Eugene Fama states that the low volatility anomaly is really just the excess return low beta, and this has been well known for 50 years. I think its indisputable that low beta underperforms high beta, but I guess that’s a fun fact of contention. It’s fun to find yourself on the minority side of a fact you think other’s don’t agree with.

His mention of 50 years can only mean that the Security Market Line (ie, relating beta to average returns) is insufficiently increasing, positive but not as much as theory suggests. That’s one implication of the low volatility anomaly, but it’s much worse than that. The Low Volatility anomaly targets two things Fama can’t admit: the Security Market Line is negative, and the essence of low vol investing is vol, not beta.

Here’s the total return on three portfolios: the aggregate market, the top 1500 stocks (in market cap, non etfs, nonfinancials) with lowest beta, those with highest beta. High beta does significantly worse, and low beta significantly better, than the market as a whole.

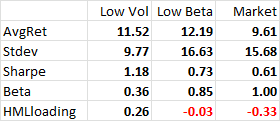

As per Low Beta being the essence of the Low Volatility Anomaly, here’s the stats on monthly returns for portfolios formed via low volatility, low beta, and the market (as a comparison).

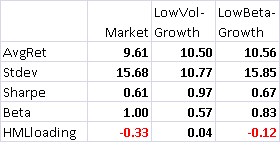

Now, the much higher Sharpe, supposedley, is because of the value loading, which is higher for low volatility portfolios. But look at how a low volatility portfolio amongst the bottom 50% of book/market stocks (aka growth stocks) does, relative to the low beta portfolio:

On a Sharpe level, the low vol sorting produces a greater anomaly than the low beta sort, and this is highlighted by fact that the Sharpe ratio disparity persists with the below average book/market subset.

In all dimensions, the volatility sort is more anomalous than the beta sort. Further, there is a return premium to low beta/vol, which simply can’t be fit within the standard model.

Disclaimer: This page contains affiliate links. If you choose to make a purchase after clicking a link, we may receive a commission at no additional cost to you. Thank you for your support!

Leave a Reply