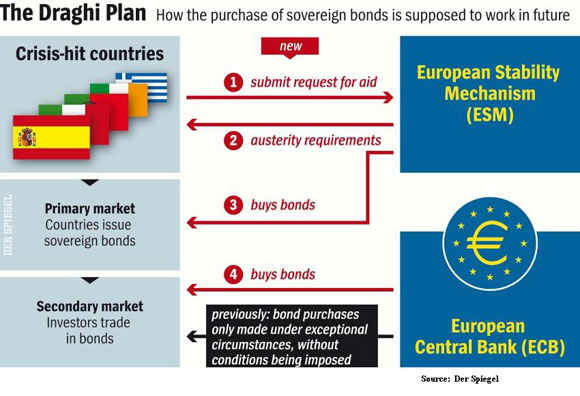

The only thing new in the “Draghi Plan”, as far as we can see, is the potential big bazooka #4 — unsterilized (?) purchases of periphery bonds by the ECB.

Still, though, countries will have to submit to conditionality — fiscal consolidation, and structural adjustment. That is, austerity. Is that politically doable in Italy? A Kiss of Death?

Furthermore, will the Germans allow debt monetization on a grand scale?

In his Bloomberg opinion piece former chief economist of the IMF, Simon Johnson, doesn’t think so,

More likely, a shift in ECB policies would make the European situation uglier. For one, Draghi would essentially be conceding fiscal dominance, demonstrating that if governments run budget deficits, they can count on the central bank to finance them. More important, the political consequences could be dire if the ECB actually succeeded in stoking German inflation and weakening the euro.

Inflation is unpopular and very unfair. People who think that higher inflation would somehow help the poor and hard pressed in the European Union should study economic history more carefully. It could lead the Germans to question the viability of the euro, increasing the risk that the currency will break apart for political reasons. The Germans didn’t turn over their monetary sovereignty to the ECB to facilitate bailouts of irresponsible governments and the crazed banks that funded real- estate bubbles. Throwing greater fiscal transfers from Germany into the mix will serve only to worsen the situation.

Perhaps Draghi is planning the same game with fiscal authorities that the Banca d’Italia used to play with Italian politicians in the 1980s and early 1990s — keep interest rates low enough to prevent fiscal collapse, yet high enough to keep fiscal prudence as a priority. Make no mistake about it, inflation or not, this is a strategy of high real interest rates.

We’re not as lathered up on the Draghi Plan as the markets seem to be.

Leave a Reply