The half-life of European bailouts is getting shorter and shorter, which should come as no surprise in these kinds of repeated games. The announced Spanish bank bailout triggered some early euphoria in financial markets which at the moment is quickly fading. Why? I suspect that market participants fear the bank bailout is simply a precursor to a much bigger bailout of Spanish government debt, a bailout that will involve some sizable private sector involvement.

One of the most telling stories is this from the FT:

Spain’s Treasury on Monday vowed to continue as normal with sovereign bond auctions, arguing that the eurozone’s weekend agreement on a €100bn bailout for Spanish banks would underpin the country’s debt market.

Spain desperately needs to be able to finance at lower bond yields – the fiscal situation simply is not sustainable at interest rates currently north of 6%. They can’t close deficits fast enough at those yields. Moreover, the ECB for all intents and purposes is out of the game. Not only do they feel honor bound to avoid anything that looks like the direct financing of national deficits, but they have likely run out of patience. Recall ECB President Mario Draghi’s comments in May:

In a damning indictment of Spain’s handling of the problems at Bankia, its third largest lender, ECB president Mario Draghi said national supervisors had repeatedly underestimated the amount a rescue would cost. He also cited the rescue of Dexia, the Franco-Belgian lender, as an example.

“There is a first assessment, then a second, a third, a fourth,” Mr Draghi said. “This is the worst possible way of doing things. Everyone ends up doing the right thing, but at the highest cost.”

One also wonders what kind of fiscal deterioration is being hidden from the general public. Or other EU officials for that matter.

Apparently, the hope was that by channeling the bailout funds to Spain’s Fund for Orderly Reconstruction, it would appear as if Spain itself is not paying for the bailout. The lack of a “program” with IMF involvement was added to further create the illusion that this was not a sovereign bailout, and was instead some type of EuroTARP. Thus, a potential liability would be avoided and Spanish bond yields would fall accordingly. In essence, the bank bailout was a last-ditch gamble on the part of the Spanish government to avoid a general government bailout. (For further reading, FT Alphaville has a nice series of posts trying to understand the details of the bailout. See here, here, and here).

The trouble is that market participants started to poke holes in this ruse, realizing that the bailout is just sovereign debt by another name, and debt that most likely would be senior to existing bondholders. There was some initial confusion over this point, although it seems that Germany wants the funds to coming from the soon-to-be-launched ESM, in which case the debt will be senior. It really doesn’t matter, though. FT Alphaville hits the nail on the head:

But we’ll close by noting even ‘pari passu’ EFSF debt (or ESM debt which might subsequently absorb EFSF pari passu status) has shown signs of de facto seniority in Greece. EFSF loans to Greece were rescheduled before bondholders, but when it came to the PSI, the EFSF did not take write-downs in common with bondholders.

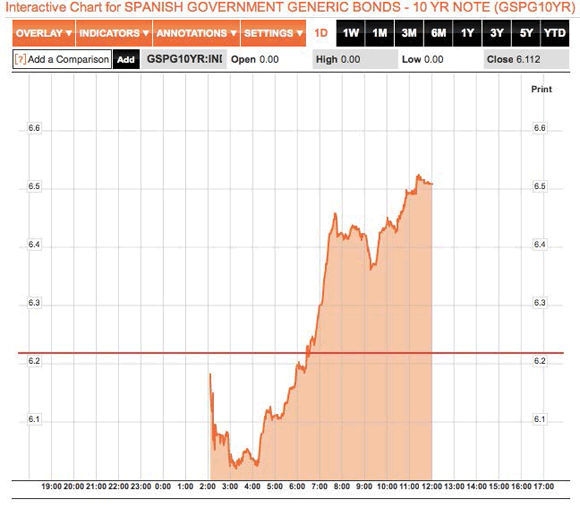

I think that no matter how many smoke and mirrors the Europeans try to put into the place, they can’t cover up the fact that the Spanish government owns this bailout. Market participants came to this conclusion as well and sent Spanish yield higher:

Which means that as of roughly 9am on the West Coast, Spain’s gamble has failed. And that pushes Spain once step closer to a real bailout of sovereign debt, and the mess – private sector involvement, Troika monitoring, etc – that comes with it.

Leave a Reply