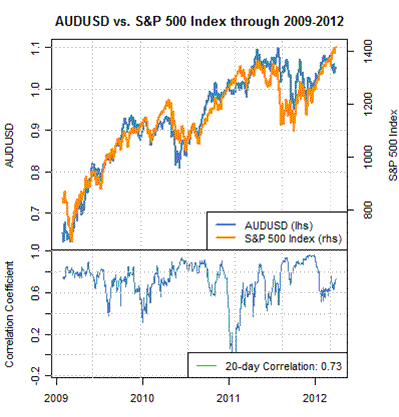

A few soft days and the bears clamor for P3 down or the end of a large Ending Diagonal. Instead I am watching the AUD. An interesting correlation since the Global Financial Crisis has been AUD and the S&P.

The rationale for the correlation is the Global Scramble for Yield that I first mentioned almost a decade ago – in a low return environment money mangers scramble anywhere they can for smidgeons of yield. The Greenspan Put exacerbated this, and so too the Bernank’s QE.

The more specific correlation is that QE drives up commodities, something also predicted here, and therefore commodity currencies like the AUD. Australia, however, is now in a bind, as its currency is over-valued for its value-added industries, and its mining exports are suffering due to the Chinese slowdown that may yet turn into a hard landing. Indeed, the AUD correlation broke over the past nine months as China began to slow:

(click to enlarge)

The bind puts pressure on the RBA to lower rates, to weaken the AUD and support the slowing failing housing sector.

We can tell which it is (liquidity pump/optimism or rush to safety/fear) by looking at the TNX (ten year Treasury). In the final rush to safety, its rate should fall below their recent low of 1.4%, maybe down to 1.2%. Right now the TNX has gone the other way, and many pundits – including EWI in a recent bond report – says the great bond bull market is over. We’ll see.

The neoclassical economics have pushed the liquidity pump, and want it to be followed up with fiscal stimulus. Problem is, that ain’t happening as tea party types around the globe have instead pushed for various forms of fiscal responsibility and austerity. This has caused many of the leading economists to get a bit hysterical, since they know that the liquidity pump sans a fiscal pump leads to a deeper drop than we saw in 2001 or 2008. Hence you see in a lot of predictions a growing sense of a disaster, a cliff the world is about to fall off of.

In the short run, such as US equities this past week, we saw a fade off the recent QE rally. Indeed, most of the QE Rally across various markets is gone, except in commodities. Does this mean we have topped? Unlikely. Neely sees us in a pattern which should soon turn north again, have a fade, then another run up. This might unfold all the way into the election, especially if it remains close.

Rather than call the top, watch the divergence.

Leave a Reply