What is it about fiscal policy that brings out the crazy? Because it all seems pretty simple. Joe Weisenthal hits the nail on the head:

The U.S. recovery has been remarkable on a comparative basis precisely for one reason: Because despite all of the rhetoric, the U.S. has completely avoided the austerity madness that’s gripped much of the world.

Weisenthal points us to Ryan Avent and Josh Lehner, both showing in different ways the better post-recession outcomes experienced by the US compared to other economies. Paul Krugman extends the argument by comparing the divergent path of Eurozone and US unemployment rates. The key difference in policy – the US pursued a more aggressive fiscal policy and didn’t pull back too quickly. I don’t think you can emphasize this point enough.

Which brings us to the fiscal cliff (or slope, which is more accurate and avoids creating the false impression that all is lost come January 1). The tax increases and spending cuts in place promise to repeat the mistakes of the UK and the Eurozone by pivoting too fast and too hard into the realm of fiscal austerity. A solution to the fiscal cliff means smoothing the path to fiscal consolidation (optimally, with no austerity in the near term, but I don’t see that as an outcome). The proximate cause of Weisenthal’s ire is former Federal Reserve Chairman Alan Greenspan, who says:

All of the simple low hanging fruits have been picked and the presumption that we are going to resolve the big issue on spending by making a few little twitches here and there I think is a little naive. If we get out of this with a moderate recession, I would say that the price is very cheap. The presumption that we will solve this problem without paying I think is grossly inappropriate…I think the markets are getting very shaky. And they are getting shaky because I think fiscal policy is out of control. And I think the markets will crater if we run into any evidence that we cannot solve this problem.

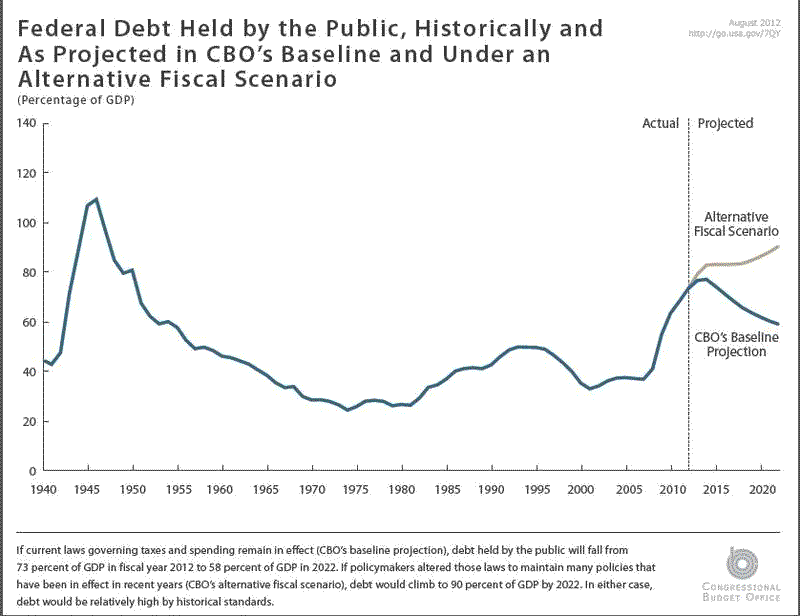

As Weisenthal notes, this is a completely backwards analysis. Let’s make this clear: If you think fiscal policy is out of control, you should welcome the fiscal cliff. From the CBO:

(click to enlarge)

If markets are shaky, they are shaky because participants recognize the recessionary impact of this level of fiscal austerity and they don’t like it. Market participants want Congress and the President to do exactly what Greenspan claims is impossible, minimize the impact of spending cuts.

