Recent increases in the monetary base have all gone into excess reserves, and so inflation has remained low, and monetary stimulus isn’t stimulating. This puzzles many people, but I have a theory for it. The idea is that while equity owners–management–are like owners of call options on the assets of a firm (aka the Merton Model), banks are like down-and-out call option owners, because if their book equity goes down too far they will be forced into a fire-sale or liquidated by regulators.

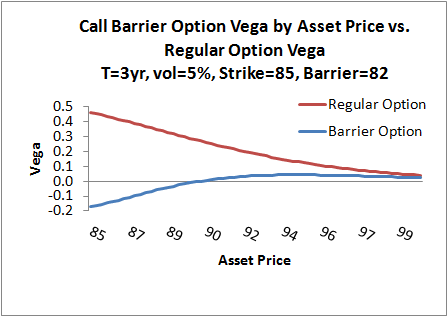

This is a barrier option, and has the interesting property that its vega–the derivative of the value of the equity with respect to asset volatility–is negative when it gets close in value to its barrier. A standard call option loves volatility, the greater the better. This can be shown by noting that an option is worth something like max(0,x), where x is a random variable; the higher the volatility of x the more an option is worth. With a down-and-out constraint, a loss can cause the equity to forever extinguish, and this causes the vega to actually go negative when close to the absorbing barrier.

That is, consider the difference in vega in the graph below.

If you have negative vega, adding risk or volatility hurts your equity value, so you turtle in, and wait like the 1990 Japanese banks for inflation and retained earnings to cure your precarious position. Banks are still in their negative vega zone currently, afraid to do anything that will either get them into legal trouble, or generate any losses that would force them into liquidation. So, they aren’t lending their new cash balances but rather hoarding them as protection.

Bank of America (BAC) recently paid a $2.4B fine to settle claims it misled investors about the acquisition of troubled brokerage firm Merrill Lynch. That brings its total fines since 2010 to $29B with no end in sight (eg, the Libor fixing scandal). Banks get fined for not lending enough to minorities, and lending too much. If the government would stop treating the banks like the Knights Templar circa 1307, the economy would recover much faster. A modern economy needs banks, ones that want to take risks and grow.

Leave a Reply