Jeffco’s well regarded Telco analyst Peter Misek is backing off of his uber-bearish stance on Research in Motion (NASDAQ:RIMM) this AM and upgrading the name to a Hold from Underperform.

– According to Misek RIMM could be a ~$43 stock in 12 months, if things go well.

Preliminary results from Jeffco quarterly handset survey indicate developed market carriers have a much more positive view of BB10 than Misek expected. With greater carrier shelf space and marketing support, he now believes BB10 has a 20%-30% probability of success. While the likelihood is low and Jeffco remains well below St for the Nov Q and Feb Q, the potential reward is high.

Preliminary Survey Results Indicate Carriers Will Support BB10

Checks in the fall of 2010 pointed to a high level of carrier excitement around BB10 (then called QNX). Carriers wanted a third ecosystem to reduce their reliance on Android and iOS.

But two years later, after integration challenges with RIM’s BIS/BES infrastructure and continued execution issues, RIM has still yet to launch BB10 handsets.

This summer the firm trialed the BB10 developer alpha handset. They saw significant potential for it, and it certainly is a vast improvement over BB7 devices; however, they believe it is highly unlikely that BB10 will be an improvement over iOS 6 and that it will be about equal to Android Jelly Bean 4.2.

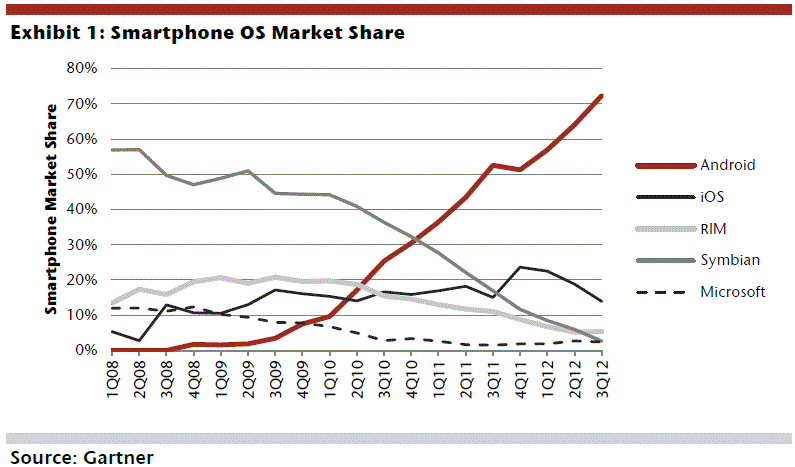

(click to enlarge)

The delay caused RIM’s new OS to fall from cutting edge to middle of the pack, and Jeffco’s own checks indicate that developer support has steeply declined. A large factor was the market share losses (falling from >20% to 5%), which limited the monetization opportunities for developers

Preliminary survey results indicate carriers will support BB10. Jeffco notes they have been surprised by the strongly positive initial feedback on BB10 from carriers (who admittedly have every incentive to be bullish). They are a bit puzzled as they expected a more muted response given BB10 is two years late and RIM’s market share has plunged from 20% to 5%. Firm’s theory is that carriers see BB10 as one of their last chances to avoid being locked into a long-term smartphone OS duopoly.

Additionally they believe RIM will be swinging for the fences with BB10 and will have significant presence at MWC and potentially even at CES.

Risk/reward more balanced. Scenario #1 (20%): Despite better prospects Jeffco still sees only a 20%-30% of BB10 success as consumer demand will be the ultimate determinate; however, they see BB10 success (which would also increase the potential for licensing) leading to a ~$43 stock in 12 months. Scenario 2 (20%): RIM could be sold if BB10 fails; however, this will likely be a takeunder at $5-$7. Scenario 3 (60%): BB10 fails, no acquisition, and continued cash burn leads the stock toward $0. The weighted probability of these scenarios equals firm’s new $10 target.

Notablecalls: Misek is the Axe in RIMM. His comments tend to move the name even if there is no rating change involved. This time there is.

His findings are certainly of interest – who knew the carriers would still be THAT interested in BB10? I certainly didn’t. Investors had left this one for dead. Even the turmoil surrounding Nokia (NYSE:NOK) was getting more attention from investors than RIM.

It’s all about carrier support these days. And the carriers want to break away from the Android/iOS duopoly. BB10 suddenly has a fighting chance.

Also, more BB10 hype could be in store at MWC and CES, which bodes well for the stock.

Last time Misek upgraded RIM to Hold was back in Dec ’11. The stock produced a 10%+ move on the day, 20% move over the next 5 days and a staggering 40% move over the next 30.

There’s a 20% short interest in the name. Will they stick around to see if Misek is right and the stock goes up 300% from here? Or will they cover? 4:1 risk reward situation.

I’m thinking $10.50+ levels today.

I like what I have seen in BB10 demos on-line. If the phones deliver I will buy one. I am getting tired of all the glitches on my 4.2 Nexus update!