macroeconomics in a nutshell, but you’d never know it from the endlessly misleading Keynesian language.

Leave a Reply