Rebalance daily! Turan Bali, Nobel Prize winner Robert Engle and Yi Yang, posted Dynamic Conditional Beta is Alive and Well in the Cross-Section of Daily Stock Returns over at the SSRN. It’s an eerily similar title to Jagannathan and Wang’s 1994 pub The CAPM is Alive and Well, which supposedly showed the same thing. When people have to continually state something is ‘Alive and Well,’ you can be pretty sure it is ‘Dead or Dying.’

Such research confirms my thinking that prejudices are more important than statistics when analyzing complex data, because people tend see what they believe rather than vice versa. Thus, developing good prejudices is more important than developing good econometric skills, reminding one of Oscar Wilde’s dictum that ‘Education is an admirable thing, but is well to remember from time to time that nothing that is worth knowing can be taught.’

In any case, they state:

Average return and alpha differences between stocks in the lowest and highest conditional beta deciles are about 8% per annum, implying a profitable zero-cost portfolio that goes long stocks in the highest conditional beta decile and shorts stocks in the lowest conditional beta decile.

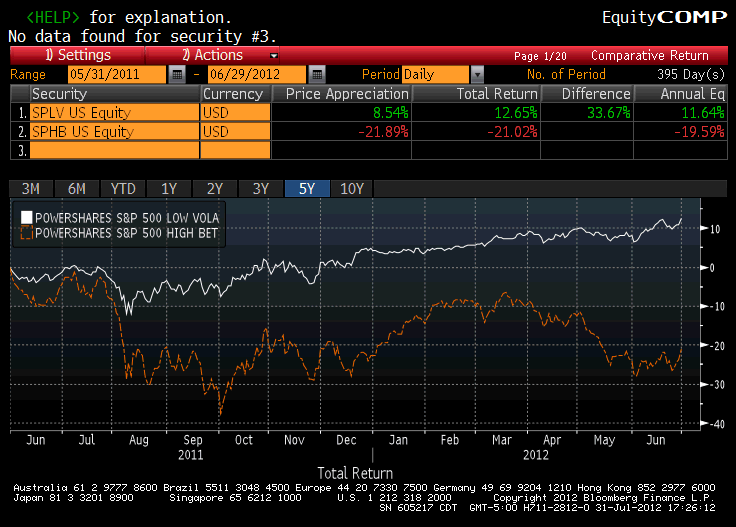

If higher beta stocks did have higher returns, many investors would hold their nose at the volatility and accept the price for a higher return. Yet, the risk and return are both lousy, so such a fund has never been popular. Consider that the low vol ETF SPLV trades about 1 million shares a day, while the high beta ETF SPHB trades about 50k shares per day. SPLV is up since inception in 5/11, while the SPHB is down (see below).

(click to enlarge)

It’s a short sample to be sure, but one can ask Robeco or Arcadian how their low volatility funds have done, among many real-world examples (eg, I wasn’t sued because low volatility didn’t produce positive alpha). Indeed, a glaring datapoint against the assertion that higher beta implies a higher return is the absence of a popular, explicitly high market beta fund, precisely because such stocks have had horrible returns. Consider there have been value and size portfolios even though these have high value and size risk, because they have higher-than-average returns. As mentioned, if higher beta truly gave one a return premium, desperate investors like CalPERS would gladly take on the risk.

The authors spend a lot of time on various subtle refinements of beta, making sure they are super fresh and estimated with the much more sophisticated Maximum Likelihood method, as opposed to some simple matrix inversion. They correctly note that the CAPM, and any of its derivatives (the APT, the SDF), are conditional, and so theoretically you need to update your beta estimates constantly as conditions change.

I’ve played around with beta calculations enough to know there isn’t any real edge to doing something really tricky. Sure, you can do better than using the past 9 months of daily data using an exponential lag by adding some trickier refinements, but not much. The 36-month betas ubiquitous in the literature generate qualitatively similar outcomes for everything I’ve looked at, so that’s not the key problem with the CAPM, any more than using the equal or value-weighted indices (also irrelevant). Indeed, their own paper shows their four different betas generate the same positive return to beta (a 4% annualized spread), only more so (8% annualized) if you update in more frequently than once a year. So, their refinement doubles a return advantage that practitioners don’t see.

In any case, this is irrelevant. The key is that they are using daily returns. Now, daily returns are problematic ever since the first estimate of the size effect was found to be overstated by 15% (annually) due to daily rebalancing effects (see Blume and Stambaugh). Using monthly return data, since 1962, I find beta negatively correlated with returns, excluding the bottom dregs of penny stocks that add spurious precision but are untradeable (basically, I took the current $500MM cut-off, and applied that backwards in real terms). The data is over at www.betaarbitrage.com.

It would have been better to instead correct for the daily rebalancing bias rather than all that beta refinement so reminiscent of the 1980’s focus on ever more sophisticated tests that produced nothing of lasting importance to anyone but a tenure-seeking finance professors.

But hey, lots of people worry about crowding into the low-volatility space, so I’m happy that the old guard doesn’t have to change their mind about this if they don’t want to. As Max Planck said, science progresses one funeral at a time. It’s a mug’s game trying to swat down all these statistical refinements that theoretically could matter, but don’t. Much better to actually trade an idea and see if it works. Too bad about finance students, however, spending valuable time learning a beautiful theory that is 180 degrees wrong, all for $50k/year.

Leave a Reply