It is truly time for Greenspan to simply fade away; he no longer has anything useful to add to the discussion. Of anything. Who should join him is Dallas Federal Reserve President Richard Fisher. Fisher laid further claim to the title of “Worst Monetary Policymaker Ever” in a speech last week, first by describing Congress as “parasitic wastrels.” It should be obvious that this is not exactly speech conducive to maintaining an independent central bank. He continues with this tirade:

The jig is up. Our fiscal authorities have mortgaged the material assets of our grandchildren to the nth degree. We are at risk of losing our political heritage of reaching across the aisle to work for the common good. In the minds of many, our government’s fiscal misfeasance threatens the world’s respect for America as the beacon of democracy…So my only comment today regarding the recent federal elections is this: Pray that the president and the Congress will at last tackle the fiscal imbroglio they and their predecessors created and only they can undo.

The rise in neo-Nazi’s in Greece is a democratic outcome of austerity? Again, Fisher just doesn’t get it. He seems to believe that the challenge upon us is to radically cut spending. Again, this is absolutely not the challenge upon us. In the middle of this tirade he launched into another:

Only the Congress of the United States can now save us from fiscal perdition. The Federal Reserve cannot. The Federal Reserve has been carrying the ball for the fiscal authorities by holding down interest rates in an attempt to stoke the recovery while the fiscal authorities wrestle themselves off the mat. But there are limits to what a monetary authority can do. For the central bank also plays a fiduciary role for the American people and, given our franchise as the globe’s premier reserve currency, the world. We dare not become the central bank counterpart to Congress by adopting a Buzz Lightyear approach of “To infinity and beyond!” by endlessly purchasing U.S. Treasuries and agency debt so as to encumber future generations of central bankers with Hobson’s choices when it comes to undoing what seems contemporarily appropriate.

Fisher appears to be under the delusion that the economy is suffering from the effects of large deficits (which require “fiscal authorities to wrestle themselves off the mat”), and the Federal Reserve is the sole support of those deficits. He continues to look at the world as if the US economy was operating well above potential, and that only the Fed stands in the way of 10% interest rates. Of course, if this were true, unemployment would not by near 8%, wage growth would not be scraping the floor, and inflation would not be hovering below the Fed’s 2% target. Fisher is not dissuaded by these little facts.

And, by the way, despite Fisher’s argument to the contrary, being the counterpart to Congress is exactly what the Fed will do as long as the economy is unable to exit the zero bound in the absence of fiscal stimulus.

Why are Greenspan and Fisher so horribly wrong? Because they belong to a group that has worried incessantly that large deficits would bring economically ruinous high interest rates and, unless held at bay by the Federal Reserve, runaway inflation. Such worries have been repeatedly proved unfounded, but Greenspan and Fisher have no other intellectual framework to fall back on. When you only have a hammer, everything is a nail. For them, any question of fiscal policy always needs to be twisted into their version of the world, even when the opposite is so completely obvious to just about everyone else at this point.

Finally, despite the ongoing evidence that fiscal austerity has failed and now pushed the Eurozone back into recession, we get this from European Central Bank President Mario Draghi (via FT Alphaville):

In my joint work with the Presidents of the European Council, the European Commission and the Eurogroup, we have identified four pillars on which to build a stable and prosperous Europe: a banking union with a single supervisor; a fiscal union that can effectively prevent and correct unsustainable budgets; an economic union that can guarantee sufficient competitiveness to sustain high employment; and a political union that can deeply engage euro area citizens.

Sounds good, right? But pay close attention to his definition of a fiscal union. It remains nothing more than an austerity union, a mechanism to control deficit spending. But a fiscal union is so much more. It transfers resources across regions. It serves as an insurer for all regions. And it frees the central bank from having to be the lender of last resort to individual regions. For Draghi, however, a fiscal union is just a mechanism to control spending. And controlling spending has done little more than push the Eurozone deeper into recession. Draghi might have prevented financial collapse, but the price he extracted ensures ongoing recession nonetheless.

Bottom Line: We need to find a cure for the crazy that some fall into whenever the topic is fiscal policy.

Leave a Reply