Expectations are running high heading into Facebook’s (NASDAQ:FB) earnings report, but the major question at this point is, are people setting themselves up for disappointment? The stock dropped like a rock following its overpriced IPO amid concerns about the lack of a discernible business model and growth plan. Since bottoming out below $18, though, Mark Zuckerberg has delivered the talk about a greater focus on mobile and search, and the stock has responded in kind with an 85% rally in five months. Now, can he walk the walk with a strong earnings report?

LinkedIn (NASDAQ:LNKD) has long been the “grown-up” among the social media stocks, and the price action is the best evidence. Facebook really started the meat of its comeback on November 14th, ironically the day the company saw 800 million shares, or 30% of the net float, expire from the IPO lock-up. Many believed that the flood of supply entering the public float would weigh on the beaten-down stock, and positioned according, but instead we got a massive short squeeze on that day. The stock hasn’t looked back since.

The stock filled its earnings gap from July within two weeks of that November 14th reversal and reclaimed all of its major moving averages. After that strong late November run, the stock put in some healthy digestion. In my 2013 predictions, I highlighted a very clean, bullish cup and handle pattern in FB that set the stage for a strong start to the year. The move happened much faster than even I expected, which is always a possibility with newer issues.

Facebook did get a slight pullback surrounding its surprise event that turned out to be the unveiling of “Graph Search,” which will allow users to search for information on their friends’ Facebook profiles. The feature itself wasn’t necessarily a game changer, but evidence that the company was on the right track in thinking about search and advertising opportunities.

In the end of the pullback was controlled, and Monday we saw FB make a new 2013 high after taking out $32.21 pivot level. It has gotten upgrades from several analysts, who mainly point to a better monetization of its mobile ads. Facebook’s mobile business is expected to grow by more than 75% from the previous quarter and make up about 26% of its total ad revenue.

(click to enlarge)

The advertising expectations for Facebook’s earnings numbers are also elevated due to good reports from Google (NASDAQ:GOOG) and Yahoo! (NASDAQ:YHOO). Both internet giants posted strong advertising sales.

On its chart, Facebook now has a major resistance level at $33.45-33.60 level. A good earnings report could help the stock burst through this key level and make its path to the upside a bit cleaner. However, as expectations build and the herd jumps on the bandwagon, be a bit more calculated and analyze your time fame.

Constructive strength is also seen in Facebook’s social media peer LinkedIn. The stock closed at all-time highs on Monday, and has been one of our recent focuses on Off the Charts. The stock triggered our buy action area at $115.50-116 when it broke the descending channel with a gap and go. After that Linkedin continued to grind higher and build a solid upper-level base before igniting higher again to fresh all-time highs yesterday.

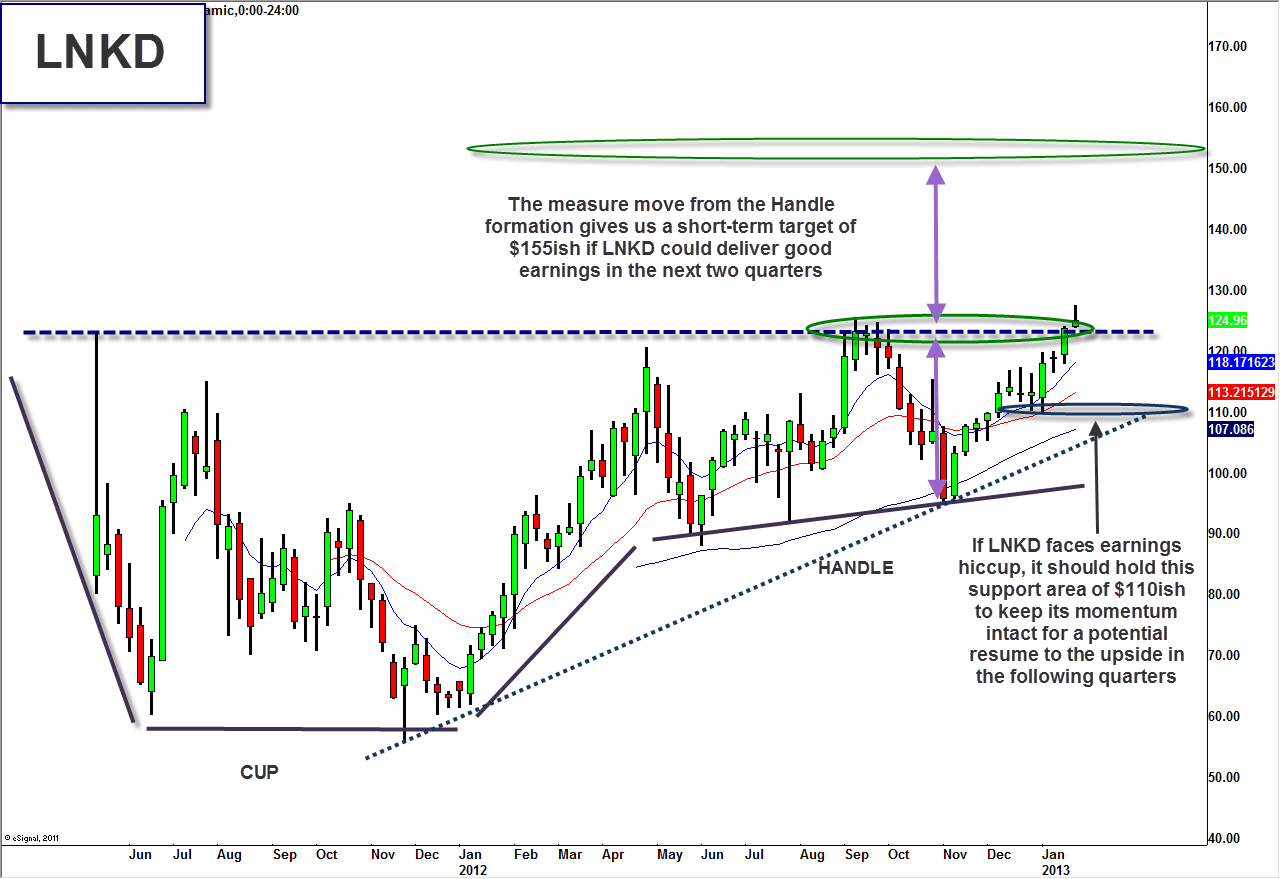

On a macro look, Linkedin also has a Cup and Handle chart pattern forming since its IPO. The measured move from the handle could take us to a $155 target if the company delivers solid earnings in the next two quarters.

(click to enlarge)

After making a new highs, Linkedin has slipped a bit to the downside this morning. As long as it holds above $123.50 key support/resistance level, I believe its pent-up momentum could remain intact to keep the bulls in the game. Linkedin is reporting earnings on February 7 with a consensus EPS estimate of $0.19, according to earnings.com.

Disclosure: Scott Redler is long AAPL, BAC, WFC, MGM, GE, ZNGA, TBT. LNKD Call spread. Short SPY. Traded but flat DDD, NFLX, BIDU.

Leave a Reply